Hey there folks! Ever been scrollin’ through car ads or dreamin’ about a new ride only to see those sweet deals tagged with “for highly qualified buyers only”? Man, it stings when you ain’t sure if that’s you. Or maybe you’re eyeing a big purchase—house, car, whatever—and wanna know how to get the best loan terms out there. Well, stick with me, ‘cause today we’re diving deep into what is a highly qualified loan, why it matters, and how you can work your way into that elite club. Let’s break it down real simple, no fancy banker talk, just straight-up advice from yours truly at [Your Company Name].

So, What Is a Highly Qualified Loan, Anyway?

Alright, let’s cut to the chase A highly qualified loan ain’t some mysterious unicorn—it’s just a loan with the best rates and terms that lenders save for their “golden child” borrowers These are the folks who’ve got their financial ducks in a row, makin’ lenders feel all warm and fuzzy about givin’ them money. Basically, if you’re a highly qualified buyer, you’re seen as low-risk. That means lower interest rates, easier approvals, and sometimes even special offers that regular folks don’t get.

But here’s the kicker to get tagged as “highly qualified” you gotta meet some strict criteria. Lenders ain’t just handin’ out these deals to anyone with a heartbeat. They’re lookin’ at your credit score your debt situation, and a few other things to decide if you’re the real deal. Don’t worry, though—I’m gonna walk ya through each piece of this puzzle so you know exactly where you stand.

Why Should You Care About Bein’ Highly Qualified?

Before we dig into the nitty-gritty, let’s talk about why this even matters. Picture this: you’re buyin’ a car for $30,000. If you’re highly qualified, you might score a loan with a 2% interest rate. Someone who ain’t? They could be stuck with 6% or higher. Over a 5-year loan, that’s thousands of bucks in extra interest! Same goes for mortgages or other big loans—bein’ highly qualified saves you serious cash and hassle.

Plus, it’s not just about money. It’s about options. For these buyers, lenders roll out the red carpet and offer perks like faster approvals or better terms for paying back the loan. Getting into this group is a game-changer, whether you want a brand-new truck or just to refinance something.

The Big Three: What Makes You Highly Qualified?

Now, let’s get into the meat of it. Lenders usually look at three main things to figure out if you’re worthy of a highly qualified loan. I’ll break ‘em down real easy, with some examples to make it stick.

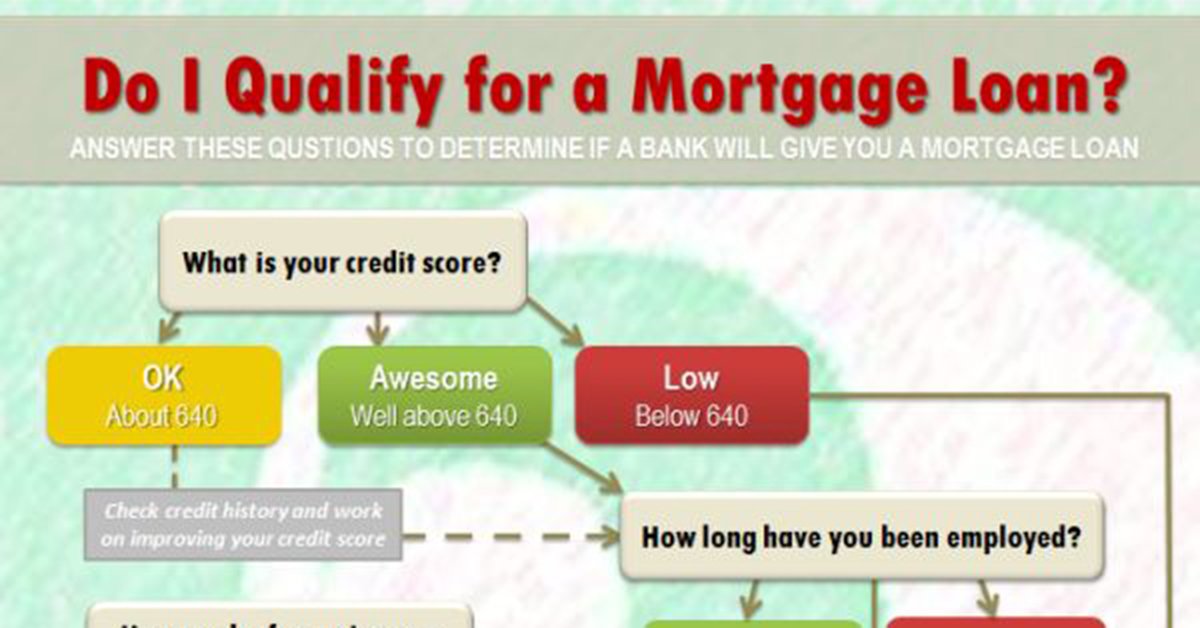

1. Your Credit Score—It’s Kinda a Big Deal

First up, your credit score. This is like your financial report card, and lenders are obsessed with it. For a highly qualified loan, you usually need a score that’s top-notch—think 720 or higher, sometimes even 740 to 850. That range is often called “prime” or “super prime,” meanin’ you’ve been super responsible with credit in the past.

- Why it matters: A high score tells lenders you pay bills on time and don’t mess around with debt. They trust ya!

- What if yours ain’t great?: Don’t sweat it yet. I’ll share tips later on boostin’ that number.

For example, if Sally’s got a score of 780, she’s golden. But if Joe’s sittin’ at 650, he might not get the best rates. It’s harsh, but that’s how it rolls.

2. Debt-to-Income Ratio (DTI)—How Much Debt You Carryin’?

Next, there’s somethin’ called your Debt-to-Income ratio, or DTI. Fancy name, simple idea: it’s how much of your monthly income goes to payin’ off debt. Lenders want this number balanced, ideally around 50% or less. You figure it out by dividin’ your monthly debt payments by your gross monthly income (that’s before taxes, y’all).

- How to calculate: Say you pay $1,500 a month on debt (credit cards, loans, etc.), and you make $3,000 before taxes. Your DTI is 50% ($1,500 ÷ $3,000). That’s okay, but lower is better.

- Why they care: If too much of your cash is tied up in debt, lenders worry you won’t handle a new loan.

If your DTI is creepin’ up high, it’s a red flag. Lenders like seein’ you’ve got room in your budget for their payments.

3. Payment-to-Income Ratio (PTI)—Debt Payments vs. Income

Then there’s the Payment-to-Income ratio, or PTI. This one is a bit different from DTI because it shows how much of your monthly income goes to paying off debt. Lenders often want this below 20%. To find it, divide your monthly debt payments by your gross income and then multiply by 100 to get a percentage.

- Quick math: Usin’ the same numbers, $1,500 in debt payments on $3,000 income is 50% DTI, but for PTI, they might focus just on certain payments. Still, keepin’ it low—like under 20%—is ideal.

- What it means: A low PTI says you’ve got plenty of income left after debt to cover livin’ expenses and new loans.

This one’s a bit less talked about, but it’s still on lenders’ radar, especially for stuff like car loans.

Bonus Factors: What Else Might Tip the Scales?

Credit score, DTI, and PTI are the big three. But lenders sometimes peek at other stuff too. Here’s a quick rundown:

- Employment History: Got a steady job with a solid company? That’s a plus. It shows you’ve got reliable income.

- Savings and Investments: If you’ve got a nice chunk saved up or some investments, it screams “I’m financially stable!” to lenders.

- Collateral: Offerin’ somethin’ valuable—like a car or house—as backup for the loan can sweeten the deal. It’s like sayin’, “If I can’t pay, take this instead.”

These ain’t always required, but they can nudge you closer to that highly qualified status.

A Quick Cheat Sheet: Are You Highly Qualified?

Here’s a little table to sum up what lenders might look for. Keep in mind, every bank or lender might tweak these numbers a bit, but this is a solid startin’ point.

| Factor | Ideal Range for Highly Qualified | Why It Matters |

|---|---|---|

| Credit Score | 720+ (often 740-850) | Shows you’re trustworthy with money. |

| Debt-to-Income (DTI) Ratio | Around 50% or less | Proves you ain’t drowning in debt. |

| Payment-to-Income (PTI) | Below 20% | Means you’ve got income to spare. |

| Employment History | Stable, long-term | Confirms steady cash flow. |

| Savings/Investments | Decent amount | Shows financial backup. |

| Collateral | Valuable asset if offered | Reduces lender’s risk. |

If you’re getting most of these, good luck—you’re probably going to get a great loan!

But What If You Ain’t There Yet? Don’t Panic!

Look, I get it. Not everyone’s got a perfect credit score or zero debt. Heck, I’ve been there myself, wonderin’ if I’d ever qualify for the good stuff. The truth is, bein’ a highly qualified buyer ain’t a destination you reach overnight—it’s a journey. And even if you’re not quite there, lenders or dealers can still work with ya to find somethin’ that fits.

The good news? You can improve your odds over time. Let me share some real-talk tips that helped me and plenty of others move the needle.

Tips to Boost Your Chances of Gettin’ a Highly Qualified Loan

- Pay Them Bills on Time, Every Dang Time: This is huge for your credit score. Set reminders, automate payments—whatever it takes. Late payments are like kryptonite to your score.

- Keep Credit Use Low: Don’t max out your cards. Aim to use less than 30% of your available credit. So, if you’ve got a $10,000 limit, keep the balance under $3,000.

- Tackle That Debt: Focus on high-interest stuff first, like credit cards. Payin’ it down lowers your DTI and makes you look better to lenders.

- Build Up Some Savings: Stash away at least 3-6 months of livin’ expenses. It’s a safety net, and lenders dig that.

- Stick to a Job: If possible, build a steady work history. Jumpin’ around too much can spook lenders.

- Dip Into Investments: If you’ve got extra cash, consider some safe investments. It shows you’re thinkin’ long-term.

These steps ain’t quick fixes, but they add up. I remember when I started payin’ off my credit card debt—felt like climbin’ a mountain. But each payment got me closer to better loan options.

Where Do Highly Qualified Loans Pop Up Most?

You might be wonderin’, “Okay, but where do I even see these loans?” Fair question. They’re super common in auto financing—think car dealerships offerin’ 0% interest or crazy low rates to buyers with top-tier credit. But they ain’t limited to cars. You might see similar deals for mortgages, personal loans, or even business financing. Anytime a lender’s got a “special offer for qualified buyers,” they’re talkin’ about this crew.

For example, when I was shoppin’ for a car a while back, the dealer had this amazin’ low-rate offer, but only for folks with a credit score over 740. I wasn’t there yet, but it lit a fire under me to get my finances in shape.

What’s the Catch? Ain’t Nothin’ Perfect

Now, let’s keep it real—there’s always a flip side. Even if you’re highly qualified, you might not get every deal out there. Some offers depend on the lender’s rules, the type of loan, or even just dumb luck. And if you’re not in that elite group yet, you might face higher interest or stricter terms. That’s just how the game works.

But here’s the thing: even if you don’t qualify right now, most lenders or dealers wanna help. They’ve got options for all kinds of credit backgrounds. So don’t be shy—reach out and see what’s on the table.

A Personal Story: My Own Road to Better Loans

Lemme share a quick story. A few years back, I was nowhere near “highly qualified.” My credit was decent, but not great, and I had some debt from school loans hangin’ over me. I wanted a new car, but the interest rates they offered were brutal. So, I got to work—paid down debt, kept my credit card use low, and made sure every bill was on time. Took about a year, but my score jumped up, and my DTI got way better. Next time I applied for a loan, bam—way better terms. Felt like winnin’ the lottery!

Point is, it’s doable. You just gotta commit to the grind.

Common Questions About Highly Qualified Loans

I know y’all might have some lingerin’ thoughts, so let’s hit a few FAQs I’ve heard over the years.

- What’s the minimum credit score for a highly qualified loan? Usually 720 or higher, but some lenders might want 740 or more. It varies, so check with who you’re borrowin’ from.

- Can I still get a loan if I’m not highly qualified? Heck yeah! You might not get the best rates, but there’s plenty of options out there for all credit levels.

- How long does it take to improve my status? Depends on where you’re startin’. Boostin’ a credit score or payin’ debt can take months or years, but every step counts.

- Are these loans only for cars? Nah, they pop up for mortgages, personal loans, and more. Auto loans just advertise ‘em a lot.

Final Pep Talk: You’ve Got This!

So, now you know the deal with what is a highly qualified loan. It’s all about bein’ a low-risk borrower with a stellar credit score, manageable debt, and financial stability. It ain’t just a label—it’s your ticket to savin’ money and gettin’ the best deals lenders have to offer. And if you’re not there yet, no biggie. Take it one step at a time, use the tips I shared, and keep pushin’ forward.

Here at [Your Company Name], we’re rootin’ for ya. Got questions or wanna chat more about gettin’ your finances loan-ready? Drop us a line anytime. Let’s turn those dreams—whether it’s a new car, home, or somethin’ else—into reality, one smart move at a time.

Keep hustlin’, and remember: the road to bein’ highly qualified starts with believin’ you can get there. Catch ya later!

Is it hard to get approved for Toyota financing?

If your credit score isn’t Tier 1, there’s no reason to despair. Our Toyota dealership in Columbus, Ohio works with customers of all credit backgrounds. To qualify for Toyota finance, your credit score should be at least 610. Customers with lower credit scores will generally get higher interest rates. The most appealing financing offers are typically reserved for those “well-qualified buyers”!.

How long does Toyota Finance take to approve?

After your application is received by our Toyota dealership in Columbus, Ohio, we’ll work hard to get you an answer as quickly as possible. Our Toyota finance team works directly with Toyota lenders to approve customers within three business days.

Do not worry if you are not able to get Toyota financing. Toyota Direct also offers in-house financing for people with bad credit. We make it easy for anyone to finance a car, whatever their situation might be. For more information on our bad credit car loans, just contact your friends at Toyota Direct!.