Let’s face it – having extra money each month is a nice problem to have But deciding where to put those dollars can be tricky, especially when you’re torn between boosting your retirement savings and getting rid of your biggest debt I’ve been researching this question for years, and the answer isn’t as straightforward as you might think.

The Financial Dilemma We All Face

If you’re like most homeowners, your mortgage is probably your biggest monthly expense. That big number staring at you every month makes it tempting to throw extra cash at it whenever possible. On the other hand, retirement experts are constantly reminding us that we’re not saving enough for our golden years.

So what’s the right move? Should you accelerate your mortgage payments or pump up your 401(k) contributions? Let’s break down the pros and cons of each approach.

The Case for Investing in Your 401(k)

1. You’ll likely get a better return

When we crunch the numbers, investing in a 401(k) often comes out ahead mathematically. Here’s why:

- Most mortgages have relatively low interest rates (often between 3-6%)

- The stock market has historically returned around 7% annually over the long term

- Your contributions grow tax-deferred until retirement

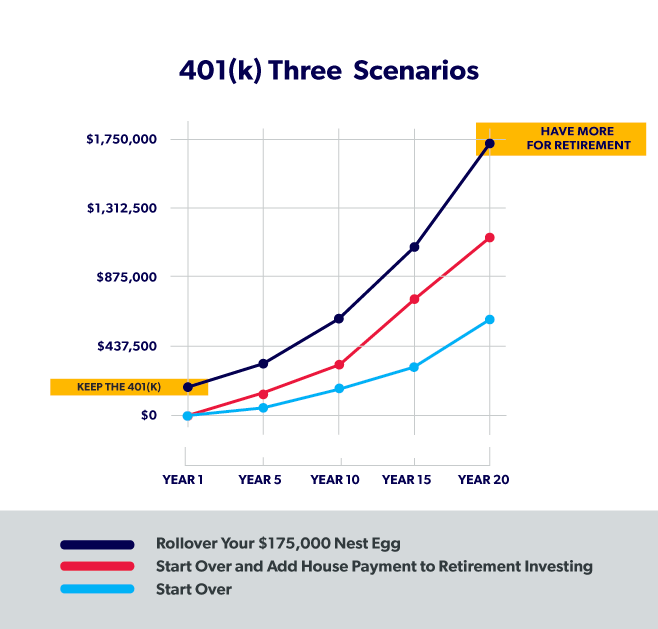

Let’s look at an example from MyBankTracker:

If you have a $200,000 30-year mortgage at 4% interest and pay an extra $200 monthly toward the principal, you’d:

- Save about $44,000 in interest

- Pay off your mortgage 8 years earlier

But if you invested that same $200 monthly in your 401(k) instead:

- Assuming a 7% annual return over 30 years

- Your nest egg would be worth approximately $235,000 more

- Even after subtracting the mortgage interest you paid, you’d still come out ahead by nearly $100,000!

2. You get tax advantages now and potentially later

Your 401(k) contributions:

- Reduce your current taxable income

- Grow tax-deferred until withdrawal

- May include employer matching (free money!)

As Rebecca Lake from MyBankTracker points out “You need the tax deduction.” When you pay off your mortgage early, you actually lose the mortgage interest tax deduction which can be valuable, especially for those in higher tax brackets.

3. You can’t take a loan for retirement

One of my favorite points from the Ameriprise article is simple but powerful: “While you can take a loan for a mortgage, you cannot take a loan out to fund your retirement.”

If you’re not maximizing your retirement accounts (especially if you’re eligible for catch-up contributions), it generally makes sense to prioritize retirement saving before accelerating mortgage payments.

When Paying Off Your Mortgage Makes Sense

Despite the mathematical advantage of investing, there are several scenarios where paying down your mortgage faster might be the right choice.

1. You’re approaching retirement

If retirement is on the horizon, a paid-off home means significantly reduced monthly expenses when your income might be lower. The peace of mind from having no mortgage payment can be invaluable during retirement.

2. You value peace of mind over potential returns

Some people simply sleep better at night knowing they’re debt-free. As the Ameriprise article notes, “Owning your own home outright can be liberating, and it’s hard to put a price on the security you may feel as a result.”

3. Your mortgage interest rate is high

If your mortgage rate is significantly higher than what you could reasonably expect from investments, the guaranteed “return” of paying off high-interest debt becomes more attractive.

4. You’re debt-averse

Some individuals just don’t like carrying debt, regardless of the potential financial benefits. If being debt-free is a personal financial priority, accelerating mortgage payments aligns with your values.

Finding a Middle Path

The good news is this isn’t necessarily an either/or decision. Many financial advisors recommend a balanced approach:

- First, ensure you’re getting any employer match – This is literally free money!

- Pay off high-interest debt – Credit cards and personal loans should generally be eliminated before extra mortgage payments

- Build adequate emergency savings – Have 3-6 months of expenses saved before accelerating either goal

- Consider a blended approach – Split your extra money between retirement contributions and additional mortgage payments

Practical Ways to Pay Off Your Mortgage Faster While Still Investing

If you want to do both, here are some strategies from Ameriprise that won’t derail your investing plans:

-

Make biweekly payments: By paying half your monthly payment every two weeks, you’ll make the equivalent of 13 payments annually instead of 12.

-

Add small, regular “overpayments”: Even an extra $100-200 per month can significantly reduce your loan term.

-

Use windfalls wisely: When you receive tax refunds, bonuses, or inheritances, consider applying a portion to your mortgage principal.

-

Refinance strategically: Switching to a shorter-term loan (like going from a 30-year to a 15-year mortgage) can help you pay off the loan faster, though your monthly payment will increase.

When Your Life Circumstances Matter

Your personal situation plays a huge role in this decision. According to the article from The Nest, consider these factors:

If you’re planning to move soon

If you don’t plan to stay in your current home long-term, putting extra money into the mortgage might not make sense. As MyBankTracker notes, “Paying off your mortgage early really doesn’t make financial sense if you’re not planning to stick with it in the long haul.”

If job security is a concern

In uncertain economic times, having a paid-off mortgage provides security. You can’t lose a house that’s fully paid for if you experience a period of unemployment.

If your time horizon is long

The longer your investment horizon, the more likely your 401(k) investments will outperform the interest savings from paying off your mortgage early.

My Personal Take

I’ve wrestled with this decision myself, and here’s what I’ve learned: there’s no one-size-fits-all answer. The mathematically optimal choice is usually to invest, especially if you’re young and have time on your side. But personal finance isn’t just about math—it’s about what helps you sleep at night.

For me, I’ve chosen a hybrid approach. I max out my employer match first (cause who doesn’t like free money?), then split any extra funds between additional 401(k) contributions and extra mortgage payments. This gives me both the potential growth from investing and the satisfaction of watching my mortgage balance decline faster than scheduled.

The Bottom Line

Before making your decision, consider:

- Your mortgage interest rate vs. potential investment returns

- Your tax situation and whether you itemize deductions

- Your risk tolerance and how you feel about debt

- Your retirement timeline and overall financial goals

- Whether you have adequate emergency savings and other debt

- Your job security and income stability

Remember that the “right” answer depends on your personal circumstances, financial goals, and emotional preferences. While the math might favor 401(k) investments, your peace of mind might favor mortgage repayment—and there’s real value in that too.

What’s your approach to this financial dilemma? Are you team 401(k), team mortgage payoff, or somewhere in between? I’d love to hear your thoughts in the comments!

Final Thoughts

Whatever you decide, make your choice deliberately after considering all factors. And don’t forget to reassess periodically as your circumstances and goals change. The most important thing is taking proactive steps toward financial security, whichever path you choose.

An Ameriprise financial advisor or other financial professional can help you evaluate your specific situation and determine the best approach based on your comprehensive financial picture.

Should I Pay Down My Mortgage Or Save For Retirement?

FAQ

Should you pay off your 401(k) if you have a mortgage?

With time on their side, younger workers also have the optimal ability to replenish the drawdown of retirement savings in a 401 (k) over the course of their working years. For older individuals or couples, paying off the mortgage can trade savings for lower expenses as retirement approaches or begins.

Is a 401(k) better than a mortgage?

There’s no universal rule to tell you whether your 401 (k) is a better bet than paying extra on the mortgage. The advantages of one option or the other vary with circumstance — for example, whether mortgage rates are up or whether your job is secure. When deciding which is the best choice for you, see how the pros

Should you invest in a 401(k) or a mortgage?

Investing in My 401 (k) There’s no universal rule to tell you whether your 401 (k) is a better bet than paying extra on the mortgage. The advantages of one option or the other vary with circumstance — for example, whether mortgage rates are up or whether your job is secure.

Do 401(k) plans pay more interest than mortgages?

From just a strictly mathematical perspective, you’re likely earning more in your 401 (k) plan than you are paying in interest on your mortgage. Even if you have a relatively conservative 401 (k) allocation, for example, you’re likely earning at least 5% on your money.

Should I use my 401(k) to pay off my house?

The main benefit to using your traditional 401 (k) to pay off your house is that you’ll no longer have to worry about making mortgage payments. If you’re like most American households, this will provide a significant boost to your monthly cash flow, possibly in the thousands of dollars.

Should you use retirement savings to pay off a mortgage?

Whether you’re decades away from stepping back from work or already in the thick of retirement, you might consider using savings, like retirement, to pay off your mortgage and be rid of the debt. But should you? And, what are the tradeoffs? Here’s some insight. Would you incur a penalty making a retirement withdrawal to pay off a mortgage?

Is it better to pay off your house or invest in 401k?

You should be maxing out your 401K before paying extra on your mortgage. Most good retirement funds will exceed 3%. Investments in a 401K are more liquid than real estate if you hit financial difficulties.

What does Suze Orman say about paying off your mortgage early?

Personal finance guru Suze Orman says it depends. While the possibility of job loss can trigger financial panic, Orman advises against rushing to drain your savings to pay off your mortgage early. Even if you have enough money saved to wipe out your mortgage, don’t pull the emergency cord until absolutely necessary.

How much will $10,000 in a 401k be worth in 20 years?

Why do people say not to pay off your mortgage?

The main reason NOT to payoff a mortgage is the cost of debt. Just like cholesterol, there’s good and bad debt. Mortgage debt is typically the least expensive debt avail. and (in the USA) there are tax incentives that further push down the cost (for most, not all homeowners).