Withdrawing funds from your 401(k) retirement account is a major financial decision that requires careful consideration. Many people wonder if tapping into their 401(k) could negatively impact their credit score.

The short answer is no, taking money out of your 401(k) does not have an effect on your credit score or show up on your credit report.

However, there are some important caveats to understand before deciding to take money out of your retirement savings. In this detailed guide, we’ll cover:

- How 401(k) loans and withdrawals differ from traditional credit

- Key factors that determine credit reporting

- Common 401(k) withdrawal mistakes to avoid

- Pros and cons of using 401(k) funds to pay debts

- Alternatives to preserve your retirement and credit

Let’s dive in,

Why 401(k) Withdrawals Don’t Hurt Your Credit

The reason a 401(k) withdrawal doesn’t show up on your credit report boils down to what credit reports actually track.

Your credit reports (at Equifax, Experian, and TransUnion) record information related to:

- Credit card accounts

- Loans from banks/lenders

- Payment history

- Delinquencies

- Bankruptcies

- Other credit obligations

A 401(k) retirement account does not fall into any of those categories. It’s not a loan from an outside lender or creditor. When you withdraw from your 401(k), you’re taking your own money out of your own account.

So 401(k) withdrawals simply do not get reported to the credit bureaus for inclusion on your credit reports. There’s no debit, no new account, no change in your outstanding debts from the perspective of credit scoring models.

That’s why 401(k) loans or withdrawals have no direct impact on your credit scores. The money is moving within your own retirement system, not from or to an external creditor.

Key Factors That Determine Credit Reporting

To fully grasp why 401(k)s are invisible to credit scoring, it helps to understand what does (and doesn’t) influence your credit reports and FICO/VantageScore numbers.

Here are some key categories that make up your credit reports:

-

Payment history – Records of on-time or missed payments for credit accounts (like credit cards, student loans, mortgages). A 401(k) withdrawal obviously has no payment history.

-

Credit utilization tells you how much of your available credit you’re actually using. 401(k) balances don’t count here.

-

Credit age/history – Length of time credit accounts have been open. 401(k)s don’t have an “open date” that ages like a credit account.

-

When you apply for new credit, keep track of the credit checks that were done. There is no application for your own 401(k).

-

The different types of credit accounts that show up on your report, like credit cards, installment loans, mortgages, and so on. A 401(k) is not considered a credit account.

As you can see, 401(k) activity simply doesn’t apply when calculating standard credit scores. There’s no payment data, no utilization ratio, no history length or new inquiries to factor in.

That’s why withdrawing any amount from your 401(k) has no direct credit impact. As far as credit reports and scores are concerned, it’s like the withdrawal never happened.

401(k) Withdrawal Pitfalls to Avoid

While 401(k) withdrawals don’t hurt your credit, that doesn’t make them completely risk-free. Here are some common mistakes to keep in mind:

-

Withdrawing too much too fast – Taking large lump sums can severely reduce your retirement savings. Avoid draining your 401(k) unless absolutely necessary.

-

Frequent withdrawals – Repeatedly tapping your 401(k) can significantly limit its growth. Look for alternatives before making it a habit.

-

Failing to repay 401(k) loans – Defaulting on a loan turns into a withdrawal. Be sure you can repay 401(k) loans on schedule.

-

Job changes – Leaving your employer can accelerate repayment deadlines. Have a plan to quickly repay any outstanding 401(k) loan balance.

-

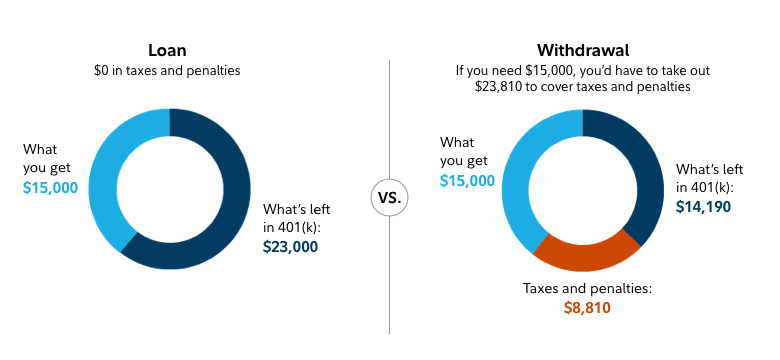

Withdrawal penalties – Those under age 59.5 face a 10% penalty on most 401(k) withdrawals on top of income taxes. Factor this into your decision.

The bottom line is to weigh the pros and cons carefully, and explore other options before withdrawing from your retirement funds if possible. A 401(k) withdrawal should be a last resort, not a convenience.

Can a 401(k) Withdrawal Help Your Credit Indirectly?

Using 401(k) funds to pay off debts like credit cards or personal loans can positively impact your credit scores indirectly.

Here’s how it works:

If high credit card balances are dragging down your credit score due to high utilization, paying off those cards with a 401(k) withdrawal would lower your utilization ratio.

That credit card debt payoff could potentially boost your credit scores over time as your utilization drops. But again, the 401(k) withdrawal itself is never visible to or recorded by the credit bureaus.

The score improvement happens because paying off credit card balances decreases your overall credit utilization across accounts. It alters revolving credit balances, a key factor in credit scores.

So in cases where heavy credit card debt is damaging your credit, a 401(k) withdrawal could help indirectly by letting you pay down those balances. But you can achieve the same result without touching retirement funds by paying off cards through other means.

Alternatives to Preserve Your Credit and Retirement

While 401(k) withdrawals don’t hurt your credit, they can still damage your long-term retirement readiness. Here are some options to consider before withdrawing funds:

-

401(k) loans – Borrowing from your 401(k) avoids penalties and taxes as long as you repay on schedule. This keeps more money invested compared to withdrawals.

-

Consolidation loans – Combines high-interest debts under a single lower fixed rate loan. Helps pay off cards faster without tapping retirement funds.

-

Balance transfers – Shifts credit card balances to a new card with a 0% intro APR to avoid interest (for a limited time).

-

Budgeting apps – Managing spending can help free up more cash to pay down debts without 401(k) withdrawals.

-

Credit counseling – Non-profit agencies provide free education and advice on reducing and repaying debts.

The key takeaway? While 401(k) withdrawals won’t hurt your credit score, they can carry other risks. Seek alternatives when possible, and only use 401(k) funds as an absolute last resort to preserve your retirement savings.

Frequently Asked Questions

Does a 401(k) withdrawal count against you when applying for a mortgage?

No, the withdrawal itself doesn’t show up on credit reports that mortgage lenders review. However, some may ask for clarification or documentation on large deposit amounts they see in your bank statements.

Can multiple 401(k) withdrawals hurt your credit?

Still no direct credit impact, even after multiple withdrawals. But ongoing withdrawals will erode your retirement funds over time.

Is it better for my credit to borrow from my 401(k) instead of withdrawing?

Technically neither affects your credit positively or negatively. But a 401(k) loan preserves your savings balance better since you repay the funds.

What if I withdraw from my IRA instead of my 401(k)?

Same outcome: no direct credit impact. IRAs function similarly for credit reporting. The withdrawal won’t help or hurt scores.

Does a 401(k) withdrawal require your credit to be checked?

Nope, you don’t need a credit check or qualify based on creditworthiness to withdraw your own 401(k) money. The withdrawal process has no connection to your credit reports or scores.

The Bottom Line

While 401(k) withdrawals make no direct appearance on your credit, think carefully before using retirement funds to pay debts. Preserving your 401(k) balance should take priority unless you’ve exhausted all other options.

If you do need to withdraw, be strategic – carefully calculate tax impacts and avoid penalties. With smart planning, you can protect both your credit and your retirement savings over the long haul.

Why Nitzsche used his 401(k) to pay off credit card debt

Nitzsche speaks from experience. He is 40 now and a self-proclaimed “credit junkie” with a credit score over 800, but in 2008 when he was in his twenties and laid off from his job, he was burdened with having to pay a mortgage on a new home, just over $20,000 in student loans and over $10,000 in credit card debt.

He made some lifestyle changes, such as having three others live in his St. Louis, MO, home at the time to split mortgage and utility payments. But one of the biggest decisions he made was completely tapping into his retirement savings — what he estimates was about $20,000 at the time — to pay off his credit cards. Nitzsche tells Select that it was a decision he likely would not make again.

“That decision was largely done out of just panic and prioritizing,” Nitzsche says. “I knew I had to do everything I could to keep my house because I had just bought it a year before and naturally took a lot of pride in being a homeowner.” “.

But it’s been more than ten years, and Nitzsche is still feeling the effects of his choice. He’s not sure if he would tell someone else in the same situation to do what he did.

Why he doesn’t recommend you do an early withdrawal

Looking back, Nitzsche says that liquidating his 401(k) to pay off credit card debt is something he wouldnt do again.

“It is so detrimental to your long-term financial health and your retirement,” he says.

Many experts agree that tapping into your retirement savings early can have long-term effects. It can put you at risk later in life when you are older, don’t have a job, and would need those funds.

There are also short-term effects from making an early withdrawal from your 401(k) as well: It doesnt come free. Doing so has costly consequences, including both a penalty fee and taxes. For borrowers 59½ years old and younger, there is generally an early withdrawal penalty of 10%, plus taxes, which can be anywhere from 20% to 25% depending on your income and tax bracket.

If you are someone who is cash-strapped during this time of uncertainty, tapping into your retirement savings is an option of last resort. “That really should not have been touched and not something we would usually advise somebody to do,” Nitzsche says.