If you quit your job and you have accumulated a substantial 401(k) balance, you may be worried about losing your 401(k) money. Find out when your employer can take your 401(k).3 min read

If you quit your job and you have a substantial amount saved in your 401(k), you may be wondering what will happen to your 401(k) money. Generally, a 401(k) is tied to your employer, and once you leave, you wont be able to contribute to the account. While the 401(k) money legally belongs to you, there are circumstances when the employer may take part or all of your 401(k).

Your employer may take your 401(k) money if you quit your job before the money is fully vested. If your employer has a vesting schedule, and you quit your job before you have satisfied the vesting schedule, your employer may take the unvested portion of the 401(k) match. Also, if you have defaulted on a 401(k) loan, your employer may offset the unpaid loan against your 401(k) balance. Plan loan offset occurs when there is a permissible distribution event like termination of employment.

Have you ever wondered what happens to your employer’s 401(k) matching contributions if you leave your job? You’re not alone. Many employees are surprised to learn that their employer can legally take back some or all of their matching contributions under certain circumstances.

As someone who’s helped countless clients navigate their retirement planning, I’ve seen the confusion and sometimes panic when people realize they might lose some of their retirement savings. Let’s clear up this misunderstood area of retirement benefits.

The Short Answer: Yes, But It Depends on Vesting

Yes, your employer can legally take back their matching 401(k) contributions if you leave before being fully vested However, they cannot touch your personal contributions or any gains on those contributions.

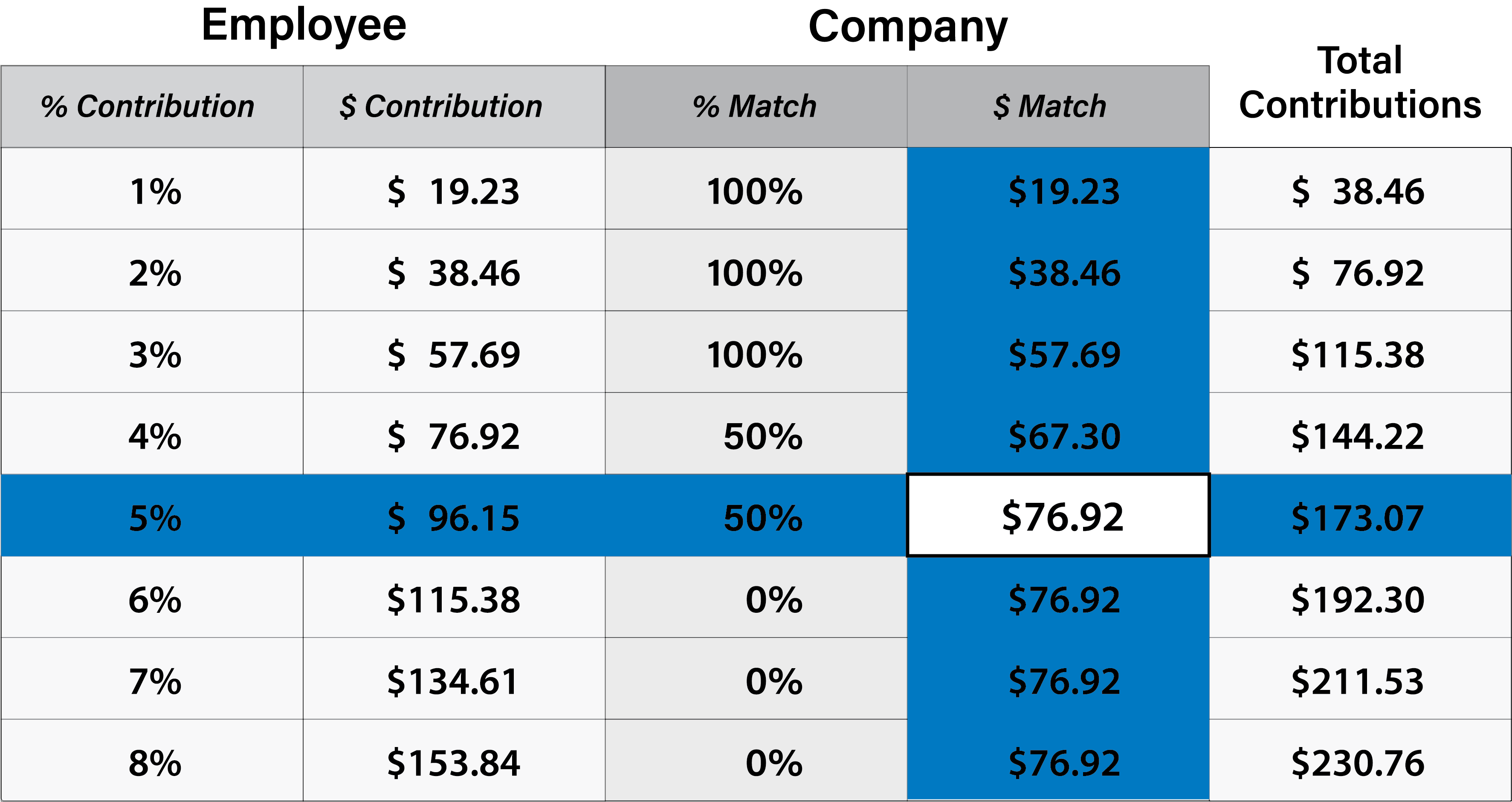

Understanding 401(k) Contribution Types

Before diving deeper we need to understand the different types of contributions that go into your 401(k)

-

Employee elective deferrals – These are contributions you make from your own paycheck. These are always 100% yours from day one.

-

Employer contributions – These can be:

- Matching contributions (when employers match a percentage of what you contribute)

- Profit-sharing contributions (discretionary amounts employers may add)

While your personal contributions are always non-forfeitable employer contributions often come with strings attached.

The Concept of Vesting: Why Employers Can Take Back Their Match

Vesting is basically the process through which you gain full ownership of your employer’s contributions over time. It’s a retention tool that companies use to encourage employees to stay longer.

There are two primary types of vesting schedules:

Cliff Vesting

With cliff vesting, you own nothing of your employer’s contributions until a specific date, when you suddenly own 100%. A typical cliff vesting period is 3 years.

For example, if your company has a 3-year cliff vesting schedule:

- Year 1: 0% vested

- Year 2: 0% vested

- Year 3: 100% vested

If you leave before completing 3 years, you forfeit ALL employer contributions.

Graded Vesting

With graded vesting, you gradually gain ownership of employer contributions over time.

A common graded schedule might look like this:

- After 2 years: 20% vested

- After 3 years: 40% vested

- After 4 years: 60% vested

- After 5 years: 80% vested

- After 6 years: 100% vested

If you leave after 4 years with this schedule, you’d keep 60% of the employer contributions and forfeit the remaining 40%.

The IRS does set maximum limits on these schedules:

- Cliff vesting cannot exceed 3 years

- Graded vesting cannot exceed 6 years

Who Gets to Keep the Gains?

This is where things get a bit tricky. If you leave before being fully vested, the employer keeps the gains on the unvested portion of their matching contributions.

For example, let’s say your employer contributed $10,000 in matching funds, which grew to $12,000 through investment gains. If you’re only 60% vested when you leave:

- You keep $6,000 of the original contribution plus 60% of the gains ($1,200)

- The employer takes back $4,000 of their original contribution plus 40% of the gains ($800)

Is This Really Legal?

Many people ask me, “Is it really legal for my employer to take back their 401(k) match?” The answer is yes. The U.S. Department of Labor and IRS regulations explicitly allow for vesting schedules and the forfeiture of unvested employer contributions.

These rules are part of the Employee Retirement Income Security Act (ERISA) which governs retirement plans. As long as your employer follows the vesting rules and clearly communicates them to you, they’re acting within their legal rights.

Scenarios When Employers Might Retrieve Contributions

Besides the standard vesting rules, there are a few other circumstances when employers might take back 401(k) contributions:

1. Administrative Errors

If an employer accidentally contributed more than allowed by the plan terms or IRS limits, they can retrieve the excess amount. This might happen if:

- Contributions were made for an ineligible employee

- The employer contributed more than the plan allows

- The contribution exceeded IRS limits

These are considered “inadvertent benefit overpayments” and require corrective action.

2. Failed Non-Discrimination Testing

401(k) plans must undergo annual testing to ensure they don’t disproportionately benefit highly compensated employees. If a plan fails these tests, adjustments to employer contributions might be necessary, potentially resulting in funds being returned.

3. 401(k) Loan Defaults

If you’ve taken a loan from your 401(k) and default on it (perhaps by leaving your job), your employer may deduct the outstanding loan amount from your 401(k) balance.

Real-World Example

I recently worked with a client, Jamie, who left her job after 2.5 years. Her company had a 5-year graded vesting schedule (20% per year). Her employer had contributed $15,000 in matching funds, which had grown to $18,000.

Since Jamie was 40% vested (20% after year 1, plus 20% after year 2), she kept:

- $6,000 of the original employer contribution (40% of $15,000)

- $1,200 of the earnings on those contributions (40% of $3,000 in earnings)

Her employer took back the remaining $10,800. Jamie was disappointed but understood that these were the terms of the plan.

What You Can Do to Protect Your 401(k) Match

-

Understand your vesting schedule – Read your plan documents carefully to know exactly when you’ll be fully vested.

-

Time your departure strategically – If possible, consider delaying your departure until after a vesting milestone.

-

Negotiate vesting during hiring – When starting a new job, you might be able to negotiate a more favorable vesting schedule, especially if you’re a highly sought-after employee.

-

Consider the match when evaluating job offers – A job with a more generous match but longer vesting period might not be better than one with a smaller match but immediate vesting.

What Happens to Forfeited Funds?

When employees forfeit unvested matching contributions, that money typically:

- Remains in the plan

- May be used to reduce future employer contributions

- Could be used to pay plan expenses

- Might be reallocated among remaining plan participants

The specific handling of forfeited funds should be outlined in your plan documents.

Additional 401(k) Considerations

Negotiating Vesting

If you’re considering leaving before being fully vested, you might try to negotiate with your employer to accelerate your vesting schedule, especially if you’re moving to a position with better overall benefits.

Rolling Over Vested Funds

When you leave a job, you can roll over your vested 401(k) funds (including any vested employer contributions) to an IRA or another employer’s 401(k) plan without tax penalties.

While it might seem unfair that employers can take back their matching contributions, remember that this is a benefit they provide with specific terms. The key is to understand those terms and incorporate them into your career and retirement planning.

Your personal contributions are always yours, and once you’re fully vested, employer contributions are yours too. Until then, consider the vesting schedule as an additional factor when making career decisions.

I’ve seen many clients benefit from staying just a few months longer at a job to reach a vesting milestone. Sometimes, that patience can mean thousands of additional dollars in your retirement account!

Have you had any experiences with losing unvested 401(k) matching contributions? What strategies have you used to maximize your retirement benefits? I’d love to hear your thoughts in the comments!

FAQs About Employer 401(k) Match Forfeiture

Can an employer take back their 401(k) contribution?

Yes, employers can take back unvested matching contributions if you leave the company before completing the vesting period. However, they cannot take back your personal contributions or any fully vested employer contributions.

Can an employer reverse a 401(k) contribution?

Once contributions are made into a 401(k) plan, they can rarely be withdrawn, even when a payroll reversal happens. Instead, if a payroll is reversed, the funds typically go into “plan cash,” an unallocated account within the plan.

Can my employer take away my 401(k) match during employment?

Employers may limit or stop matching contributions during difficult financial times. These cuts are usually temporary. If this happens, consider increasing your personal contributions or contributing to an IRA to maintain your retirement savings rate.

Does your employer match your 401(k) contributions?

According to the Plan Sponsor Council of America, about 98% of companies that offer a 401(k) match their employees’ contributions to some extent. However, the matching formula varies significantly between companies.

Can your employer take your 401(k) if you default on your 401(k)?

If your 401(k) loan is due and you default in making timely loan payments, the 401(k) loan will be considered to be in default. A 401(k) plan may provide that, if the 401(k) is not repaid on time, the account balance may be offset when there is a permissible distribution event such as termination of employment.

A plan loan offset is the unpaid loan balance that reduces your 401(k) balance. Usually, a 401(k) plan may provide that if a 401(k) loan is in default, the unpaid loan balance should be deducted from your 401(k) balance. The plan loan offset is considered an actual distribution, and it may be eligible for rollover to a qualified retirement plan. It can be triggered by distribution events like plan termination, death, or voluntary leaving employment.

What to do with your 401(k) if you quit

Once you quit your job, you wonât be allowed to make further contributions to the account. However, the 401(k) money is still yours, and you must figure out what to do with the money. Here are some options with the money: