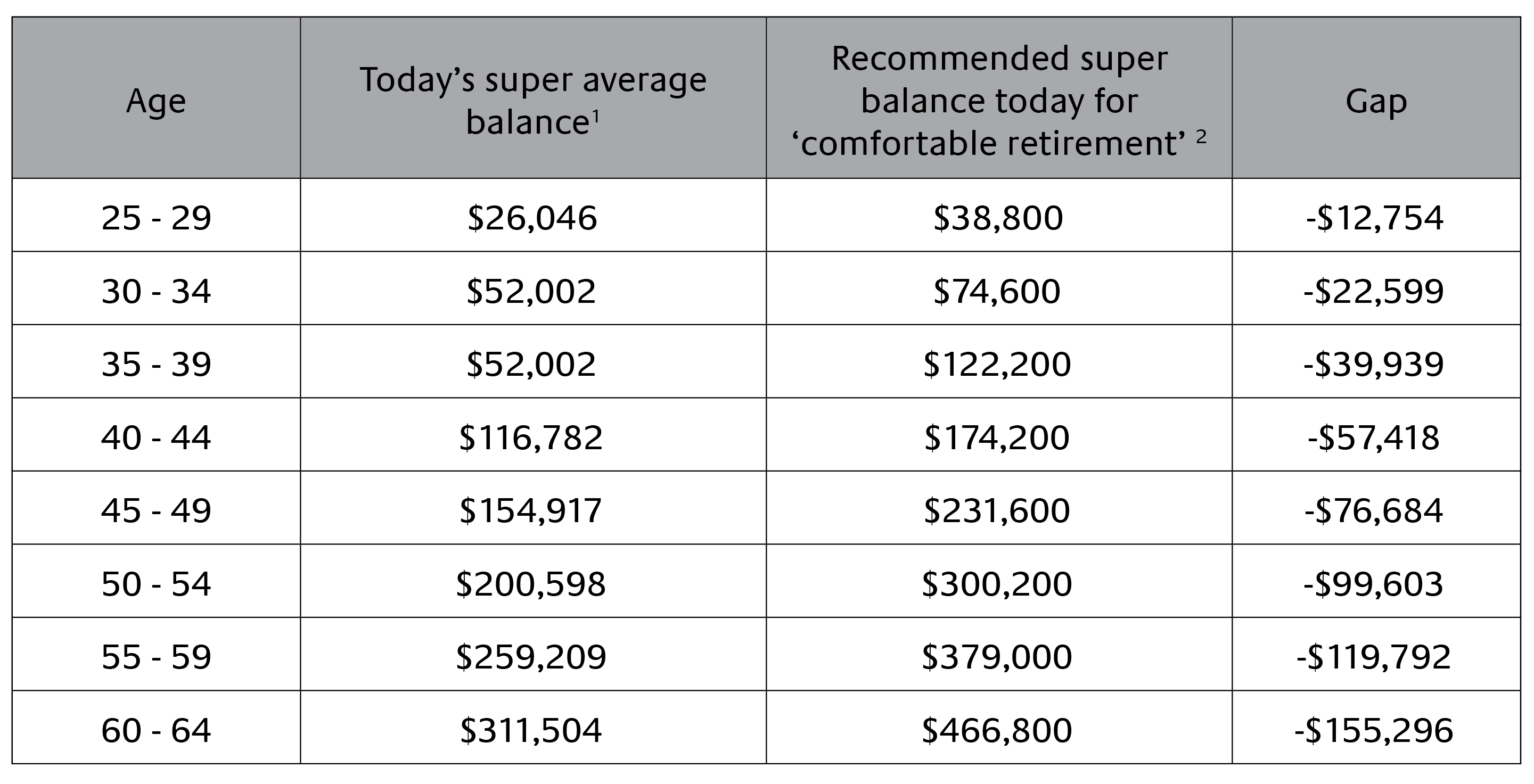

By the time you reach Age Pension age, you might have some money in the bank and hopefully a decent chunk in super savings to support you through retirement.

But you probably don’t want to be digging into your savings regularly. If eligible, the Age Pension could help you stretch your savings for longer after you stop working, while also giving you access to a range of concessions and benefits.

Worried your super balance might stop you from getting the Age Pension? You’d be surprised how much you can actually have stashed away and still receive Centrelink payments! As someone who’s been helping Aussies navigate their retirement planning for years, I want to share some straight facts about balancing your super with pension eligibility.

The Super-Pension Balance: What You Need to Know

Let’s cut to the chase – if you owned your home and were of pension qualifying age in 2020, a couple could have up to $394,500 in super and other assets and still receive the full Age Pension under the Centrelink assets test

But wait! The thresholds have changed since 2020, and it’s important to have the latest figures.

Current Age Pension Asset Test Limits (2025)

For those wondering how much super you can have without losing pension benefits today, here’s the current situation:

Full Age Pension – Assets Test Limits

| Status | Homeowner | Non-Homeowner |

|---|---|---|

| Single | $314,000 | $566,000 |

| A couple (combined) | $470,000 | $722,000 |

| A couple separated by illness | $470,000 | $722,000 |

| A couple, one partner eligible (combined) | $470,000 | $722,000 |

Part Age Pension – Assets Test Upper Limits

| Status | Homeowner | Non-Homeowner |

|---|---|---|

| Single | $686,250 | $938,250 |

| A couple (combined) | $1,031,000 | $1,283,000 |

| A couple separated by illness | $1,214,500 | $1,466,500 |

| A couple, one partner eligible (combined) | $1,031,000 | $1,283,000 |

These thresholds are significantly higher than they were in 2020! Good news for retirees.

How Super Affects Your Pension Eligibility

When Centrelink looks at your eligibility for the Age Pension, they test your situation in two ways:

- Assets Test – Looks at what you own (including super)

- Income Test – Looks at what money comes in (including deemed income from super)

The test that results in the lower pension amount is the one that applies to you Yep, that’s right – they use whichever method gives you less money! But don’t worry, I’ll explain how to work with this system

Does Super Count as an Asset for the Pension?

Simply put – yes, it does. Any superannuation you have will be counted as an asset, including the balance of any account-based pensions.

Here’s something many folks miss: your super is assessed the same way whether it’s in accumulation phase or pension phase. The assessment applies to both.

How Does Super Income Affect Your Pension?

The balance of your super is included in the Age Pension assets test. Additionally, deemed income from your super balance is included in your income test calculations even if you haven’t started drawing from it.

For the full Age Pension under the income test, your assessable income needs to be below:

- $212 per fortnight (single)

- $372 per fortnight (couple combined)

Real-Life Example: How Age Pension Assessment Works

Let me show you how this plays out with a practical example:

Bill (68) and Sharon (67) are both retired with these assets:

- Home (joint): $900,000 (exempt from assessment)

- Home contents (joint): $20,000

- Vehicles: $20,000

- Bank account (joint): $40,000

- Super – Account Based Pension (Bill): $300,000

- Super – Account Based Pension (Sharon): $400,000

- Australian Shares (Sharon): $15,000

Under the Assets Test, Bill and Sharon have $795,000 worth of assessable assets. This is below the homeowner couple upper-threshold for part-pension of $1,031,000, so they qualify for a part pension.

Their Age Pension payments will reduce by $1.50 each for every $1,000 their assets exceed the lower threshold of $470,000. This means their maximum Age Pension drops from $841.40 each per fortnight to $353.90 per fortnight.

Under the Income Test, they would get a higher pension amount of $783.15 each per fortnight. But since the Assets Test gives them a lower amount, that’s what applies.

Smart Strategies to Maximize Your Pension Eligibility

Here are some approaches you might consider to reduce your assessable assets:

-

Gift within limits – You can gift up to $10,000 in one financial year (maximum of $30,000 over 5 financial years)

-

Renovate your home – Since your principal home is exempt from the assets test, some homeowners choose to renovate

-

Repay debt secured against exempt assets – Paying off your mortgage can be a good strategy

-

Consider funeral bonds – Within limits, these are exempt from assessment

-

Look at your super withdrawal options – You can choose between lump sum withdrawals or income streams

Remember that taking money out of superannuation doesn’t affect payments from Centrelink directly, but what you do with that money afterward might.

Super Withdrawal Options in Retirement

When you meet the retirement condition of release, you can usually choose to withdraw your super as:

- A super lump sum

- A super income stream

- A combination of both

The withdrawal option you choose may affect the tax you pay and how much money you have for retirement.

A super income stream involves a series of regular payments from your super fund. These can be either:

- An account-based super income stream

- A capped defined benefit income stream

- An innovative retirement income stream

The Transfer Balance Cap: Something to Watch

There’s a lifetime limit on the amount you can transfer into tax-free retirement phase accounts. This is called your transfer balance cap.

From 1 July 2023, the general transfer balance cap is $1.9 million. This is significantly higher than the $1.6 million cap that was in place in 2020.

Understanding Your Age Pension Age

Before you can access the Age Pension, you need to have reached Age Pension age, which is currently 67.

Back in 2020, if you were born before 1 July 1955, the Age Pension age was 66. For those born between 1 July 1955 and 31 December 1956, it was 66 years and 6 months.

We’ve seen huge changes since 2020 in how much super you can have and still get the pension. The thresholds have increased significantly, giving retirees more flexibility.

The key takeaway? You can have substantial super savings and still receive some Age Pension. For example, a homeowner couple can have combined assets up to $1,031,000 and still receive a part pension in 2025.

Don’t assume your super balance automatically disqualifies you from the Age Pension. It’s worth checking your eligibility, as even a part pension can make a big difference to your retirement lifestyle.

FAQs About Super and the Age Pension

Can I get the Age Pension if my spouse still works?

Yes, you can apply for an Age Pension when you’ve reached age 67, even if your partner is younger or still working.

Does selling your house affect your pension?

Selling your house at market value doesn’t usually affect your pension eligibility, but giving it away for less than market value could impact your entitlement.

How much is the full pension for a single person?

To qualify for a full Age Pension as a single person, your income must be below $212 per fortnight, but you can still be eligible for a part Age Pension with higher income.

Do I have to declare super to Centrelink?

Yes, super pensions are usually treated as income and may reduce your Centrelink payments. Super lump sums may be included in the Assets Test.

Can I withdraw super after 60?

If you’re between 60 and 64, your super benefit is preserved until your “retirement.” After you’re retired, there are no restrictions to accessing your super benefit either as a pension or lump sum withdrawal.

Remember, retirement planning is not one-size-fits-all. Your personal circumstances, including your assets, income, age, and retirement goals, will determine the best approach for you. When in doubt, consider getting personalized financial advice to help maximize your retirement income.

Can you withdraw your super and still get the Age Pension?

When you withdraw money from your super, you’ll need to notify Centrelink. How the withdrawn funds are assessed will depend on what you do with the funds (e.g. spend or put them in the bank etc).

You should also consider any Centrelink implications of your partner’s withdrawals. For example, if your partner is under the Age Pension age and aren’t retired yet, Centrelink will not count their superannuation as part of your combined assets. However, if your partner withdraws some of their superannuation, it will be counted as part of your assets, so a withdrawal may impact your Age Pension.

Each person’s situation is different, so it’s important to understand all the ins and out and get trusted financial advice before making any decisions about your super and the Age Pension. A good place to start to get more detailed information is from the Services Australia website.

*These thresholds are reviewed and updated regularly. For the most up-to-date limits and tables, visit Services Australia.

WATCH: See how the government age pension and super work together through retirement

If you exceed the asset and income limit for the full Age Pension, you may be eligible for a part pension

From 1 July 2025, part pensions cease when your assets are over the cut-off point (also called the ‘asset limit’). As above, if you are a member of a couple, the limit is for both you and your partner’s assets combined. Here are Centrelink’s asset limits for the part pension*.

| Your situation | Asset Limit | |

| Homeowner | Non-homeowner | |

| Single | $704,500 | $962,500 |

| A couple, combined | $1,059,000 | $1,317,000 |

| A couple, separated due to illness, combined | $1,247,500 | $1,505,500 |

Note: As of 1 July 2025.

You can find the rates by checking the Payment and Service Finder via Centrelink.