If youve heard about Experian Boost®ø page and are wondering whether it really works, the answer is yes! Since launching in early 2019, Experian Boost has helped millions of people instantly increase their credit scores.

Experian Boost is the first service that lets you use your monthly phone, internet, rent, insurance, and streaming service bills to build credit history and raise your credit score. Connecting to your bank and credit card accounts is how Experian Boost finds qualifying on-time bill payments. If you agree, these payments will be added to your credit report. The process takes about five minutes, and youll see any changes to your credit scores instantly. Most people who try Experian Boost see their credit scores improve immediately.

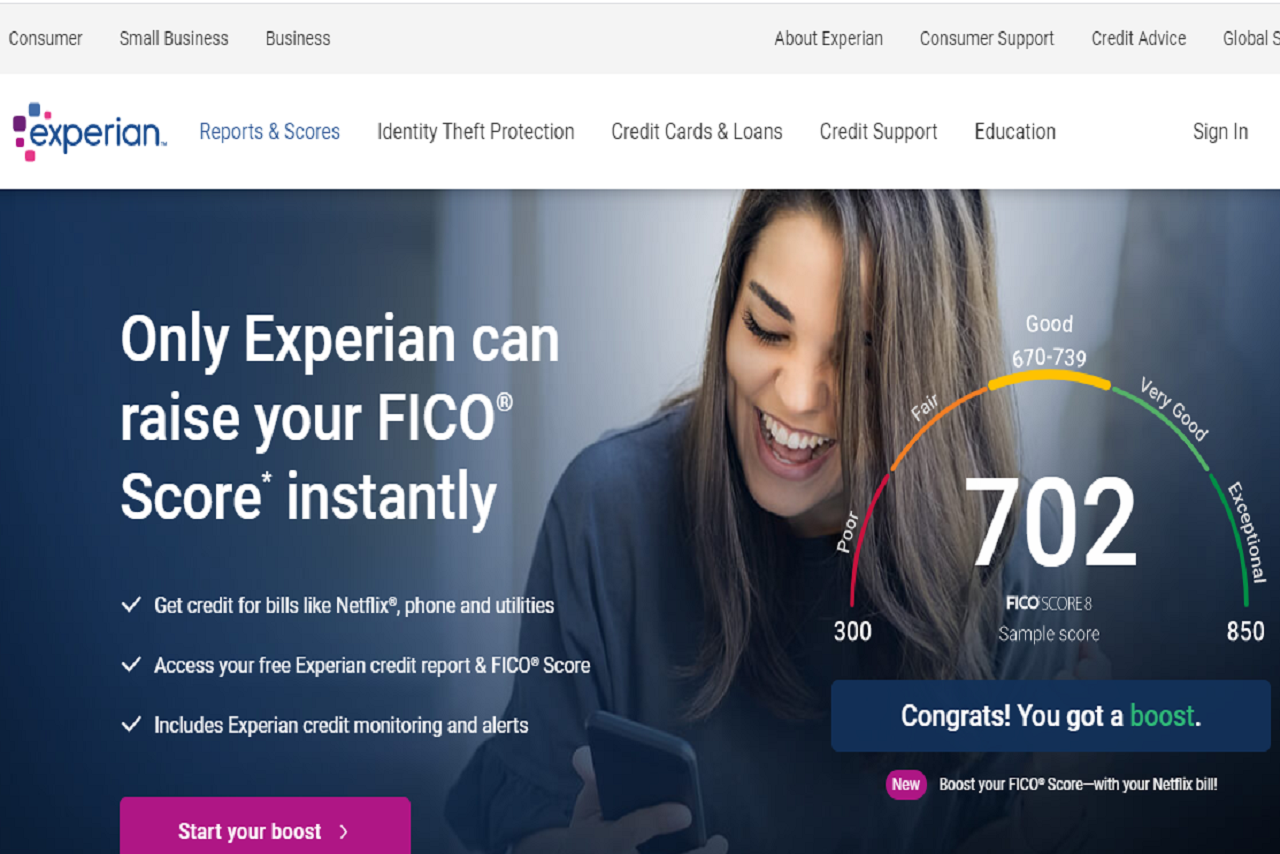

Average users boosted their FICO® ScoreΠ8 based on Experian data by 13 points. Some may not see improved scores or approval odds. Not all lenders use credit information impacted by Experian Boost.

Experian Boost is a free service from Experian that allows consumers to add additional payment history to their Experian credit report. This can help improve your FICO credit score. But an important question is – do lenders actually consider Experian Boost when making lending decisions? Here’s what you need to know

What is Experian Boost?

Experian Boost allows you to connect your bank account so Experian can scan for recurring payments you make for phone, TV/streaming services, utilities, and even rent. It looks for at least 3 on-time payments in the past 6 months.

You can choose to add your on-time payments to your Experian credit report if you have made them on time. This additional payment history can help boost your FICO Score.

On average, users who receive a boost improve their FICO Score by 13 points, according to Experian. But results can vary.

How Experian Boost Works

Here are the basic steps to use Experian Boost:

- Sign up for a free Experian account

- Connect your bank account so Experian can access your payment history

- Experian scans your bank transactions for recurring payments

- You select which positive payment history you want added to your Experian credit file

- If eligible payments are found, you may see an improved FICO Score instantly

The key is that Experian Boost is adding additional positive payment history that wasn’t previously being reported to your credit report. This helps make your credit file more robust.

Do All Lenders Consider Experian Boost?

The short answer is no. Not all lenders consider Experian Boost when making lending decisions. Here are some key factors:

Only Impacts Experian Credit Report

Experian Boost only adds data to your Experian credit file. It does not impact your credit reports at Equifax and TransUnion, the other two major credit bureaus.

And lenders can decide what to do based on credit reports from any of the three bureaus. If a lender looks at your Equifax or TransUnion report, Experian Boost won’t help them in any way.

Many Lenders Don’t Use FICO Scores

Even though FICO scores are the most common, there are a lot of other scoring models out there. And not all lenders use FICO scores.

For example, many credit card issuers develop their own proprietary credit scoring models. And some lenders may use VantageScore instead of FICO.

So even if Experian Boost improves your FICO score with Experian data, other credit scoring models are unaffected.

Most Mortgage Lenders Exclude Experian Boost

One of the most important lending decisions is getting approved for a mortgage. But most mortgage lenders specifically exclude any benefit from Experian Boost when evaluating your creditworthiness.

Why? Mortgage lenders tend to be conservative and want the most established credit history. The “boosted” payment history hasn’t been thoroughly validated over a long period of time, so mortgage lenders ignore it.

What Types of Lenders May Consider Experian Boost?

While it’s limited, there are some types of lenders that may give weight to the Experian Boost increased payment history:

- Lenders who specifically use Experian data and FICO scores in their decisions

- Lenders with more lenient underwriting policies who emphasize recent payment history

- Personal loan companies

- Credit card issuers (though many have custom scoring models)

- Auto lenders

- Peer-to-peer lenders like Prosper and LendingClub

So while it’s not universal, there are some situations where Experian Boost could potentially help with lending approvals and terms.

Tips to Maximize Your Chances with Experian Boost

If you want to use Experian Boost and increase your chances of it impacting a lending decision, consider these tips:

- Apply for credit from lenders specifying they use Experian data and FICO scores

- Focus on personal loans, credit cards, peer-to-peer lending, and auto loans where underwriting may be less strict

- Make sure you have a thorough credit history established before relying on Experian Boost

- Use Experian Boost along with other tactics to improve your overall credit scores

While it can be helpful, think of Experian Boost as just one credit-building tool in your toolbox. Combine it with other responsible credit behaviors.

The Bottom Line

Experian Boost can potentially help give your credit score a modest bump by adding more positive payment history to your Experian credit file. However, its impact on lending decisions is limited since it only affects one credit bureau and many lenders don’t even use the scores it improves.

But it is still a free service worth considering, especially if you have an established credit history and are strategic about applying for credit from lenders using Experian data and FICO scores. Just don’t expect Experian Boost alone to be a silver bullet for guaranteed loan approvals.

Will Lenders Use My Experian Boost Score?

Helping consumers raise their credit scores so they can obtain credit when they need it is one of the main reasons Experian Boost was created. Experian Boost impacts multiple credit scoring models, so as long as your lender utilizes the most common versions of the FICO® Score and VantageScore® credit score, they will see your boosted credit scores when they request your credit report from Experian.

You may even find lenders who recommend Experian Boost when youre getting ready to apply for a loan. For example, home equity lending specialist Spring EQ says Experian Boost has become a staple in their lending process and something they recommend to applicants when they believe it can make a difference in granting them a loan with lower interest rates and fees.

Make sure to keep your accounts connected when applying for new credit so lenders can see your boosted credit scores on your Experian report. If you disconnect your bank or credit card accounts from Experian Boost, your credit scores will be calculated without that additional information.

How Is Experian Boost Helping Consumers?

A growing number of people looking to improve their scores or establish credit history are trying Experian Boost and experiencing an instant credit score increase. In fact, people receiving a boost instantly raise their FICO® Score by an average of 13 points with Experian Boost.

Do Lenders Look at Experian Boost? – CreditGuide360.com

FAQ

Do lenders consider Experian Boost?

Most mortgage lenders do not consider credit scores impacted by Boost. Terms and conditions subject to change.

Is it a good idea to use Experian Boost?

In short, stay away from Experian Boost. It will only lead to a falsely high score that won’t be taken into account when lending decisions are made.

How can I raise my credit score by 100 points in 30 days?

Raising your credit score by 100 points in 30 days is an ambitious goal, but possible by focusing on key areas and taking proactive steps.

Do lenders look at Experian?

The credit score used in mortgage applications While the FICO® 8 model is the most widely used scoring model for general lending decisions, banks use the following FICO scores when you apply for a mortgage: FICO® Score 2 (Experian) FICO® Score 5 (Equifax).