Your P45 shows how much tax you’ve paid on your salary so far in the tax year (6 April to 5 April).

You can check how much tax you paid last year if you think you might have paid too much.

What Happens to Your P45 When You Close the Office Door for Good

Yes, you absolutely do get a P45 when you retire! This important document isn’t just for people who are changing jobs or getting sacked – it’s for anyone leaving employment, including those riding off into the retirement sunset.

If you’re approaching retirement age and wondering about all the paperwork involved understanding what happens with your P45 is crucial for managing your finances properly after you stop working. Let’s dive into everything you need to know about P45s and retirement.

What Exactly is a P45?

Before we get into the specifics of retirement let’s clarify what a P45 actually is. A P45 is officially known as a “Certificate of Earnings and Pension Contributions” and serves as a vital document in the UK tax system. It details

- Your earnings for the current tax year (from April 6th to April 5th)

- The amount of tax you’ve paid so far in that tax year

- Your tax code

- Your National Insurance contributions

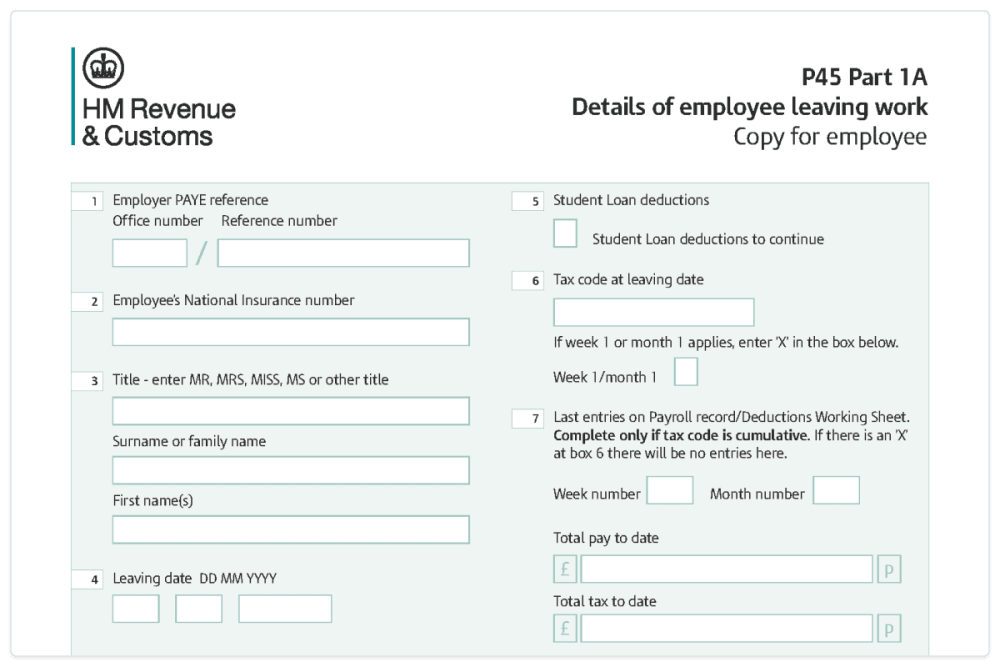

The P45 consists of four parts

- Part 1: Sent to HMRC by your employer

- Part 1A: For you to keep for your personal records

- Parts 2 and 3: To give to your new employer (or pension provider when retiring)

Retirement and Your P45: The Facts

When you retire, your employer is legally obligated to provide you with a P45, just as they would if you were leaving to take another job. This is true regardless of whether you’re:

- Taking full retirement

- Planning to work part-time elsewhere

- Considering returning to work later

As the RIFT Refunds website confirms: “Yes, you should still get a P45 from your last employer when you retire. You should hang onto it, too. Your pension provider will expect you to have it to hand, and you’ll need it to keep your tax code straight if you make any withdrawals from your pension.”

Why Your P45 Matters in Retirement

You might be wondering why you need a P45 if you’re not planning to work again. There are several important reasons:

1. For Your Pension Provider

When you start drawing your pension, your pension provider needs information about your tax situation. Your P45 helps them determine the correct tax code to apply to your pension payments, ensuring you’re taxed appropriately from day one.

Without a P45, your pension provider might have to use an emergency tax code, which could result in you paying too much tax initially (though you can reclaim this later).

2. If You Return to Work

Many retirees find themselves “un-retiring” these days. Rising costs of living might mean full retirement isn’t financially viable, or you might just miss the structure and social aspects of working.

If you do decide to return to work, having your P45 will make the process smoother. As explained on TheMoneyKnowHow website: “Some retirees may decide that full retirement is no longer affordable due to rising costs of living and choose to return to work in order to supplement their income.”

3. For Tax Investigations

HMRC can conduct tax investigations up to 20 years after a given tax year. Having your P45 safely stored gives you peace of mind that you can provide accurate information if ever required.

4. For Self-Assessment Tax Returns

If you need to complete a Self-Assessment tax return after retirement (perhaps because you have additional income sources), the information on your P45 will be useful.

What If You Don’t Receive Your P45?

By law, your employer must give you a P45 when you retire. However, if for some reason you don’t receive one:

- Contact your employer directly – Remind them of their legal obligation to provide your P45

- Contact HR department – If it’s a larger company, speak to the HR team

- Contact HMRC – As a last resort, HMRC can help chase this up

What If You Lose Your P45?

It happens to the best of us – important documents sometimes go missing. If you lose your P45:

- Contact your previous employer – They might be able to provide a copy if they use digital P45s

- Complete a Starter Checklist – If you’re starting another job or need to provide information to your pension provider, you can complete a Starter Checklist (formerly known as a P46)

- Contact HMRC – They can help ensure your tax affairs remain in order

Unfortunately, unlike some other documents, you can’t get an official replacement P45 from HMRC. As the RIFT Refunds site notes: “Remember, you can’t get a replacement P45 if you lose it.”

Tax Considerations When Retiring

When retiring, your tax situation becomes more complex. You might have multiple sources of income:

- State Pension

- Private/Occupational Pensions

- Investment Income

- Potential part-time work

Your P45 helps ensure that your initial tax code is correct, but it’s worth checking that HMRC has the right information about all your income sources.

If you return to work after retirement, the Money Know How website advises: “It will be crucial to confirm that your tax code is accurate from the start of your new job if you have additional sources of income, such as workplace/private pensions or state pensions.”

National Insurance After Retirement

An important consideration when retiring or returning to work after retirement age is National Insurance contributions.

Generally, once you reach State Pension age, you no longer pay National Insurance contributions, even if you continue working. However, you may need to provide proof of your age to your employer to ensure they don’t deduct NI from your wages.

How Long Should You Keep Your P45?

While a P45 is technically only valid for the tax year in which it was issued, it’s advisable to keep it for much longer. Some financial experts recommend keeping tax documents for at least 6 years, which aligns with how long HMRC generally has to investigate your tax affairs.

Given that tax investigations can sometimes go back 20 years in cases of suspected fraud, it’s not a bad idea to keep important tax documents like your P45 indefinitely if storage space allows.

What If You’re Already Receiving a Pension Before Fully Retiring?

If you’ve been drawing a pension while still working (which is increasingly common with pension freedoms and phased retirement), your situation is slightly more complex.

When you fully retire, you’ll still receive a P45 from your employer for your employment income. Your pension provider will continue to pay your pension as before, and they’ll have their own records of tax paid on that income.

Common Questions About P45s and Retirement

How long is a P45 valid for?

A P45 is valid throughout the tax year in which it was issued. If the tax year changes between you leaving a job and starting another activity that requires your tax information, you’ll need to use a Starter Checklist instead.

Do pension providers issue P45s?

No, pension providers don’t issue P45s. They issue other tax documents such as P60s at the end of each tax year showing how much pension you received and how much tax was deducted.

Can I use an old P45 from years ago?

No, you can only use a P45 from the current tax year. If you’re retiring years after your last employment, you won’t have a valid P45 to provide. In this case, you’ll need to complete a Starter Checklist for your pension provider.

Will my state pension be on my P45?

No, your state pension won’t appear on your P45. The P45 only covers income from the employer you’re leaving. State pension is administered separately by the Department for Work and Pensions (DWP).

Final Thoughts

Getting your P45 when you retire is not just a formality – it’s an important step in ensuring your tax affairs remain in order as you transition from employment to retirement.

Even if you think you’ll never need it again, make sure you receive your P45 and keep it somewhere safe. The transition to retirement brings enough challenges without adding tax complications to the mix!

Remember that your financial situation in retirement may be more complex than when you were employed, with multiple income sources potentially including pensions, investments, and perhaps some part-time work. Having all your documentation organized, including your P45, will help you manage this complexity with confidence.

If you do not have a P45

Your new employer will need to work out how much tax you should be paying on your salary if you do not have a P45. For example, if:

- you’re starting your first job

- you’re taking on a second job

- you cannot get your P45 from your previous employer

You’ll need to tell your new employer about things like other jobs you have, any benefits you get and if you have a student loan. They’ll ask you to either fill in a ‘starter checklist’ or give the information in another way.

Your employer will use this information to work out your correct tax code before your first payday if you do not have a P45.

Is this page useful?

Don’t include personal or financial information like your National Insurance number or credit card details. This field is for robots only. Please leave blank What were you doing? What went wrong?