“Expert verified” means that our Financial Review Board thoroughly evaluated the article for accuracy and clarity. The Review Board comprises a panel of financial experts whose objective is to ensure that our content is always objective and balanced.

Bankrate is always editorially independent. While we adhere to strict , this post may contain references to products from our partners. Heres an explanation for . Our is to ensure everything we publish is objective, accurate and trustworthy. Bankrate logo.

Founded in 1976, Bankrate has a long track record of helping people make smart financial choices. We’ve maintained this reputation for over four decades by demystifying the financial decision-making process and giving people confidence in which actions to take next.

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. Our content is written by professionals with a lot of experience and is edited by experts in the field to make sure it is fair, correct, and reliable.

Our mortgage reporters and editors focus on the points consumers care about most — the latest rates, the best lenders, navigating the homebuying process, refinancing your mortgage and more — so you can feel confident when you make decisions as a homebuyer and a homeowner. Bankrate logo.

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. Our award-winning editors and reporters create honest and accurate content to help you make the right financial decisions.

We value your trust. We want to give readers information that is both correct and fair, and we have editorial standards in place to make sure that happens. Our editors and reporters thoroughly fact-check editorial content to ensure the information you’re reading is accurate. We maintain a firewall between our advertisers and our editorial team. Our editorial team does not receive direct compensation from our advertisers.

Bankrate’s editorial team writes on behalf of YOU – the reader. Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy. So, whether you’re reading an article or a review, you can trust that you’re getting credible and dependable information. Bankrate logo.

If someone wants to get a mortgage with a no income verification loan, also called a “doc loan,” they don’t have to show tax returns, pay stubs, W-2s, or other common forms of proof of income. Instead, the lender looks at the borrower’s assets, credit score, and debt-to-income ratio to decide if they can pay back the loan.

No income verification loans emerged in the early 2000s as an option for borrowers who did not have typical income sources, like the self-employed investors or retirees living off savings. However, lax lending standards and abuse led to the demise of these loans during the 2008 financial crisis.

While true “no doc” loans are rare today, variations like asset-based lending allow borrowers to qualify for a mortgage with alternative documentation. No income verification loans can be an excellent solution for certain borrowers but also come with stricter requirements.

How Do No Income Verification Loans Work?

With a traditional mortgage, the lender verifies the borrower’s income using documents like W-2s, pay stubs, and tax returns. This provides proof that the borrower has a stable income source to make regular mortgage payments.

No income verification loans operate differently:

-

The borrower gives an estimate of their income and assets—Instead of showing proof, the borrower gives an estimate of their income and assets.

-

Since income isn’t checked, the lender looks at assets, credit, and the ratio of debt to income to figure out if the borrower can pay back the loan.

-

Loan approval is based on the lender’s overall assessment – If the lender feels the borrower can repay the loan based on their profile, the no income verification loan is approved.

The main advantage of these loans is flexibility. Borrowers who may not have a salaried job can still qualify if they have strong finances otherwise. The main drawback is lenders perceive higher risk without income verification, so no doc loans come with stricter requirements.

Types of No Income Verification Loans

There are several variations of no income verification loans:

-

Stated Income – The borrower states their income without documentation. Lenders may require plausibility based on occupation.

-

Bank Statement – Lenders review 12-24 months of bank statements to assess cash flow. Common for self-employed borrowers.

-

Asset-Based – Loan approval is based on assets like savings and investment accounts. Used by retirees or high-net-worth borrowers.

-

No Income, Verified Assets (NIVA) – Only assets are verified, no income documentation provided.

-

No Income, No Assets (NINA) – Primarily for investors using projected rental income to qualify.

While programs differ, the unifying element is qualifying for a mortgage with little or no income documentation. Variations accommodate borrowers with diverse financial situations.

Who Qualifies for a No Income Verification Loan?

Since no income verification loans deviate from conventional mortgages, they serve niche demographics like:

-

Self-Employed – Irregular income makes documenting earnings difficult. This group can use assets or bank statements to get loans that don’t require proof of income.

-

Investors – Real estate investors can use projected rental income rather than W-2s to qualify. Useful for quickly expanding portfolios.

-

High-Net-Worth – Individuals with substantial assets may not have typical incomes. No income verification loans enable qualifying based on savings or investments.

-

Retirees – Retirees often have limited earned income. No income verification loans allow them to tap home equity using assets like pensions or retirement accounts.

The critical factor is having a strong overall financial profile despite untraditional income streams. No income verification loans provide solutions for unique situations.

Requirements for No Income Verification Loans

While no income verification loans offer more flexibility, lenders offset the additional risk by imposing stricter requirements:

-

Higher Credit Scores – Most lenders require minimum scores of 700. Anything lower may result in denial or less favorable loan terms.

-

Larger Down Payments – Down payments of 20-30% or higher are typical. This provides the lender equity cushion if the borrower defaults.

-

More Assets – Lenders often require liquid assets to cover several months or years of payments as reserves. This ensures the borrower can repay long-term.

Meeting the higher credit, down payment, and asset requirements demonstrates the financial means to take on a no doc loan responsibly despite the lack of income verification.

Pros and Cons of No Income Verification Loans

No income verification loans have advantages but also some potential drawbacks to consider:

Pros

- More flexible qualifying for niche groups

- Faster approval with less documentation

- Alternative options when income is difficult to prove

- Leverage assets instead of income

Cons

- Higher interest rates than conventional loans

- Larger down payments required

- Need excellent credit to qualify

- Loans may lack some consumer protections

No income verification loans serve a purpose but are not appropriate for all borrowers. Understanding the trade-offs helps determine if this route makes sense.

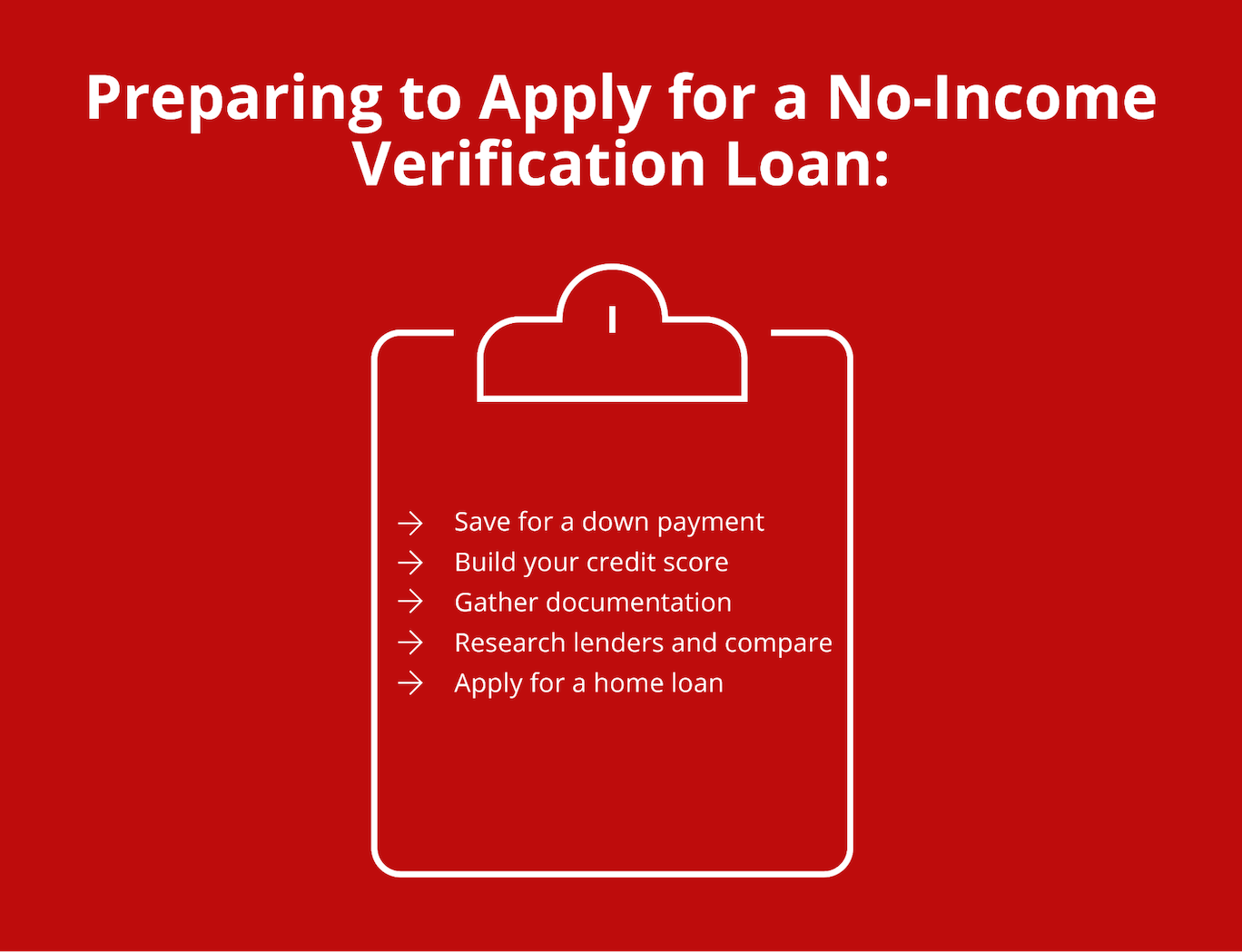

How to Qualify for a No Income Verification Loan

Qualifying for a no income verification loan entails:

- Having a credit score of 700+

- Providing bank statements showing ample assets

- Making a large down payment, often 20-30%

- Maintaining low debt-to-income ratios without income documentation

- Finding a lender specializing in alternative product offerings

Meeting strict criteria demonstrates you can manage the loan responsibly despite less income verification. A qualified mortgage broker is invaluable for navigating this specialized process.

Are No Income Verification Loans Still Available?

The “no doc” loans that contributed to the housing bubble are extinct today. However, variations allowing alternative documentation persist in limited contexts. Common options include:

- Bank statement lending for self-employed borrowers

- Asset-based loans using savings and investments

- Niche lender products for high-net-worth individuals

- Investor loans using projected commercial rental income

These programs deviate from conventional loans but can assist borrowers with unique situations. The critical factor is maintaining prudent lending standards absent income documentation. No income verification loans still fill important niches when done responsibly.

The Bottom Line

No income verification loans enable qualifying for a mortgage based on assets, credit, or other alternative documentation instead of pay stubs or tax returns. While not appropriate for everyone, these specialty loans serve self-employed, investors, and high-net-worth individuals with non-traditional finances. However, borrowers must meet strict criteria and accept higher rates and costs. When utilized prudently, no income verification loans remain viable for a subset of borrowers.

Should you get a no-doc mortgage?

No-doc mortgages can be a good option for certain homebuyers if you fall into one of these categories:

- You’re self-employed.

- You have an inconsistent income, but ample assets.

- You have hefty tax write-offs that lower your taxable income.

- You’ve generated a high net worth through a non-traditional source, like an inheritance.

Because of the costs involved with a no-doc mortgage, you should only explore this option if you can’t qualify for a traditional mortgage. Many lenders will work with self-employed borrowers to verify their income in alternative ways, without the need for a no-income verification mortgage.

Pros and cons of no-doc mortgages

Like just about any type of loan, a no-doc home loan comes with benefits and drawbacks.

No Income Verification Personal Loans: What You Need to Know

FAQ

Can you get a mortgage with no income verification?

If it’s due to issues with your tax return or the inability to prove your income using traditional methods, a no-income verification mortgage may be ideal. Here’s what you need to know before applying. Can You Get a Home Loan with No Income Verification?.

What are the benefits of no income verification mortgages?

Below are some key benefits of no income verification mortgages: You won’t have to provide income documentation. Your debt-to-income ratio may not stop you from being approved for a loan. You could be eligible for a loan even if you took several write-offs in recent years.

What are the different types of no income verification loans?

Borrowing solutions include secured loans, loans with low minimum income requirements and no-doc personal loans. No-income verification loans don’t require proof of income to qualify for a loan. Online secured personal loans, pawn shop loans, title loans and credit card cash advances are the primary types of no income verification loans.

Do no-income verification mortgages require proof of income?

No-income verification mortgages don’t require proof of income. But these types of loans require proof of other assets. You always need to prove to a lender that you can afford to repay the loan. What is a no-income verification mortgage?.

What is a no-income verification mortgage?

No-income verification mortgages, also known as stated income or low-documentation mortgages, are popular types of non-qualified (Non-QM) home loans. These types of home loans allow you to qualify your income based on alternative methods. A few key advantages of mortgages with no-income verification offered by Griffin Funding include:

What is a no-income verification personal loan?

A no-income verification personal loan is a type of loan where the lender doesn’t require proof of income to qualify for loan approval. More specifically, they don’t require traditional documentation such as pay stubs, W-2s or tax returns like most personal loan lenders.

Can you get a loan without verifying income?

Most of the time, it’s hard to get a loan without proof of income because lenders want to know that you can pay back the loan. However, some lenders may consider other stuff like credit history and scores, assets, or a co-signer who has a steady income.

What credit score is needed for no-income verification?

To be eligible, most borrowers need a credit score of 700 or higher (higher than conventional loans), a down payment of 30% or more (higher than conventional loans’ 5% down payment), and significant assets like bank balances, investment accounts, or rental income.

How much do you have to put down for a no-income verification mortgage?

You do not need tax returns or tax transcripts to qualify. Lenders can use 12 or 24-month bank statements. Businesses can show 12-24 months of P&L statements. You can get a no-income verification mortgage with as little as 10% down.

Does LendingTree require proof of income?

Yes, LendingTree generally requires proof of income. When applying for loans through LendingTree, you’ll need to provide documentation like pay stubs, W-2s, or tax returns to verify your income, as well as information about your employment and debts.