You may already know that your credit score is mostly based on how well you’ve paid back loans and credit cards in the past. But according to the Consumer Financial Protection Bureau (CFPB), paying your utilities, rent and cell phone bills could also be a factor.

When it comes to credit scoring, those types of payments provide whatâs known as alternative data. If alternative data is reported to credit bureaus, paying bills on time can help build credit. Keep reading to learn how.

As a responsible adult, you know that paying your monthly bills on time is important. But did you know that paying these regular bills could also help you build your credit?

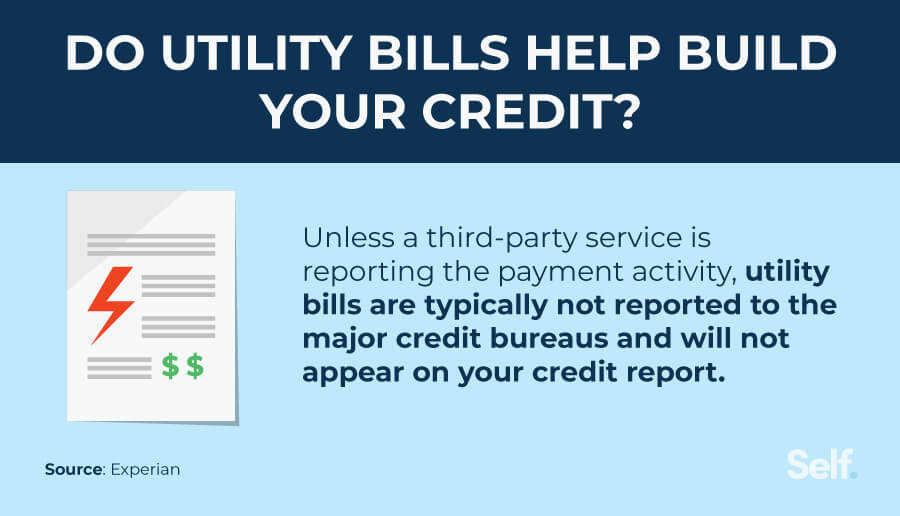

Utility payments like your gas, electric water phone, and cable bills are not automatically reported to the three major credit bureaus (Experian, Equifax, and TransUnion). So simply paying them usually won’t affect your credit score. However, new services are emerging that allow consumers to opt-in to credit reporting for utility and telecom payments.

This complete guide will explain how utility bill reporting works, which payments can be included, and how to get credit for paying on time. It will also talk about the possible cons and things you should think about before signing up.

Do Phone, Internet, and Cable Bills Help Build Credit?

Most cell phone, internet, and cable/satellite companies don’t tell credit bureaus about how well you pay your bills. That’s why paying these bills on time doesn’t always make your credit score better.

If you use a third-party reporting service, you may be able to report your phone and internet payments to one or more bureaus:

-

Experian Boost – Free service that reports phone, internet, streaming, and utility payments to Experian. Boosts FICO Scores based on Experian data.

-

RentTrack – Reports rent and utility payments to TransUnion for a monthly fee.

-

Payment Rails – Free service reporting rent, utilities, insurance, internet, and phone payments to Equifax.

-

Creditable – Paid service reporting rent and utility payments to all three bureaus.

The benefit is that positive payment history helps your credit, especially if you’re just starting to build credit. The downside is that late payments could also be reported and hurt your score.

Can Utility Bills Like Gas, Electric and Water Improve Your Credit?

Like phone bills, utility companies don’t automatically report your gas, electric, water, trash, and sewage payment history to the credit bureaus. So paying on time won’t help your credit score.

Again, services like Experian Boost, RentTrack, Payment Rails, and Creditable allow you to opt-in to utility bill reporting. They scan your bank transactions for utility payments and report positive payment history to one or more bureaus.

According to Experian, Boost users who added utility payments saw an average increase of 13 points in their FICO Score based on Experian data.

The services above can report gas, electric, water, trash collection, sewage, and heating fuel payments. Experian Boost also reports streaming services like Netflix, Hulu, Disney+, and Spotify.

Can Rent Payments Be Added to Your Credit Report?

Most landlords don’t report on-time rent payments to credit bureaus. So simply paying rent typically won’t improve your credit score.

Rent reporting services like Payment Rails, RentTrack, Creditable, and others allow tenants to opt-in to credit reporting of rent payments. They verify rent payments with the landlord before reporting positive payment history.

According to RentTrack, users saw an average credit score increase of 41 points within three months after adding rent to their credit reports.

Should You Sign Up for Utility and Rent Reporting?

Reporting services can be enticing if you want extra help building credit or improving your credit score. But make sure to consider the pros and cons before signing up:

Pros

-

On-time payments help credit scores

-

Useful for credit building if you have little other credit history

-

Extra motivation to pay rent and utilities on time

Cons

-

Late payments could hurt your credit

-

Monthly or annual fees with some services

-

Not reported to all three bureaus (except Creditable)

-

Data collection/privacy concerns

-

Time lag between payments and credit report updates

-

Some services require bank account access

Evaluate the costs against the potential credit benefit to decide if it’s right for you. And know you can report rent, utilities, and telecom payments indirectly by putting them on a credit card and paying on time.

Do Medical Bills and Insurance Payments Help Your Credit?

Simply paying medical bills and health insurance premiums on time does not typically improve your credit score. That’s because doctors, hospitals, clinics, and insurance companies generally don’t report your payment history to credit bureaus.

The exception is if you put medical payments on a credit card. Then it becomes a credit card payment that helps your score if paid on time. But avoid this if possible, as credit card interest rates can lead to higher medical costs.

While medical collections can hurt your credit, new rules set for 2025 will remove nearly all medical debt from credit reports. This will prevent medical bills from damaging scores.

Can Car Insurance Payments Build Your Credit?

Car insurance payments don’t influence your credit score. Auto insurance companies don’t report policyholders’ premium payment history to credit bureaus.

The only connection between car insurance and your credit occurs when applying for a policy. In most states, insurers will check your credit before determining your insurance rates. Applicants with lower credit scores tend to pay higher premiums.

But simply paying your car insurance on time won’t build your credit history or lead to better credit scores.

Do Late Utility and Rent Payments Hurt Your Credit?

If you sign up for a rent/utility reporting service, late payments could potentially hurt your credit score and show up as delinquencies on your credit reports. However, a single late payment likely won’t damage your credit significantly.

The real risk is if unpaid utility or telecom bills get sent to collections. Unpaid medical bills also often go to collections agencies. Having an account in collections severely damages your credit.

Even if utility and rental companies don’t report to credit bureaus, severely late or delinquent accounts could still go to collections and show up on your reports.

Can Prepaid Debit Cards for Utilities Improve Your Credit?

Some prepaid debit cards allow users to pay rent and utilities with the card, then report those on-time payments to credit bureaus. This helps build the user’s credit history.

For example, Chime Credit Builder and Self Credit Builder cards work this way. You load funds to the prepaid card, use it for eligible purchases like rent and utilities, then on-time payments are reported by the card issuer.

The benefit is you don’t need the billing companies to report payments – the card issuer does it automatically. Just be sure to make payments on time each month. Late payments can negatively impact your credit.

Do Personal Loans and Auto Loans Help Credit More Than Utilities?

Personal loans, auto loans, student loans, and mortgages are forms of “credit” – you borrow money and repay it over time. Timely repayment of installment and revolving credit helps builds your credit history and score.

Utilities and rent are ongoing expenses but not credit accounts – you aren’t borrowing money from those companies. So loans and credit cards have a more direct impact on your credit profile than paying bills.

That said, reporting services allow utility/rent payments to count toward your credit history. These payments help build credit, especially if you have few other credit accounts.

The Bottom Line

Utility, telecom, and rent payments don’t automatically help your credit score. But new opt-in services report these payments to credit bureaus, helping build your history if paid on time.

Consider the pros and cons before signing up for reporting services. Weight the costs against the potential credit benefit. And know you can report bills indirectly via credit cards.

While utilities themselves don’t build credit, timely payments are still crucial to avoid collections damage and maintain good financial health. Use utilities’ autopay features to ensure on-time payments every month.

Can late phone, rent and utility bill payments affect credit?

Itâs possible that getting behind on payments can lower credit scores even if the bills arenât being reported regularly.

Depending on how far behind payments get, the account could be turned over to a collections agency. The debt collector could make a negative report to the credit bureaus. Collections activity can stay on a credit report for seven years and sometimes longer, according to the CFPB.

You can learn more about how debt collections work from the CFPB.

How do utility, rent and phone bill payments appear on my credit reports?

Alternative data isnât as common as traditional factors used to judge credit. But if itâs reported, itâll appear on your credit reports as something called a tradeline. Tradelines include account information like payment history, account status, account activity and account history.

Do utility bills help build credit?

FAQ

Do utilities increase your credit score?

Paying non-credit bills like rent, utilities, and medical expenses on time won’t bump up your credit score because they’re usually not reported to credit bureaus. But if they’re very late or in collections, they’ll likely get reported and affect credit scores negatively. Sep 13, 2024.

Do you get credit for paying utilities?

Utility companies typically don’t report your payment history to the credit bureaus. But paying utility bills on time can help your credit score when you use Experian Boost. This tool specifically integrates gas, electric, water and other utility payments into your Experian credit report and scores.

What bill helps build credit?

Paying your mortgage, credit cards and loans on time will boost your score because they are reported to the three major credit bureaus. But not every account you pay is reported to the bureaus, so good behavior like paying rent and utility bills on time typically won’t help your score.

What brings your credit score up the fastest?

Keep paying your bills on time. In many credit scoring formulas, your payment history has the greatest effect on your overall credit scores. So, it’s critical to make payments on time.