Sales Ledger Control Account is a summary account which checks the arithmetical accuracy of the Sales Ledger. With this, we can quickly check if the general ledger balance for the sales ledger matches the sum of all the trade receivable accounts in the sales ledger.

The Sales Ledger Control Account is like a “T-Account” or a copy of an Individual Trade Receivable (Debtor) account. But instead of having transactions for a single trade receivable (Debtor), it has transactions for all of the business’s trade receivables (debtors). As this control account contains the summarized information of all the trade receivables accounts in the sales ledger, it is also called as “Total Trade Receivables Account”(“Total Debtors Account”).

Look at how this control account is set up below and try to figure out what it has in common with an individual trade receivable account (also known as a debtors account).

Sales ledger control account is generally prepared at the end of the financial year or “whenever” it is required to check the arithmetical accuracy of the individual trade receivable accounts.

As we discussed earlier, this control account is prepared as an independent check on the arithmetical accuracy of the sales ledger (Debtors Ledger). So, we should not obtain the information required to prepare this control account from the Sales ledger (Debtors ledger), instead all the information required should be obtained from books of original entry or prime entry.

Giving customers credit is something that many businesses do. But this also puts them at risk of bad debts, which are amounts owed by customers that can’t be met. It’s important to keep track of these bad debts and write them off in the sales ledger when you’re managing credit sales. This detailed guide will show you what bad debts are, why you need to get rid of them, and how to do it in the sales ledger step by step.

What are Bad Debts?

Bad debts refer to accounts receivable owed by customers that are deemed uncollectible. There are several situations in which bad debts can arise:

-

The customer goes bankrupt or goes into liquidation

-

The customer disappears without paying their dues.

-

There are disputes or legal issues that make the amount unrecoverable

-

The customer is facing financial difficulties and is unable to pay.

It is thought that these debts are “bad” because it is unlikely that the money will be paid back. They should be separated from doubtful debts, which can be collected but aren’t certain to do so.

Why Write Off Bad Debts?

Businesses should get rid of bad debts in their books for a number of important reasons:

-

To reflect accurate financial position: Keeping uncollectible amounts in accounts receivable overstates the assets and revenue of the business. Writing off bad debts ensures the financial statements reflect the true picture.

-

The matching principle says that expenses should be recorded in the same accounting period as the related income. Bad debt write-offs allow this.

-

Tax benefits: Written off bad debts can be claimed as tax deductions in many jurisdictions, providing tax benefits to businesses.

-

Credit control: Identifying and writing off bad debts helps identify problem accounts and informs credit policies.

-

Accounting standards: GAAP and IFRS standards mandate bad debt write-offs when they are identified.

Methods for Estimating Bad Debts

Before writing off individual bad debts, businesses need to estimate the amount of bad debts expected in a period. This is done via:

-

Percentage of sales method: A set percentage of net credit sales is set aside as provision for bad debts, based on past experience.

-

Aging method: Accounts receivable balances are categorized by age. A higher percentage is applied to older outstanding amounts.

Recording Bad Debts Written Off in Ledger

There are two key steps to writing off bad debts in the accounting records:

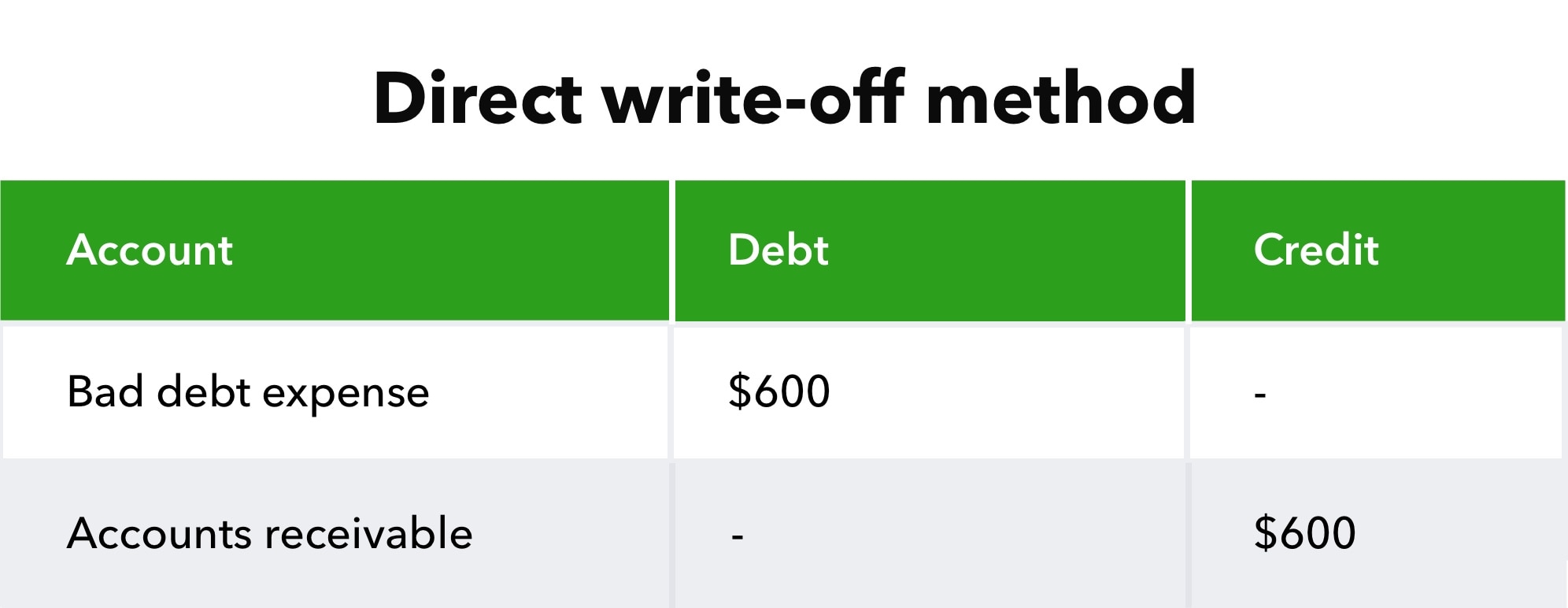

1. Journal Entry to Write Off Bad Debt

Once a debt is confirmed as uncollectible, it needs to be removed from accounts receivable via a journal entry:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Date | Bad Debt Expense | x | |

| Date | Accounts Receivable – Customer | x |

This entry removes the amount from accounts receivable and records it as an expense.

2. Ledger Account Postings

The journal entry then needs to be posted to update the ledgers:

-

Bad Debt Expense ledger is debited with the write-off amount

-

The individual Accounts Receivable ledger for that customer is credited with the amount written off

This reduces the customer’s outstanding balance to zero and removes the amount from accounts receivable.

Example of Writing Off a Bad Debt

Let’s see how this works with an example:

- On 1 Jan, ABC Co. made a credit sale of $1,000 to Customer A

- On 31 Jan, ABC Co. determines Customer A’s debt of $1,000 is uncollectible.

- They pass a journal entry writing off the bad debt:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Jan 31 | Bad Debt Expense | 1,000 | |

| Jan 31 | Accounts Receivable – Customer A | 1,000 |

- This is posted to the ledgers:

Bad Debt Expense Ledger

| Date | Description | Debit | Credit | Balance |

|---|---|---|---|---|

| Jan 31 | Bad debt write-off – Customer A | 1,000 | 1,000 |

Accounts Receivable – Customer A

| Date | Description | Debit | Credit | Balance |

|---|---|---|---|---|

| Jan 1 | Credit sale | 1,000 | 1,000 | |

| Jan 31 | Bad debt write-off | 1,000 | 0 |

- Customer A’s balance is now zeroed out after the write-off.

Recovery of Bad Debts

In some cases, bad debts originally written off may be subsequently recovered if the customer makes a payment. These recoveries are recorded as follows:

- The amount recovered is credited to Bad Debts Recovered account

- Bad Debt Expense account is debited with the same amount

- No sales ledger account is involved in this entry

Recovered amounts directly increase the income for the period.

Impact on Financial Statements

-

Income Statement – Bad debt expense reduces net income in the period of write-off. Recovered bad debts are added to net income.

-

Balance Sheet – Writing off bad debts reduces accounts receivable and total assets.

Proper recording of bad debts and any related recoveries is vital for accurate financial statements.

Writing off bad debts is an essential accounting process for any business providing credit sales. By promptly identifying uncollectible accounts and removing them from the sales ledger, companies can maintain up-to-date records that properly reflect income and assets. The process requires careful analysis of accounts receivable, appropriate journal entries, and accurate ledger postings. Automating ledger postings and credit control procedures can help streamline bad debt write-offs.

How to check the arithmetical accuracy of the sales ledger:

Once the control account is prepared using the above format with the information obtained from various books of prime entry/original entry, the total of balances on the individual trade receivable accounts in the sales ledger should match with the closing balances on the Sales ledger control account.

If the closing balances of sales ledger control and the total of balances on the individual trade receivable accounts in the sales ledger agrees, we can presume that there are no errors or fraud occurred in the sales ledger. If the balances are different, it means there are mistakes in the sales ledger or control account for each trade receivables account. So to locate these errors, accountants need to check each and every trade receivables account in the sales ledger carefully until the error is found or the fraud is detected.

Source of information for Sales Ledger Control Account:

The following table provides the details of source of information for the sales ledger control account items.

|

S.No |

Item |

Source of information |

|

1. |

Opening trade receivables (opening debtors) |

Total of Trade Receivable balances at the end of the previous accounting period. |

|

2. |

Credit Sales |

Total Credit Sales from the Sales Day Book (Sales Journal). |

|

3. |

Sales returns (Return inwards) |

Total sales returns from the Return Inwards Day book (Sales returns journal). |

|

4. |

Cash received |

From the cash column on the debit side of the Cash Book. |

|

5. |

Cheques received |

From the bank column on the debit side of the Cash Book. |

|

6. |

Discount allowed |

Total of the Discount column on the debit side of the Cash book. |

|

7. |

Bad debts written off |

From the the Journal (Proper Journal). |

|

8. |

Dishonored cheques |

From the bank column on the debit side of the Cash book. |

|

9. |

Refunds to trade receivables |

From cash/bank column on the credit side of the Cash book. |

|

10. |

Set off (Transfer to Purchases ledger) |

From the Journal (Proper Journal). |

|

11. |

Interest charged on overdue accounts. |

From the Journal (Proper Journal). |

|

12. |

Closing Trade receivables (closing debtors) |

Total of Trade Receivable balances at the end of the current accounting period. |

Irrecoverable Debts And The Ledger Accounts

FAQ

What is bad debts written off in ledger?

A dealer may write-off the whole or partial value of sales to a particular customer as bad debt. There should be no more bad debts, and the purchase values should be moved to the expense account. The amount of tax included in such sale value can be claimed as a deduction by the dealer.

How to record bad debts written off?

In the journal entry, debit the bad debt expense and credit allowance for doubtful debt accounts. When writing off an account, debit allowance for doubtful accounts and credit the receivable account.

Where does bad debts go in sales ledger control account?

Contra entries in a sales ledger control account usually include credit notes given to customers who paid over time, write-offs for bad debts or debts that aren’t clear, and receipts for cash purchases. These entries also cater to situations where interest charged on overdue accounts needs to be accounted for.

Which ledger account do I use to write-off a bad debt?

Bad Debt Direct Write-Off Method The method involves a direct write-off to the receivables account. With the direct write-off method, bad debt expense is a direct loss from uncollectibles. This loss goes against revenues, which lowers your net income.