If you have good credit, you may be able to get a better interest rate on a new loan, credit card, or mortgage. The interest you pay on your loan over its life will be hundreds to thousands of dollars less if you do this. To improve your current and future standing, you need to know how your credit score affects other parts of your finances. It can help you get ready for what your score range means and how it will affect your life to check your credit report, keep an eye on your credit scores, and keep track of your credit history.

In Canada, credit scores range from 300 to 900. The lowest credit score in Canada is in the 300 range while the highest tends to be in the 800 range. Here’s how to know where you fall and how to boost your credit score and use your fluctuating credit scores to improve your credit history and increase credit limit and reports.

Your credit score is a three-digit number that tells lenders about how creditworthy you are and how well you can pay back debt. In Canada, credit scores range from 300 to 900. A higher score means you are less of a credit risk. But what exactly constitutes a bad credit score in Canada?.

What is Considered a Bad Credit Score in Canada?

Credit scores below 560 are usually seen as bad or poor in Canada. According to Equifax, one of Canada’s two main credit bureaus, a credit score below 560 means that lenders are likely to be wary of lending money to you.

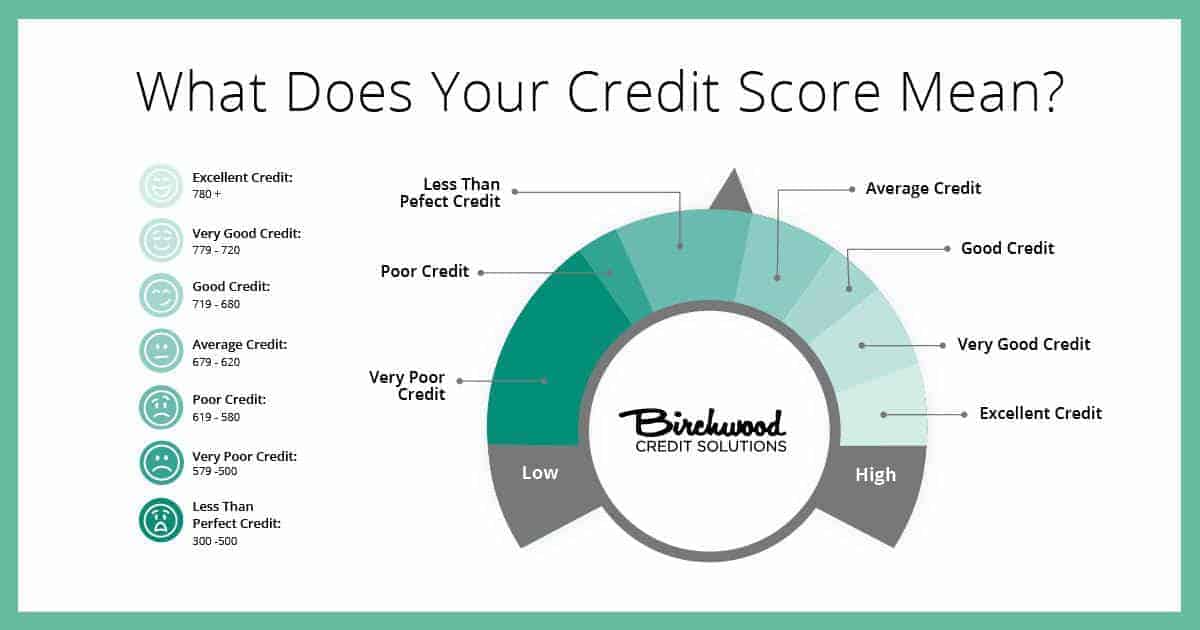

While there is some variation between credit scoring models here is how the score ranges generally break down

- 800-900: Exceptional

- 760-799: Very Good

- 680-759: Good

- 620-679: Fair

- 560-619: Poor

- 300-559: Bad

So, if your credit score is 559 or less, that’s considered bad credit, and it will be hard for you to get loans, mortgages, and credit cards.

How Credit Scores Are Calculated in Canada

The two main credit bureaus, Equifax and TransUnion, use different proprietary formulas to calculate your credit score. While the exact algorithms are secret, we know they take into account

- Payment history (35%): Whether you pay your bills on time. The biggest factor.

- Credit utilization (30%): How much you owe compared to your total credit limits. Keep this below 30%.

- Credit history length (15%): How long you’ve been using credit. Longer is better.

- Credit inquiries (10%): Applying for a lot of credit in a short timeframe can lower your score.

- Credit mix (10%): Having different types of credit (credit cards, loans, etc).

Your personal credit report data from lenders is fed into these algorithms to generate your score. Even a small difference in any factor can cause big swings in your overall score.

What Does a Bad Credit Score Mean for You?

A poor credit score below 560 will make getting approved for credit much more difficult and expensive:

- You’ll likely get rejected for credit cards, loans, and mortgages.

- If approved, you’ll pay much higher interest rates and fees.

- You may need to provide collateral/security deposits.

- Other areas life like renting an apartment can also be impacted.

A bad credit score suggests you are a high-risk borrower based on your past repayment behavior. While it doesn’t inherently mean you are irresponsible, it does limit your financing options.

Credit scores aren’t set in stone, which is good news. You can work to raise your score over time. Let’s look at how.

How to Improve Your Credit Score in Canada

If you have bad credit, don’t panic. Here are some tips to start rebuilding and improving your credit score:

1. Use a Secured Credit Card

Secured credit cards require a security deposit that acts as your credit limit. The card issuer reports your payment activity to the credit bureaus each month, helping build your credit profile. The deposit is fully refundable when you close the account.

The Refresh Secured Card from Desjardins is a good secured card option with no monthly fees.

2. Pay All Bills on Time

Payment history makes up 35% of your credit score calculation. Get into the habit of paying at least the minimum monthly payment on all bills before the due date. Setting up autopay can help.

3. Lower Your Credit Utilization Ratio

Don’t max out your credit cards. Experts recommend keeping your balance below 30% of the credit limit on each card. The lower the better for your score.

4. Don’t Close Old Credit Card Accounts

While open credit cards count against your credit utilization, closing the accounts also shortens your credit history which can lower your score. Leave old accounts open.

5. Limit New Credit Applications

Each application triggers a hard credit check that can temporarily knock a few points off your score. Only apply for credit you need and space applications out over time.

6. Correct Errors on Your Credit Report

Errors like missed payments or unknown accounts could be dragging down your score. Review your credit reports regularly and dispute inaccuracies.

7. Build Credit Mix Over Time

Having different types of credit—credit cards, a car loan, etc.—shows you can handle various credit lines responsibly. Don’t open accounts just for mix, but build it over time.

Be Patient When Rebuilding Your Credit

Improving your credit takes time and discipline. Pay all bills on time, keep balances low, limit inquiries, and build credit history over years not months. Monitor your score monthly and celebrate milestones along the way.

With diligence and smart credit habits, you can rebuild even the worst credit into something respectable over time. Don’t get discouraged—a poor score today doesn’t have to mean a poor score forever.

How to improve your score to get above the lowest credit scores in Canada

It is not the end of the world though if you have a bad credit score. you can still take steps to improve your credit reports and boost bad credit to a better range. It will take time but it can be done. Here’s how you can boost your bad credit rating and poor credit history by using a credit card responsibly:

- Pay your credit card bill on-time. Always pay your credit card bill on time and in full each month. On-time payments account for 35% of your credit score, so staying on top of this will help your score improve. Enrolling in autopay can help you keep your account in good standing. This will go a long way in improving your payment history.

- Pay more than the minimum due. If possible, pay off your entire balance, but if you can’t, try to pay more than the minimum amount due to help keep your account in good standing and to decrease interest charges. Positive payments are good for your credit reports and will help improve your bad credit standing over time.

- Don’t overspend. Only charge purchases you can afford to pay back in full. Not only will this prevent you from accumulating credit card debt and interest, but it will help your credit score grow by keeping your balance low. Show you are responsible with your payment history and manage your money well to price to a lender, bank or credit union you are low risk when it comes to paying back a loan.

- Charge less than 30% of your credit limit. Your credit utilization — how much you use in credit versus how much is available to you — accounts for 30% of your credit score. Try to limit credit card purchases to 30% or less than your total credit limit. One of the biggest mistakes people make that lead to bad credit ratings is they fail to manage their debt and have a high income-to-debt ratio.

- Treat your credit card like a debit card. To avoid missing a payment, pay off purchases as you charge them. Many bad credit scores come from allowing cards to get maxed out and high interest rates to boost balances beyond what can easily be paid off. You can avoid this problem from the start with smart use of your credit card accounts.

Credit score range

Score type

Below 560- Poor or bad credit scores

560 to 659- Fair credit scores

660 to 724- Good credit scores

725 to 759- Very good credit scores

760 and up- Excellent credit scores

A score below 560 is generally considered to be a bad credit score in Canada, according to credit bureau Equifax. A score between 560 and 659 is often considered fair, while scores between 660 and 724 are considered to be an acceptable or good credit score. If your score is between 725 and 759 on your credit report, it’s considered very good, while scores 760 and higher are viewed as excellent. If your score is at 560, lower, or hovering close to this range, your credit score is considered poor and it is generally seen as a bad credit score.

How to increase your CREDIT SCORE to 800 (Avoid these 5 mistakes!)

FAQ

What is a bad credit score in Canada?

If you do not know what your credit score is, check it for free here. What is a Bad Credit Score? A credit score below 560 is generally considered a bad credit score in Canada. This means that if your score ranges between 300 and 559, you will find it challenging to qualify for a loan or credit card.

What is a bad credit score range?

A bad credit score range is usually between 300 – 559. However, as mentioned above, this range may vary by lender and credit scoring model used. Having bad credit scores can make borrowing less accessible and more expensive. It can also affect your insurance premiums and ability to qualify for a job or rental unit.

What does a bad credit score mean?

Depending on where your credit score falls within this range, you can have a bad to excellent credit. That said, there is no definitive model for what certain credit scores mean to all lenders and creditors. One lender may consider credit scores of 760 and above to be excellent, while another may consider scores above 780 to be excellent.

Does checking your credit score hurt your credit?

Checking your score won’t hurt your credit — promise. Canada’s credit scores range from 300 to 900. A score below 300 means you have bad credit. A bad credit score is a score of 574 or less and means banks, lenders, landlords, and even some employers will consider you less financially responsible than borrowers with a higher score.

Is 700 a good credit score in Canada?

A credit score of 700 is considered good (scores between 660 and 724). In fact, with a credit score of 700, you’re only 25 points away from the very good credit score range. Find out more about your 700 credit score: Is an 800 credit score a good credit score in Canada? Credit scores between 760 and 900 are great.

Is 650 a bad credit score in Canada?

Most people in Canada, though, have a credit score that sits around 650. This is for all areas of Canada, not just Ontario or BC, and while that isn’t a bad score at all, there’s still plenty of room to grow. It’s a complex topic and before we dive into the details, we need to start from the beginning. What Are Credit Scores?.

What credit score is considered bad in Canada?

Equifax, the credit bureau, says that a score below 560 is usually seen as bad credit in Canada. Scores between 560 and 659 are usually thought to be fair, and scores between 660 and 724 are thought to be good or acceptable.

Is a 600 a bad credit score?

A credit score of 600 or below is generally considered to be a bad credit score. And if your credit is low, you may qualify for a loan but the terms and rates may not be favorable. Credit scores between 601 and 669 are considered fair credit scores.Feb 21, 2025

How common is a 750 credit score?

Is a 900 credit score possible?