Understanding why mortgage rates vary by lender can help you select the right lender for your situation.

Hey there, folks! If you’ve popped open your mail or got a call from your mortgage lender saying, “Hey, we wanna lower your rate!” and your first thought was, “What’s the catch?”—you’re not alone I’ve been there, squinting at those letters like they’re written in some secret code Why on earth would my mortgage company offer me a lower rate outta the blue? Are they suddenly feeling generous, or am I about to get played? Let’s dive into this headfirst and figure out what’s really goin’ on with these offers. Spoiler It ain’t always as sweet as it sounds, but it ain’t always a scam neither.

At our lil’ corner of the internet here, we’re all about breakin’ down the complicated money stuff into plain ol’ English. So, grab a coffee (or a beer, I ain’t judgin’), and let’s unpack why your mortgage company might be sliding this offer your way, whether you should jump on it, and how to avoid gettin’ burned.

The Big Picture: Why They’re Dangling a Lower Rate

Before we get into the nitty-gritty let’s start with the most likely reasons your lender is suddenly playin’ Santa Claus with your interest rate. Mortgage companies ain’t charities, so there’s always somethin’ in it for them. Here’s the deal

- They Wanna Keep You as a Customer: Yo, if you’ve been payin’ your mortgage on time, you’re a goldmine to them. But with so many lenders out there, they know you could refinance elsewhere for a better deal. Offerin’ you a lower rate is their way of sayin’, “Stay with us, buddy!” It’s cheaper for them to keep you than to lose you to the competition.

- Market Rates Are Droppin’: If the big dogs at the Federal Reserve or wherever slash interest rates, lenders often follow suit. They might be offerin’ a lower rate ‘cause that’s just where the market’s at right now. It’s less about you and more about them stayin’ competitive.

- They’re Pushin’ a Refinance: Sometimes, a “lower rate” offer is really just a refinance in disguise. They’re hopin’ you’ll sign up for a new loan term, which might mean more years of payments or extra fees. That lower monthly payment? Might cost ya more in the long run.

- Your Credit Got Better: If you’ve been hustlin’ to boost your credit score, they mighta noticed. A better score means you’re less risky, so they could offer a lower rate to lock you in before someone else does.

- They’re Strugglin’ for Business: If the housin’ market is slow or they’re losin’ clients, lenders get desperate. Lowerin’ rates can be a way to drum up some action, even if it means slimmer profits for them.

I know what you’re thinking: Is this real, or am I losing my mind? Hold that thought. We’re going to talk more about each of these reasons, plus I’ll share some real-life stories about mortgage offers I’ve received. But first, let’s talk about the big red flag scams.

Watch Out: Not Every Offer Is Your Friend

I have to tell you the truth: some of these deals are as shady as a back-alley deal. A few years ago, I got a call from someone saying they were my lender and offering such a low rate that I almost dropped the phone. It turned out to be a scammer trying to get my personal information. It wasn’t even my real mortgage company. Here’s what to watch for:

- They’re Pushy as Heck: If they’re callin’ you non-stop or sayin’ you gotta sign NOW or the deal’s gone, that’s a bad vibe. Real lenders give ya time to think.

- Askin’ for Upfront Cash: Any “processing fee” or “application cost” before you even see paperwork? Run, don’t walk. Legit companies don’t do that mess.

- Fishy Contact Info: Check the email or phone number. If it ain’t matchin’ your lender’s official stuff (like, it’s a weird Gmail address or somethin’), it’s probably fake.

- Too Good to Be True: If the rate they’re offerin’ is way below market—think 1% when everyone else is at 4%—it’s likely a bait-and-switch.

If you’re smellin’ somethin’ off, don’t ignore that gut feelin’. Call your actual lender directly (use the number on your statement, not the one they gave ya) and ask if this offer is real. Better safe than sorry, right?

Breakin’ Down the Reasons: Let’s Get Specific

Alright, let’s roll up our sleeves and dive into why your mortgage company might genuinely be offerin’ a lower rate. I’m gonna lay it out clear as day, ‘cause I know this stuff can feel like readin’ a foreign language sometimes.

1. Keepin’ You Loyal (Customer Retention, Baby!)

Mortgage companies spend a lotta dough to get new customers—think ads, fancy offices, all that jazz. Losin’ a good borrower like you means they gotta start from scratch. So, if they think you might refinance with someone else, they’ll dangle a lower rate to keep ya in their camp. It’s like when your phone company offers a discount right before you cancel. Same game, different players.

Here’s how it usually plays out:

- They check your payment history and see you’re solid.

- They peek at market rates and notice competitors are offerin’ better deals.

- They send you an offer to match or beat those rates, hopin’ you’ll stick around.

I remember when my lender dropped my rate by half a percent outta nowhere. I thought, “No way!” But after some diggin’, I realized they’d just lost a bunch of clients to a rival bank. They were fightin’ to keep me. Worked, too—I stayed.

2. The Market’s Changin’ (Economic Shifts)

This one’s a bit more big-picture, but bear with me. When the economy shifts, so do interest rates. Home mortgage rates will go down if the Federal Reserve (the people who control the flow of money) lowers their rates. Your lender may offer a lower rate because they are getting used to the new normal. It ain’t personal; it’s just business.

Check this quick table to see how it works:

| Economic Thing | What It Means for You |

|---|---|

| Fed Lowers Rates | Lenders drop mortgage rates to stay competitive. |

| Housing Market Slows | Less demand means lenders sweeten deals. |

| Inflation Cools Down | Lower rates across the board, includin’ yours. |

So, if you’ve been hearin’ on the news about “rate cuts,” that might be why your lender’s suddenly so generous. Timing’s everythin’!

3. They Want You to Refinance (And Make More Off Ya)

Now, this is where it gets a lil’ tricky. A “lower rate” offer might be a refinance deal. When you refinance, you get a new loan to replace the old one. Usually, the new loan has better terms or a lower interest rate. Sounds great, right? Not so fast. Sometimes, they’re countin’ on you not readin’ the fine print.

Here’s the pros and cons I’ve seen:

- Pros: Lower monthly payments, maybe pay off debt faster if you play it smart.

- Cons: Could mean a longer loan term (more interest over time), plus closin’ costs and fees that ain’t cheap.

I got burned once on this. Thought I was savin’ money with a lower rate, but didn’t notice the term went from 20 years to 30. Ended up payin’ way more interest. Lesson learned—crunch them numbers before signin’ anything.

4. Your Credit’s Lookin’ Good

If you’ve been payin’ off credit cards, keepin’ bills on time, or just gettin’ your financial house in order, your credit score mighta jumped. Lenders love that. A higher score tells ‘em you’re less likely to default, so they might offer a lower rate as a reward—or to lock you in before another lender does.

Quick tip: Check your credit report for free once a year (there’s websites for that, just Google it). If it’s improved, you got leverage. Heck, even if they don’t offer a lower rate, you can call ‘em up and ask!

5. They’re Hungry for Clients

Lastly, if the mortgage biz is slow, companies get desperate. Maybe new home sales are down, or folks ain’t refinancin’ much. To keep the cash flowin’, they’ll lower rates to attract business. It’s like a store havin’ a clearance sale—they’d rather make a lil’ profit than none at all.

I’ve seen this happen after economic dips. Lenders start mailin’ out offers left and right, hopin’ someone bites. If you’re gettin’ a flood of these letters, that might be the deal.

Is It Worth It? How to Decide

So, your mortgage company’s offerin’ a lower rate, and now you know why. But should you take it? That’s the million-dollar question (or, ya know, the hundred-thousand-dollar question, dependin’ on your loan). Here’s my no-BS guide to figurin’ it out.

Step 1: Do the Math

Get a calculator or one of them online mortgage tools. Plug in the new rate, the term, and any fees. See if you’re really savin’ money over time. Don’t just look at the monthly payment—check the total interest you’ll pay.

Step 2: Read Every Dang Word

I ain’t kiddin’. Grab that offer letter and read it like it’s a thriller novel. Look for hidden fees, prepayment penalties, or weird clauses. If it’s a refinance, check how long the new term is. If you don’t get somethin’, call ‘em and ask.

Step 3: Shop Around

Just ‘cause they offered don’t mean it’s the best deal. Get quotes from other lenders. I did this once and found a rate a full point lower somewhere else. My original lender matched it when I told ‘em I was walkin’. Play hardball if ya gotta.

Step 4: Think Long-Term

Ask yourself: How long you plannin’ to stay in this house? If it’s just a couple years, a refinance might not be worth the closin’ costs. But if you’re settlin’ in for the long haul, a lower rate could save ya thousands.

Step 5: Trust Your Gut

If somethin’ feels off, don’t ignore it. Talk to a financial advisor or a buddy who’s good with money. I’ve dodged a few bad deals just by listenin’ to that lil’ voice in my head.

My Two Cents: A Personal Story

Lemme wrap this up with a quick story from my own life. Few years back, my mortgage company hit me with a lower rate offer right after I’d been shoppin’ around online for refinance options. Coincidence? I think not. They dropped my rate from 4.5% to 3.8%, which sounded awesome. Monthly payment went down by about $150, and I was stoked.

But here’s where I almost messed up—I didn’t check the new loan term. They’d stretched it out an extra 5 years. I woulda paid way more in interest if I hadn’t caught it. After some back-and-forth, I got ‘em to keep the original term and still lower the rate a bit. Took some hagglin’, but it saved me a bundle.

Point is, these offers can be legit, but you gotta be sharp. Don’t let excitement cloud your judgment. We’re all tryna save a buck, but don’t let ‘em sneak one past ya.

Final Thoughts: You Got This!

So, why is your mortgage company offerin’ you a lower rate? Could be they’re tryna keep you loyal, matchin’ market trends, pushin’ a refinance, rewardin’ your good credit, or just hungry for business. Whatever the reason, it’s on you to figure out if it’s a deal or a dud. I’ve laid out the whys, the warnings, and the how-tos, so now it’s your turn to take the reins.

Here’s a lil’ recap checklist for ya:

- Double-check the offer’s legit (no sketchy vibes).

- Crunch the numbers—monthly savings vs. total cost.

- Compare with other lenders’ rates.

- Read the fine print like your life depends on it.

- Decide if it fits your long-term plans.

We at this blog got your back. If you’re still unsure, drop a comment or shoot us a message. I’ve been down this road, made the mistakes, and learned the tricks, so I’m happy to help ya navigate it. Mortgage stuff don’t gotta be scary—just gotta be smart about it. Now go out there and make sure you’re gettin’ the best dang deal possible!

How Are Mortgage Rates Determined?

Some factors affecting your mortgage rate are under your control because rates vary based on financial situations. Your mortgage rate will partially depend on how risky the loan appears to lenders.

Lenders will review your financial history to determine the likeliness of you making payments on time, falling behind on payments or completely stopping paying on your loan. They will consider how much money they could lose if you fail to make payments.

Other factors affecting how mortgage interest rates are determined may be beyond your control. By understanding what affects your mortgage rate, you can choose a lender with a competitive interest rate.

Factors You Can Control

Credit scores of 740 or higher will grant borrowers the lowest mortgage rates and the widest variety of loan product choices. Interest rates will be a little higher for borrowers with credit scores between 700 and 739, and they will be even higher for borrowers with a score that is 699 or lower. However, homebuyers with credit scores as low as 580 also have low down payment mortgage options.

Your debt-to-income ratio compares your monthly pre-tax income to your owed debt, such as student loans, leases, car loans and credit cards. Its the percentage of the income you spend on monthly debt payments and your new home loans projected payment.

Your lender will determine your debt-to-income ratio by combining your monthly debt payments with your projected mortgage payment and then dividing the total by your monthly income before tax.

Your down payment amount will also affect your mortgage rate because of the impact it has on your loan-to-value ratio. The smaller your down payment is, the larger your loan-to-value ratio will be. Similarly, the larger your down payment is, the smaller your loan-to-value ratio will be.

The loan-to-value ratio compares a mortgage amount to a homes value or price. For example, if you place a $30,000 down payment on a $120,000 home, the mortgage will be $90,000. Your loan-to-ratio value will be 75% because you are borrowing 75% of the houses value.

The loan-to-value ratio should be higher than 80% for lenders to consider it high, but not at Homesite Mortgage! We specialize in low down payment financing.

A lender may also charge you more for financial actions like cash-out refinances, adjustable rate mortgages and loans for manufactured or second homes, as these loans are riskier for the lender.

How loan officers TRICK YOU (and how to prevent it)

FAQ

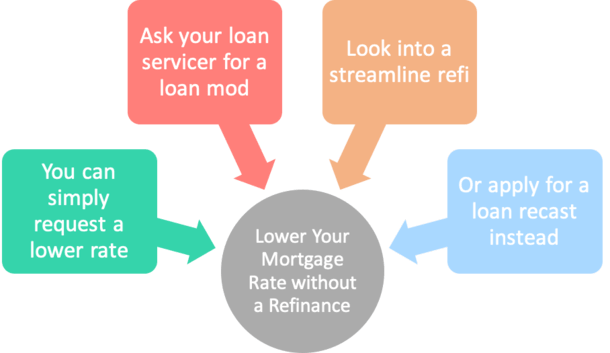

Can a mortgage company lower your interest rate?

Yes, a mortgage company can lower your interest rate, but it usually involves either a loan modification or a refinance. A loan modification is a permanent change to the loan terms, often reducing the interest rate to make payments more manageable.

Why is my mortgage payment suddenly lower?

Mortgage payments change based on what kind of home loan you have, or if your taxes and insurance premiums have changed. Your escrow account is used to pay for insurance and taxes. When there’s an increase or decrease to those costs, your mortgage payments are adjusted accordingly.

How much is a $300,000 mortgage at 7% interest?

Monthly payments on a $300,000 mortgage At a 7. 00% fixed interest rate, your monthly mortgage payment on a 30-year mortgage might total $1,996 a month, while a 15-year might cost $2,696 a month.

Is 7% a bad mortgage rate?

Compared to historical mortgage rates, 7% isn’t considered a high rate. While it might be high compared to pandemic-era rates that were sub-3%, it’s on par with mortgage rates in the 1990s, and considerably lower than the double-digit rates seen in the late 1970s and early 1980s.