At Upstart, we believe you’re more than your credit score. Your credit score is simply a number based on the information in your credit report, and doesn’t consider anything else. Still, it might be helpful to know what your credit score is and what it means for you.

While there is no universal definition of an “excellent” credit score, virtually all lenders would consider your 846 FICO Score to be in that category. Here’s a rundown of what this credit score means to you, different types of lenders, and how to make sure your 846 credit score stays in the top tier for years to come.

A credit score of 846 is not just good it’s exceptional! In fact, an 846 credit score is about as close to perfect as you can get.

But what exactly makes a credit score of 846 so great? And how can you reach this credit score nirvana? I’ll explain everything in this article.

What is Considered a Good Credit Score?

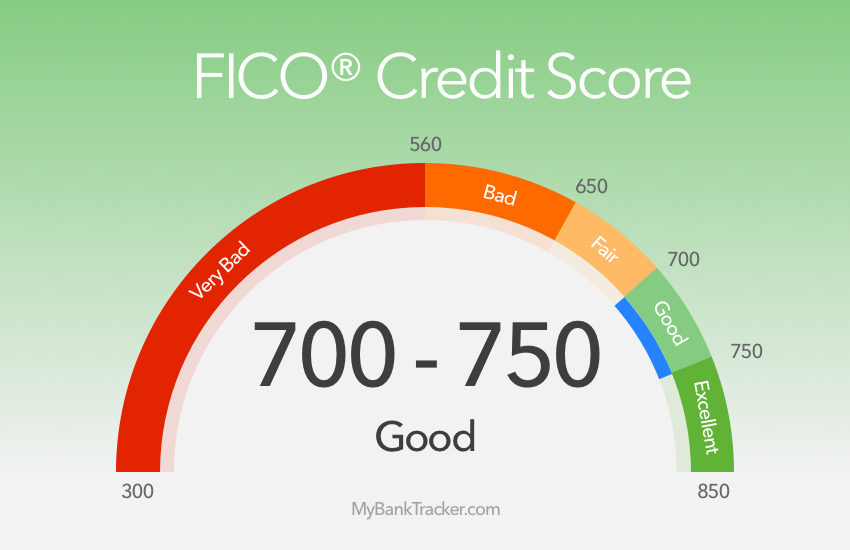

First let’s do a quick review of the credit score ranges so you understand where an 846 stands

- 300-579 = Bad Credit

- 580-669 = Fair Credit

- 670-739 = Good Credit

- 740-799 = Very Good Credit

- 800-850 = Exceptional Credit

As you can see, an 846 score is at the very top of the “Exceptional” range. It’s as good as it gets!.

According to FICO, the company that created the most widely used credit scoring model, only 14% of people have credit scores of 800 or above. So scoring an 846 puts you in very elite company credit-wise.

The Benefits of an 846 Credit Score

What does it mean to have such a high credit score? Here are some of the key benefits

1. Easy Approval for Credit

With an 846 credit score, you’ll have no trouble getting approved for just about any loan or credit card. Lenders will view you as being extremely low-risk, so you’ll get the best terms and lowest interest rates possible.

Whether you’re applying for a mortgage, auto loan, personal loan, or credit card, you can expect quick, no-hassle approval with an 846 score.

2. Large Credit Limits

In addition to easy approval, an exceptional 846 credit score qualifies you for the highest credit limits.

Credit card companies will be happy to give you a lot of spending power because your excellent credit score shows that you can handle big lines of credit responsibly.

3. Premium Credit Card Rewards

Many high-end credit cards for people with good credit come with lots of valuable rewards and sign-up bonuses.

If you get an 846, you can choose from high-end travel rewards cards, cash-back cards, and cards that give you statement credits or points that you can exchange for gift cards, merchandise, and more.

4. Lower Insurance Rates

Not only will your credit score save you money when borrowing, it can also lower your insurance premiums.

Car insurance companies often use credit-based insurance scores to set rates. Drivers with higher scores tend to pay less for coverage.

So your exceptional 846 credit score should qualify you for the lowest auto insurance rates.

How to Reach an 846 Credit Score

Now that you know how beneficial it is, you’re probably wondering how to raise your credit score to the lofty heights of 846. Here are some tips:

1. Always Pay Bills On Time

Payment history is the most important factor that determines your credit score.

If you want to reach a perfect 846, you need a flawless track record of paying all your bills on time, every time. Even one 30-day late payment can drop your score significantly.

Set up automatic payments and reminders to never miss a due date. Check your payment due dates often too.

2. Lower Credit Utilization

This measures how much of your available credit you’re using. Experts recommend keeping your overall utilization below 30%.

To hit an 846, get utilization as low as possible by paying balances down aggressively each month. Shoot for 10% or less if you can.

Also avoid maxing out any one credit card. Keep individual card balances well under the credit limit.

3. Let Your Credit History Age

15% of your credit score is determined by the length of your credit history. The longer your accounts have been open, the better.

Having credit cards open for many years demonstrates stability and responsible usage over time. Avoid closing old accounts unless absolutely necessary.

4. Limit Credit Applications

Every time you apply for new credit, the hard inquiry on your credit report could cause a slight dip in your scores. Too many in a short period looks risky.

To reach 846, be very selective about only applying for credit when absolutely needed. Too many applications could delay your goals.

5. Maintain Credit Mix

Lenders like to see you managing a mix of credit types – a mortgage, installment loans, credit cards, etc. This shows you can handle diverse accounts responsibly.

If your credit profile consists of only credit cards, consider adding an installment loan or mortgage to demonstrate you can make consistent monthly payments.

Is 850 a Realistic Goal?

With a near-perfect credit score of 846, is it even worth trying to inch up to the max of 850? The short answer is no.

Reaching 850 is unrealistic for most people. And more importantly, it won’t benefit you financially in any way compared to an 846 score.

Lenders don’t differentiate between someone with an 846 credit score and 850. You’ll get the same exceptional rates and treatment either way.

The only reason to try for 850 is personal satisfaction. It won’t save you any money or open additional credit opportunities.

Maintaining Your 846 Credit Score

Once you’ve achieved rarefied credit score air with an 846, you’ll want to monitor your credit closely to detect any dips early.

Obsessively checking your credit won’t directly impact your scores. But it allows you to quickly address any reporting errors or other problems that could affect your pristine credit profile.

Be vigilant about checking your credit reports and FICO scores from all three bureaus at least monthly, if not weekly. Also consider credit monitoring services that alert you to score changes.

A small slip in your credit habits could knock your 846 score down fast. So be sure to continually practice the excellent credit management required to sustain perfection!

Bottom Line

A credit score of 846 is about as close to perfect as you can get. This exceptional score will qualify you for the best loan terms, higher credit limits, premium rewards cards, and lower insurance rates.

While 850 is technically the max score, reaching 846 is realistically the best goal. It signals to lenders that you are an ideal borrower and allows you to leverage your credit for maximum savings.

What does an 846 credit score mean?

In short, an 846 credit score puts you in the top tier of U.S. consumers in the eyes of lenders. In the widely used FICO credit scoring model, scores range from 300 to 850. The average credit score was 714 in 2021. Fewer than one-fourth of U.S. adults have credit scores of 800 or higher.

To get your score to this level, you usually need to have been good with your credit for a long time. A credit score of 846 tells lenders that you are highly likely to pay back money that you borrow. According to a 2019 study by FICO, much less than 1% of borrowers with a FICO score of 800 or higher become seriously behind on their loan payments for things like credit cards or installment loans.

With all of that in mind, it’s important to keep in mind that your credit score is just one part of your overall financial well-being, and it is often not the only thing lenders look at when evaluating a loan application. When Upstart looks at personal loan applicants, our model looks at more than 1,000 data points, such as employment, education², and more.

Buying a car with an 846 credit score

You could get an auto loan even if you have bad credit. But just like with mortgages, having an excellent credit score like 846 should qualify you for the best rates a lender can offer, assuming your income and debt situation is acceptable. And with auto loans, your high credit score can make even more of a difference.

On a 60-month new car loan, the average borrower with a credit score of 720 or higher gets a 5.52% APR as of October 2022. With a score in the 660-689 range, the average rate is 9.14%. With a “fair” score of 600? You’re looking at an average rate of nearly 16%.

How I Boosted My Credit Score to 846: Practical Steps and Tips

FAQ

How rare is an 846 credit score?

Fewer than one-fourth of U. S. adults have credit scores of 800 or higher. In general, you need to have been good with your credit for a long time in order to get your score to this level. Lenders know that you will likely pay back any money you borrow if your credit score is 846.

Is a 900 credit score possible?

Does anyone have an 850 credit score?

What is a realistically good credit score?

For a score with a range of 300 to 850, a credit score of 670 to 739 is considered good. Credit scores of 740 and above are very good while 800 and higher are excellent. While credit scores range from 300 to 850, most people think that a score in the mid to high 600s or higher is good.