Millions of people in the UK are struggling with personal debt. It’s more important than ever to understand the size and effects of personal debt in a time when living costs are going up and the economy is uncertain. This article will give you a full picture of the latest data and trends on the average amount of personal debt in the UK.

Key Statistics on Personal Debt in the UK

-

The total amount of personal debt owed by people in the UK is £1.84 trillion as of June 2023. This includes secured lending like mortgages and unsecured borrowing like credit cards and overdrafts.

-

The average total debt per UK adult is £34,597. This includes an average mortgage debt of £30,574 and average unsecured debt of £4,022.

-

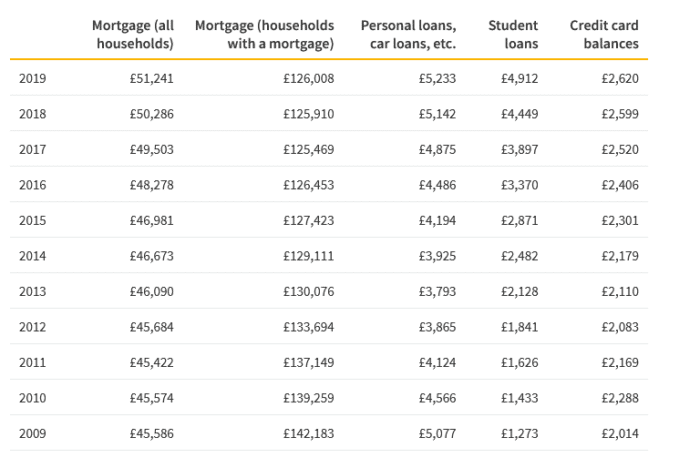

Looking just at unsecured debt, the average UK adult owes £1,241 on credit cards

-

On average, every UK household owes £65529 in total debt. It’s made up of £5,7910 in secured loans and £7,619 in unsecured loans.

-

There were 112,575 individual insolvencies in England and Wales in the 12 months leading to June 2023. This equates to 298 people going insolvent every day.

-

3% of UK adults report borrowing over £10000 more in 2022 compared to 2021.

Trends in Personal Debt Levels

Looking at trends over recent years shows that personal debt levels have steadily risen in the UK:

-

Total UK personal debt increased from £1.8 trillion in 2022 to £1.84 trillion in 2023. That’s an extra £40 billion in debt over just one year.

-

Between 2021 and 2022, there was a £498 increase in debt per adult in the UK.

-

Credit card borrowing saw a sharp annual growth rate of 13% in July 2022. This was the highest growth since 2005.

-

Around 11% of UK consumers say they are using credit more than usual in 2022. This suggests people are increasingly relying on credit to get by.

-

Official predictions forecast that average household debt could reach £82,641 by 2025.

So the data clearly shows that personal debt levels are on an upward trajectory in the UK. This is likely being driven by the cost of living crisis placing increasing pressure on households.

Regional Differences in Debt Levels

It’s important to understand that debt levels around the UK are not uniform. There are significant regional variations:

-

London and the South East have the highest average debt levels, at around £60,000 per household.

-

Scotland, Wales, and Northern Ireland have the least amount of debt, with each household owing between £40,000 and £44,000

-

Areas with larger cities tend to have higher debt. For example, the average debt in Greater Manchester is £52,000.

-

Poorer regions like the North East have lower debt at £48,000 per household. But this is still high relative to average earnings.

So while debt levels are high nationally, the problem is generally more acute in wealthier parts of the country. However, poorer households often struggle more to repay debts relative to incomes.

Debt Demographics: Age, Gender and Income

-

Younger adults have the most debt as a percentage of income, at over 110%. Debt-to-income ratios decline steadily with age.

-

25-44 year olds are the most likely age groups to have some form of consumer credit. 71% of 25-34 year olds have credit, compared to just 20% of over 65s.

-

Men have higher average debts than women, owing £2,800 in unsecured debt compared to £1,800 for women.

-

But women are more likely to say they are using credit more than usual, by a margin of 13% to 10%.

-

Higher income households owe substantially more in mortgages and student loans. But lower income groups struggle more to repay debts relative to disposable income.

So while young people have high relative debt levels, it is high income households that owe the most in absolute terms. And deprived groups face the toughest challenges with repayment.

Main Causes of Rising Personal Debt

Several factors have driven the steady rise in personal debt across the UK in recent years:

-

Stagnant wage growth combined with rising living costs has increased reliance on credit just to get by.

-

Higher housing costs have caused mortgage sizes to increase, in turn raising total household debt.

-

Cuts to benefits and public services have also added pressure on finances and forced more borrowing.

-

Student loans are contributing to high debt levels for younger adults.

-

Unemployment remains a key cause of debt problems when incomes are lost.

-

Low financial literacy and an increase in predatory lending has also enabled excessive borrowing.

So while borrowing is sometimes necessary or sensible, changes to the economy and public policy have undoubtedly increased the debt burden on UK households over the past decade.

Consequences of High Personal Debt

The high and rising levels of personal debt in the UK do not come without consequences:

-

High debt repayments reduce disposable incomes and therefore spending in the wider economy.

-

It leaves households very vulnerable to income shocks, with little savings to fall back on.

-

The risk of falling into arrears and eventual insolvency is increased.

-

Mental health can be affected by debt problems, especially when severe.

-

Financial exclusion and poverty become more likely due to reliance on high-cost credit.

-

Low-income households face the worst consequences, increasing inequality.

So debt is not just a financial issue but can have far-reaching impacts on wellbeing, poverty, inequality and the broader economy. Urgent action is required to tackle the UK’s debt problem.

This article has provided an in-depth overview of the latest statistics and trends related to personal debt levels in the UK. To conclude:

-

Total personal debt is very high at £1.84 trillion and rising rapidly.

-

Average per adult debt stands at around £34,597, most of which is mortgage lending.

-

Unsecured borrowing like credit cards and loans is growing quickly.

-

London and the South have the most debt, but poorer areas struggle more with repayments.

-

Younger adults and high-income households owe the most in absolute terms.

-

Stagnant incomes, rising costs and cuts to services are fuelling debt increases.

-

High debt has damaging consequences for people, communities and the economy.

Tackling problem debt must be made a priority. Greater financial education, regulation of irresponsible lending, and more comprehensive debt advice services can help address the UK’s debt crisis. But addressing the root economic causes is equally important for creating a more financially secure society.

You aren’t alone in your debt

Personal debt in the UK has been steadily rising, reflecting broader economic challenges and individual financial pressures.

This marked an increase of £205 million compared to May 2023, adding an extra £275. 94 of debt per adult. These figures highlight that personal debt in the UK is a growing concern for individual and households.

On a per-household basis, the average debt, including mortgages, stood at £65,239. So, the average amount of debt for adults was £210,934,537% of their average yearly income in the UK. This means that the typical adult in the UK owes nearly as much as they earn in a year, creating a cycle of debt that is almost impossible to break.

What’s The Average Personal Debt in the UK?

FAQ

What is the average debt per person in the UK?

The average total debt per household, including mortgages, was £65,143. Per adult this was £34,487, around 97. 0% of average earnings. This is up from the revised £34,370 a month earlier.

What is considered high debt in the UK?

Generally, high debt in the UK is defined as a debt-to-income ratio of over 50%. This means an individual uses over 50% of their income for debt repayments. If you fall into this category, you will likely face: Persistent difficulty in meeting minimum payments.

How much does an average person have in debt?

According to Experian, average total consumer household debt in 2024 is $105,056. That’s up 13% from 2020, when average total consumer debt was $92,727.

What is the average credit card balance in the UK?

The average credit card balance in the UK is £1,675, as of May 2023. 78% of UK adults have at least one form of consumer credit. Individuals collectively borrowed a net £0. 6 billion on credit cards, in July 2022. 21. 6 million in the UK used cash either once a month or not all, in 2022.