Financial institutions try to lower the risk of lending money to people by checking the credit of people and businesses that want to open a new credit account or loan.

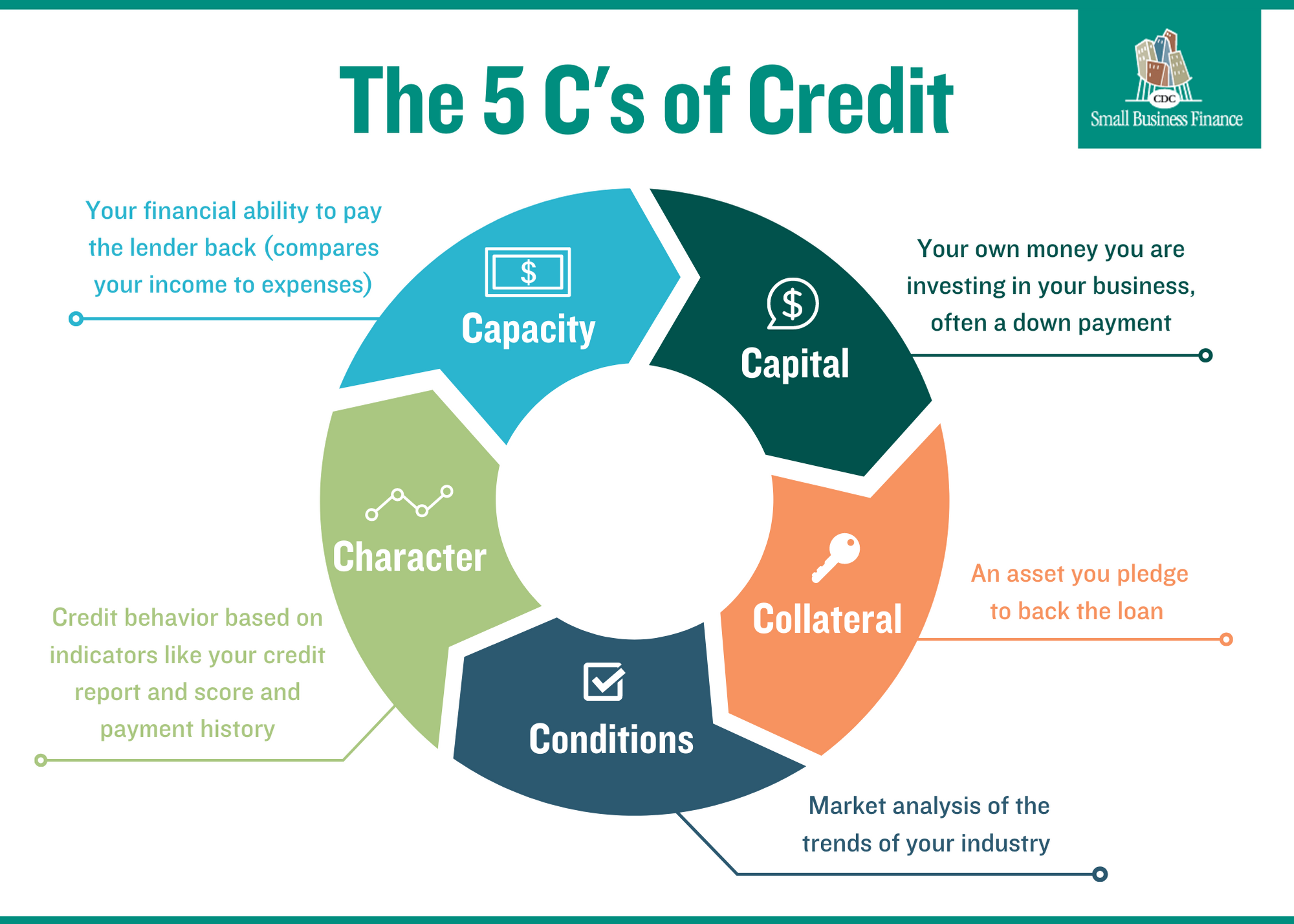

This review process is based on a review of five key factors that predict the probability of a borrower defaulting on his debt. Called the five Cs of credit, they include capacity, capital, conditions, character, and collateral. There is no regulatory standard that requires the use of the five Cs of credit, but the majority of lenders review most of this information prior to allowing a borrower to take on debt.

Lenders measure each of the five Cs of credit differently—some qualitative versus quantitative, for example—as they do not always lend themselves easily to a numerical calculation. Creditworthiness is determined by each financial institution in its own way, but most lenders put the most weight on a borrower’s ability to pay back the loan.

Hey there friend! Ever wondered what goes on behind the scenes when you apply for a loan? Whether you’re dreaming of a new ride a cozy home, or just need some extra cash to get by, lenders ain’t just tossing money at ya without a good look under the hood. They’ve got a system, a checklist if you will, called the 5 Cs of lending. These bad boys are the key to whether you get that sweet approval or a big fat “nope.” So, let’s break it down real simple-like and figure out how you can stack the odds in your favor. At my lil’ corner of the internet, we’re all about keepin’ it real and helpin’ you navigate this funky financial maze.

So, what are these 5 Cs of lending? They’re Character, Capacity, Capital, Collateral, and Conditions. Each one’s a piece of the puzzle that lenders use to size up if you’re a safe bet or a risky gamble. Stick with me, and I’ll walk ya through each one, toss in some tips to boost your game, and make sure you’re ready to roll when you hit up that bank or lender. Let’s dive in!

What Are the 5 Cs of Lending? A Quick Rundown

Before we get into the nitty-gritty, lemme give you the quick and dirty on these 5 Cs. Think of ‘em as the five fingers of a hand—each got its own role, but together, they grip that loan decision tight:

- Character: This is all about your rep. Have you been good with money in the past? Paid your bills on time? It’s your financial track record, plain and simple.

- Capacity: Can you handle the payments? Lenders wanna know if your income’s got the muscle to cover what you owe without breakin’ a sweat.

- Capital: What skin you got in the game? This is the cash or assets you’re bringin’ to the table, like a down payment on a house.

- Collateral: Got somethin’ to back up your promise? This is stuff you own that the lender can take if you don’t pay up, like a car or house.

- Conditions: What’s the big picture? Lenders look at why you need the money and what’s goin’ on in the world around ya, like the economy or your job’s future.

Got it? Cool. Let’s look at each of these Cs one by one and break them down so you know what’s going on.

1. Character: Your Money Reputation Matters

First up, we got Character, and no, I ain’t talkin’ about whether you’re a nice person (though that’s cool too) In lending land, Character is all about your financial history It’s how you’ve handled credit before—did ya pay your credit card on time, or are there a bunch of late notices in your past? Lenders dig into your credit report, which is like a report card of your money moves. They check stuff like

- How long you’ve had credit accounts.

- If you’ve missed payments or gone into collections.

- Any big red flags like bankruptcies.

They also peek at your credit score a lil’ number usually between 300 and 850. Higher is better ‘cause it tells ‘em you’re less of a risk. If your score’s in the dumps, they might think twice before handin’ over the dough. I remember when I first checked my score—man, it was a wake-up call! Had to fix a couple o’ mistakes on there to get it lookin’ right.

How to Boost Your Character:

- Check your credit report for free once a year from them big three bureaus. Make sure there ain’t no errors draggin’ ya down.

- Pay bills on time, every time. Set up auto-payments if you gotta—don’t let a forgoten due date mess ya up.

- Keep old accounts open if they’re in good standin’. It shows you’ve got history.

Get this right, and you’re already lookin’ like a solid bet to any lender.

2. Capacity: Can You Swing the Payments?

Next, we got Capacity, which is just a fancy way of sayin’, “Can you afford this loan?” Lenders wanna know if your income can handle the payments without leavin’ ya broke. They look at your job history, how much you make, and somethin’ called your debt-to-income ratio (DTI). That’s just your monthly debt payments divided by your monthly income before taxes. If your DTI is too high—say, over 36% or 43% for some loans like mortgages—they might worry you’re stretched too thin.

Think of it like this: if you’re already jugglin’ a car payment, student loans, and a credit card, addin’ another loan might tip the scales. They wanna see stability—steady income, a solid job, not hoppin’ from gig to gig every other month. I’ve been there, tryin’ to convince a lender I could manage when my paycheck barely covered the basics. It’s tough, but real.

How to Improve Your Capacity:

- Boost your income if you can. Side hustles, freelance gigs—anything steady helps.

- Pay down existin’ debts. Even small chunks off the balance can lower that DTI.

- Avoid takin’ on new debt right before applyin’. Keep that ratio lookin’ nice and low.

Show ‘em you got the cash flow, and they’ll be more likely to say “yes.”

3. Capital: Show Me the Money You’re Puttin’ In

Now let’s chat about Capital. This one’s all about what you’re bringin’ to the table. Lenders love it when you have something to put down as collateral. That way, you’re less likely to back out if things get tough. For instance, if you’re buying a house and can slap down 2020%, they’ll be much happier than if you have nothing to offer up front.

Capital ain’t just for houses, though. It could be savings you’ve built up that show you can cover payments if your income takes a hit. It’s like sayin’, “Hey, I’m invested in this too, so I ain’t gonna flake.” When I was lookin’ at gettin’ a car loan, savin’ up a decent chunk for the down payment made the whole process smoother. Lenders dig that commitment.

How to Strengthen Your Capital:

- Save up for a bigger down payment. Even a lil’ extra can make a difference.

- Keep some emergency cash handy. It shows you’ve got a backup plan.

- Think about timin’. Sometimes buyin’ now with less capital is smarter if the asset’s value is risin’ fast.

More capital, less risk for them. It’s a win-win.

4. Collateral: Got Somethin’ to Back It Up?

Collateral is your safety net—or rather, the lender’s. It’s somethin’ you own that they can take if you don’t pay back the loan. Think of it as a pledge. For a car loan, the car itself is usually the collateral—if you stop payin’, they can repossess it. Same with a mortgage; the house is on the line. This makes the loan “secured,” which is less risky for lenders, so they often offer better rates and terms compared to unsecured loans like credit cards.

But heads up, if you default, you lose that asset. Don’t promise something you can’t stand to give up—it’s a big deal. People have gotten into trouble because they didn’t think about what they were risking. Be smart about it.

How to Use Collateral Wisely:

- Only offer assets you’re okay losin’ if worst comes to worst.

- Make sure the value of your collateral matches the loan amount. They’ll check it.

- Understand the terms—some loans automatically tie to specific stuff, like a car or home.

Collateral can sweeten the deal, but it’s gotta be handled with care.

5. Conditions: What’s the Bigger Picture?

Last but not least, we have Conditions, which is a bit of a surprise. It’s all about “why” and “what’s going on” with your loan. Why do you need the money? Is it a good reason, like getting a car to get to work, or a bad reason, like starting a risky business? Lenders also look at things you can’t change, like the economy, your industry, and even how long you’ve been at your job. If the market is going down or your field is unstable, they might think twice.

Conditions also cover the loan itself—how much you’re askin’ for, the interest rate, and how long you’ll take to pay it back. It’s like they’re checkin’ the weather before decidin’ to sail with ya. I’ve noticed sometimes it ain’t even about you; it’s just bad timin’ in the world. Frustratin’, but real.

How to Work with Conditions:

- Be clear on why you need the loan. A strong purpose can sway ‘em.

- Show your job or industry is stable if you can. Long-term employment helps.

- Stay aware of market vibes. If times are tough, maybe wait it out or adjust your ask.

Conditions might be the least in your control, but a lil’ prep goes a long way.

Why Do the 5 Cs Even Matter?

Alright, so why should you care about these 5 Cs? ‘Cause they’re the gatekeepers to gettin’ that loan you want. Lenders use ‘em to figure out if you’re a safe bet or a headache waitin’ to happen. Nail these areas, and you’re more likely to get approved with better terms—lower interest rates, bigger loan amounts, all that good stuff. Mess up, and you might get stuck with high rates or flat-out denied. We’ve all been there, stressin’ over whether the bank’s gonna give us a shot. Knowin’ these Cs gives you power to prep and shine.

Plus, understandin’ this stuff helps you manage your money better overall. It’s like peekin’ behind the curtain of the financial world. You start seein’ how your choices—like payin’ bills late or savin’ up—impact your future. It’s a game-changer, trust me.

A Quick Cheat Sheet on the 5 Cs of Lending

Wanna quick reference to keep these Cs straight? I gotcha covered with this lil’ table. Keep it handy next time you’re gearin’ up to apply for credit.

| C | What It Means | Why It Matters | How to Improve |

|---|---|---|---|

| Character | Your credit history and reputation | Shows if you’re reliable with money | Check report, pay on time, keep old accounts |

| Capacity | Ability to repay based on income/debt | Proves you can afford payments | Boost income, lower debt, avoid new loans |

| Capital | Money or assets you bring to the deal | Lowers risk with your investment | Save for down payment, keep emergency funds |

| Collateral | Assets backing the loan if you default | Gives lender security, often better terms | Offer valuable assets, understand risks |

| Conditions | Purpose of loan and external factors | Context affects lender’s confidence | Strong purpose, job stability, market timing |

Boom, there it is. Pin this somewhere, ‘cause it’s gold when you’re preppin’ to borrow.

Real Talk: How I’ve Seen the 5 Cs Play Out

Lemme share a quick story from my own life—or at least, close enough to it. A while back, I was tryin’ to get a small loan to fix up some stuff around the house. Thought it’d be a breeze, but nah, got hit with a reality check. My credit history (Character) had a couple dings from some late payments years ago—didn’t think it’d matter, but it did. My income was decent, but with other bills, my Capacity looked tight. Didn’t have much saved up for Capital, and since it wasn’t a secured loan, no Collateral to offer. Plus, the timin’ (Conditions) wasn’t great with some economic jitters goin’ on.

Long story short, I had to hustle. Fixed up my credit by disputin’ an old error, cut down some debts to boost my Capacity, and saved a lil’ extra to show I was serious. Took a few months, but when I reapplied, it was a different story. Got approved with a decent rate. Point is, these 5 Cs ain’t just theory—they’re real, and they hit hard if you ain’t ready.

Practical Steps to Master the 5 Cs Before You Apply

If you’re thinkin’ about applyin’ for a loan soon, don’t just wing it. Here’s a game plan to get your ducks in a row across all 5 Cs. We at this blog wanna see ya win, so take these to heart:

- Start with Character: Pull your credit report now. Fix any mistakes and start buildin’ a habit of on-time payments. Even a few months of consistency can help.

- Check Your Capacity: Figure out your debt-to-income ratio. Add up monthly debt payments and divide by your gross income. If it’s over 36%, work on payin’ stuff down.

- Build Some Capital: Set a goal for a down payment or emergency fund. Even $500 extra can show lenders you mean business.

- Think About Collateral: If it’s a secured loan, know what you’re puttin’ up. Don’t offer somethin’ you can’t lose.

- Understand Conditions: Research the market a bit. If your industry’s shaky or rates are high, maybe hold off or adjust your plan.

Do this prep, and you’re walkin’ into that lender’s office—or website—with confidence. Ain’t no better feelin’ than knowin’ you’ve got your stuff together.

Common Mistakes to Dodge with the 5 Cs

Now, I’ve seen folks trip up on these Cs, so lemme point out some traps to avoid. Don’t make these rookie moves:

- Ignorin’ Your Credit (Character): Thinkin’ past mistakes won’t haunt ya is a big nope. They do, so face ‘em head-on.

- Overestimatin’ Capacity: Be real about what you can pay. Don’t assume a raise is comin’ or bills will magically shrink.

- Skippin’ Capital: Tryin’ to borrow 100% with nothin’ down often looks risky. Save somethin’, even if it’s small.

- Misunderstandin’ Collateral: Pledgin’ stuff without knowin’ the consequences can bite ya. Read the fine print.

- Forgettin’ Conditions: Applyin’ durin’ a recession without a rock-solid reason? Might not fly. Timing matters.

Steer clear of these, and you’ll save yourself a lotta headache.

Wrappin’ It Up: Take Control of Your Lending Game

So, there ya have it—the 5 Cs of lending laid out bare. Character, Capacity, Capital, Collateral, and Conditions ain’t just banker jargon; they’re the blueprint to unlockin’ that loan you’re after. Get a grip on each one, polish up where you’re weak, and walk into any loan application knowin’ you’ve done your part. We’re rootin’ for ya here, ‘cause nothin’ feels better than takin’ charge of your financial future.

Got questions or wanna share how these Cs worked—or didn’t—for you? Drop a comment below. I’m all ears, and let’s keep this convo goin’. Remember, money stuff don’t gotta be scary when you’ve got the know-how. Let’s keep hustlin’ together!

Capital

Lenders also analyze a borrowers capital level when determining creditworthiness. Capital for a business-loan application consists of personal investment into the firm, retained earnings, and other assets controlled by the business owner.

For personal-loan applications, capital consists of savings or investment account balances. Lenders view capital as an additional means to repay the debt obligation should income or revenue be interrupted while the loan is still in repayment.

Banks like people who have a lot of money to borrow because it shows that they have some stake in the game. When borrowers use their own money, they feel like they own the loan, which makes them more likely to pay it back. Banks measure capital quantitatively as a percentage of the total investment cost.

Character

Character refers to a borrowers reputation or record regarding financial matters. The old saying that past behavior is the best indicator of future behavior is one that lenders live by.

Each has its own formula or approach for determining a borrowers character, honesty, and reliability, but this assessment typically includes both qualitative and quantitative methods.

As part of the character check, a lender will likely review the applicants credit history or score, which credit reporting agencies standardize to a common scale.

If a borrower has not managed past debt repayment well or has a previous bankruptcy, their character is deemed less acceptable than a borrower with a clean credit history.

What are the 5 Cs of Credit?

FAQ

What are the 5c principles of lending?

Character, capacity, capital, collateral and conditions are the 5 C’s of credit. Lenders may look at the 5 C’s when considering credit applications. Understanding the 5 C’s could help you boost your creditworthiness, making it easier to qualify for the credit you apply for.

What are the 5 cs and explain them all?

The 5 Cs of Credit analysis are – Character, Capacity, Capital, Collateral, and Conditions. They are used by lenders to evaluate a borrower’s creditworthiness and include factors such as the borrower’s reputation, income, assets, collateral, and the economic conditions impacting repayment.

What are the five cs used by lending institutions?

What are the 5 P’s of lending?

It talks about each of the Five Ps: People is about the borrower’s character and reputation, Purpose is about how the money will be used, Payment is about where the money will come from to pay back the loan, Plan is about how the loan will be supervised and what will happen if the borrower doesn’t pay, and Protection is about collateral and other ways to pay back the loan.