Have you ever dreamed of paying zero taxes on your retirement withdrawals? Well that dream can become reality with Roth IRAs – but only if you know the rules. As someone who’s spent countless hours researching retirement options for my clients I’ve seen firsthand how understanding “qualified distributions” can save you thousands in retirement.

Today, we’re diving deep into what makes a Roth IRA distribution “qualified” and how these withdrawals are treated for tax purposes. The best part? Qualified Roth IRA distributions are completely tax-free! Let’s explore what this means for your retirement planning.

What Exactly Makes a Roth IRA Distribution “Qualified”?

For your Roth IRA distribution to be considered qualified (and thus completely tax-free) it needs to satisfy two key requirements

-

The Five-Year Rule The distribution must occur at least five years after you established and funded your first Roth IRA

-

One of These Conditions Must Be Met:

- You’re at least 59½ years old when taking the distribution

- You become disabled before taking the distribution

- The distribution goes to your beneficiary after your death

- You’re using up to $10,000 toward a first-home purchase (lifetime limit)

The five-year period starts on January 1st of the year for which you made your first Roth IRA contribution. For example, if you made a contribution for 2023 (even if you actually made the deposit in early 2024 before the tax filing deadline), your five-year period would begin on January 1, 2023.

I remember helping a client who thought each Roth IRA had its own separate five-year clock. She was wrong! All Roth IRAs owned by the same person count toward the same five-year period. So if you opened a Roth at Fidelity in 2019 and another at Vanguard in 2022, the five-year period for both started in 2019.

Tax Treatment of Qualified Roth IRA Distributions: 100% TAX-FREE!

Here’s the beautiful part that makes Roth IRAs so special – when your distribution is qualified, it’s completely tax-free. This means:

- No federal income tax

- No state income tax (in most states)

- No 10% early withdrawal penalty

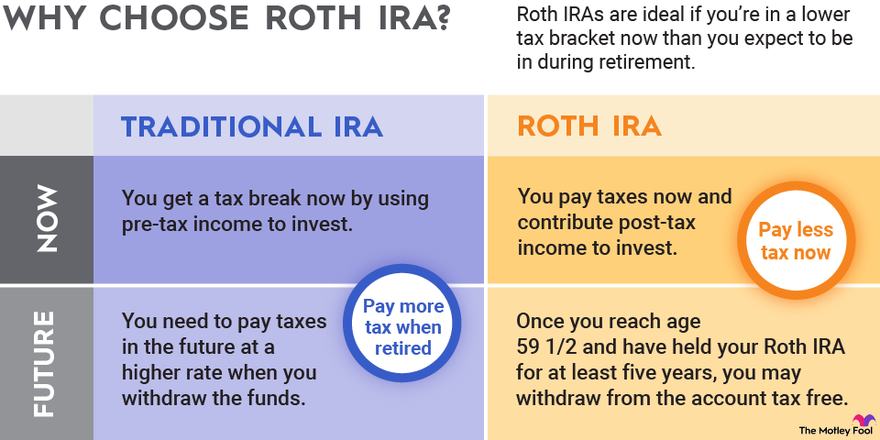

This is a HUGE advantage compared to Traditional IRAs, where distributions are generally treated as ordinary income and subject to income tax. With Traditional IRAs, you might also face a 10% early distribution penalty if you withdraw before age 59½.

Let me put this in perspective with a quick example. Say you’ve built up $500,000 in your Roth IRA by retirement age. If all distributions are qualified, you could potentially withdraw the entire amount (including all the earnings) without paying a single penny in taxes. That’s money the IRS can’t touch!

The Ordering Rules: How Non-Qualified Distributions Are Taxed

What happens if your distribution doesn’t meet the qualified criteria? Well, the IRS has specific “ordering rules” for Roth IRA distributions that determine which portions are taxable.

The IRS considers money to come out of your Roth IRA in this specific order:

- Regular contributions (always tax-free and penalty-free)

- Taxable conversion amounts (tax-free but may be subject to penalty)

- Nontaxable conversion amounts (tax-free and penalty-free)

- Earnings (taxable and potentially subject to penalty)

Let’s break this down with a simple table:

| Type of Roth IRA Asset | Qualified Distribution | Non-Qualified Distribution |

|---|---|---|

| Regular contributions | Tax-free & penalty-free | Tax-free & penalty-free |

| Taxable conversions | Tax-free & penalty-free | Tax-free but penalty may apply* |

| Nontaxable conversions | Tax-free & penalty-free | Tax-free & penalty-free |

| Earnings | Tax-free & penalty-free | Taxable & penalty may apply** |

*Penalty waived if 5 years since conversion or exception applies

**Penalty waived if exception applies

This ordering system actually works in your favor! Since contributions come out first, and these are always tax-free and penalty-free, you may be able to access some of your Roth IRA money even before meeting the qualified distribution requirements.

Real-Life Example: Understanding Roth IRA Distribution Taxation

Let’s say John is 55 years old and established his first Roth IRA in 2018. His Roth IRA now has:

- $10,000 in contributions

- $50,000 from taxable conversions (made in 2018)

- $10,000 from nontaxable conversions (made in 2018)

- $5,000 in earnings

If John takes out $25,000 in 2023, how would it be taxed?

The first $10,000 would be considered a return of his regular contributions – completely tax-free and penalty-free.

The next $15,000 would come from his taxable conversion amounts. Since these were already taxed when converted, there’s no income tax due. However, since it hasn’t been 5 years since the conversion AND John is under 59½, the $15,000 might be subject to the 10% early distribution penalty unless he qualifies for an exception.

This is why understanding these rules is so important! A little planning can save you a lot in taxes.

Exceptions to the 10% Early Distribution Penalty

The 10% penalty on early distributions can be waived if you qualify for one of these exceptions:

- You’re at least 59½

- You become disabled

- You’re a beneficiary withdrawing after the account owner’s death

- You use the money for unreimbursed medical expenses exceeding 7.5% of your AGI

- You’re taking substantially equal periodic payments (SEPP)

- You use the funds for higher education expenses

- You use the money for medical insurance after losing your job

- The distribution results from an IRS levy

- The distribution is a qualified reservist distribution

- The distribution is for qualified disaster recovery

- The withdrawal is rolled over within 60 days (if eligible)

- The withdrawal is for a qualified birth or adoption (up to $5,000)

I helped a client last year who needed to access her Roth IRA funds before age 59½. By documenting that she was using the money for qualified higher education expenses for her daughter, we were able to avoid the 10% penalty completely!

Important Updates: SECURE Act and SECURE 2.0 Changes

Retirement rules have changed significantly in recent years with the passage of new legislation:

-

SECURE Act (2019) made these key changes:

- Increased the Required Minimum Distribution (RMD) age from 70½ to 72

- Eliminated the “stretch IRA” provision for most beneficiaries

- Added a new exception allowing penalty-free withdrawals up to $5,000 for qualified births or adoptions

- Removed the age limit for traditional IRA contributions

-

SECURE 2.0 Act further raised the RMD age to 73

Remember, Roth IRAs don’t require RMDs during the owner’s lifetime, which is another major advantage over Traditional IRAs!

Frequently Asked Questions About Roth IRA Distributions

Can I deduct contributions to a Roth IRA on my taxes?

No, you absolutely cannot. Since Roth IRA contributions are made with after-tax money, there’s no tax deduction in the year you contribute. The tax benefit comes later when qualified distributions are tax-free.

Will converting my Traditional IRA to a Roth IRA save me taxes now?

Nope! When you convert, you’ll actually owe taxes on any pre-tax amounts you’re converting. The potential tax savings come later when your qualified Roth distributions are tax-free. I usually recommend conversions when you’re in a lower tax bracket or when market values are down.

Can a Roth IRA help avoid probate?

Yes! Like other retirement accounts, Roth IRA assets pass directly to your named beneficiaries without going through the probate process. This can save time, money, and hassle for your loved ones.

Do I need to report Roth IRA distributions on my tax return?

Even tho qualified distributions are tax-free, you’ll still receive a Form 1099-R showing your distribution. You should report this on your tax return, but it won’t increase your taxable income if it’s qualified.

Why I Love Roth IRAs for My Clients

As a financial advisor, I’ve seen firsthand how Roth IRAs can transform retirement planning. The tax-free growth and tax-free qualified distributions provide incredible flexibility and peace of mind.

One of my favorite strategies is to recommend clients contribute to both Traditional and Roth accounts, creating “tax diversification.” This gives you options in retirement to draw from taxable or tax-free accounts depending on your tax situation each year.

Key Takeaways on Qualified Roth IRA Distributions

To sum up what we’ve covered:

- Qualified Roth IRA distributions are 100% tax-free when you satisfy both the five-year rule and one of the qualifying conditions (age 59½, disability, death, or first home purchase)

- The ordering rules work in your favor by allowing contributions to come out first (always tax-free)

- The five-year rule applies once to all your Roth IRAs for qualified distribution purposes

- Each conversion has its own separate five-year period for determining if early withdrawal penalties apply

- Numerous exceptions can help you avoid the 10% early withdrawal penalty even on non-qualified distributions

Have you started your Roth IRA yet? If not, there’s no better time than now to begin building your tax-free retirement nest egg!

Remember, while I’ve tried to be accurate, tax laws change frequently. Always consult with a qualified tax professional before making significant retirement account decisions.

If I withdraw money from my IRA before I am age 59 1/2, which forms do I need to fill out?

Regardless of your age, you will need to file a Form 1040 and show the amount of the IRA withdrawal. Since you took the withdrawal before you reached age 59 1/2, unless you met one of the exceptions, you will need to pay an additional 10% tax on early distributions on your Form 1040. You may need to complete and attach a Form 5329, Additional Taxes on Qualified Plans (Including IRAs) and Other Tax-Favored Accounts PDF, to the tax return. Certain distributions from Roth IRAs are not taxable.

Can I deduct the 10% additional early withdrawal tax as a penalty on early withdrawal of savings?

No, the additional 10% tax on early distributions from qualified retirement plans does not qualify as a penalty for withdrawal of savings.