When you want to buy a house, you work hard to make sure all of your financial plans are in order. As you pull together the paperwork, you may be wondering if you’ll be required to provide your tax returns to purchase a home.

The short answer is: maybe. Some types of loans do require you to provide your tax returns. But in many other cases, tax returns are not required.

Getting a mortgage is an exciting yet often stressful process, especially when it comes to providing all the required documentation. One key document that gives lenders insight into your finances is your tax return. But do you really need to provide tax returns when applying for a conventional loan?

The short answer is yes, most conventional loans need tax returns. There are, however, some exceptions and other choices you should think about if your tax situation is complicated. In this comprehensive guide, we’ll explore:

- What are conventional loans?

- Why lenders require tax returns

- When tax returns may not be needed

- Alternative documentation options

- How to get a conventional loan without tax returns

- Tips for borrowers with complex tax situations

What Are Conventional Loans?

Conventional loans are mortgages that conform to standards set by Fannie Mae and Freddie Mac. They have loan limits that typically change from year to year. For 2023, the baseline conforming loan limit is $726,200, while the limit is higher for expensive housing markets.

Conventional loans come in a variety of forms, including

- Fixed-rate mortgages (FRMs)

- Adjustable-rate mortgages (ARMs)

- Conforming jumbo loans

One of the best things about them is that they have lower requirements for eligibility and lower interest rates than government-backed loans. Conventional loans are given by private lenders instead of government programs.

Why Lenders Require Tax Returns

When reviewing a mortgage application, lenders need to verify the borrower’s income and get a complete picture of their financial situation. Tax returns provide key insights that help lenders assess eligibility and risk.

Here are some of the main reasons lenders require tax returns:

-

Validate income—Tax returns help lenders see how much and where the borrower gets their money. The lender needs to know that the applicant has a steady source of income to pay the monthly bills.

-

Assess income stability – By reviewing 2 years of returns, lenders can see how consistent the applicant’s income has been over time. Large fluctuations may be a red flag.

-

Review deductions—Lenders check to see if deductions lower taxable income by a large amount. Large write-offs could mean the borrower makes more money than they report.

-

Confirm self-employment income – For self-employed borrowers, tax returns help establish the viability of their business by showing net profit.

-

Check for other properties – Tax returns reveal any rental income, making it possible to factor in those mortgage payments in eligibility assessments.

-

Verify creditworthiness – Returns provide info like profits, losses, and dividends that help paint a financial picture and indicate creditworthiness.

So in short, tax returns are a standard requirement because they help lenders thoroughly evaluate income, stability, deductions, assets/liabilities, and credit risk. This allows them to make prudent lending decisions.

When Tax Returns May Not Be Needed

While tax returns are the norm, there are some scenarios where they may not be required to get a conventional loan:

Recent graduates – Applicants who have graduated college recently may not have 2 years of tax returns available if they only joined the workforce. In such cases, W-2s and paystubs may suffice.

Entering retirement – Older borrowers preparing for retirement may have left their long-term jobs. For them, lenders may approve conventional loans just with retirement account statements and social security award letters.

Major life events – After events like divorce or death of a spouse, lenders may approve loans based on the applicant’s current income situation documented via pay stubs and W-2s.

Rapid income increase – If income rose sharply since the last tax filing, lenders may be willing to base decisions on the most recent paystubs rather than older returns.

Specific lender programs – Some conventional loan programs, like Fannie Mae’s HomeReady mortgage, have flexible requirements allowing alternate income documentation for lower-income borrowers.

So in certain scenarios, it is possible to get a conventional mortgage approved without submitting tax returns. That said, the bar is high, and such cases are more exception than norm.

Alternative Documentation Options

If your tax situation is complex, here are some alternative documents you can provide to apply for a conventional loan:

-

Written VOE – A written verification of employment from your employer explaining your income. This avoids having to document highly variable incomes.

-

1099s – For self-employed borrowers who get 1099 forms instead of W-2s.

-

Profit and loss statements – To establish income for self-employed individuals.

-

CPA letters – An explanation letter from your accountant verifying your income.

-

Business tax returns – Business returns alongside personal returns if you have an ownership stake in a business.

-

Asset statements – Bank/investment statements to demonstrate assets, which is crucial for jumbo conventional loans.

-

Gift funds – Gift letters validating any gift money you receive toward your downpayment or closing costs.

So make sure to discuss alternatives with lenders to provide documents that give an accurate picture of your finances and income. With some creativity, you may be able to get approved without having to submit personal tax returns.

How to Get a Conventional Loan Without Tax Returns

Here are tips for improving your chances of qualifying for a conventional mortgage without having to provide tax returns:

-

Improve your credit score – A higher score demonstrates creditworthiness and reduces risk for lenders. Aim for at least 740.

-

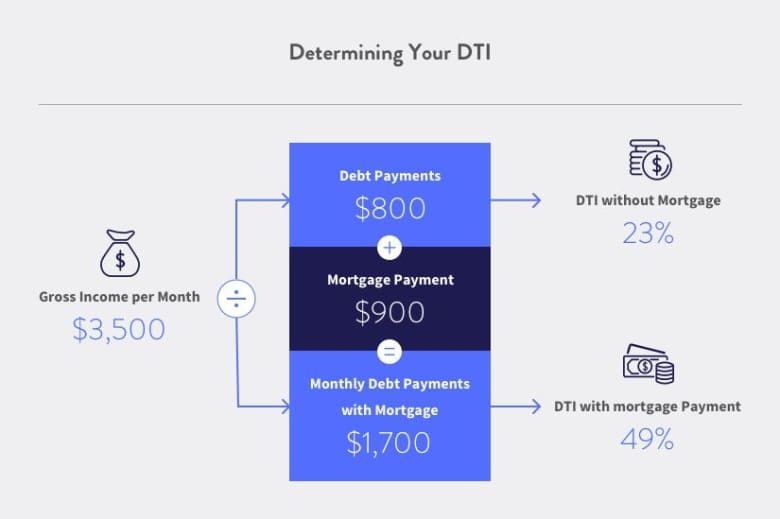

Lower your DTI – Keep debt-to-income ratios low. If you have a DTI below 36%, lenders may be more flexible.

-

Make a larger down payment – Putting down 20% or more gives lenders confidence to potentially waive tax return requirements.

-

Know guidelines – Ask lenders in advance about alternative documentation for your situation instead of assuming tax returns are mandatory.

-

Consider a jumbo loan – Jumbo conventional loans rely more on your assets and credit profile than income documentation.

-

Work with smaller lenders – Smaller banks and credit unions may be more open to alternative documentation than big banks.

-

Get co-signers – Having a co-signer with strong credit could make lenders comfortable approving your conventional loan without tax returns.

-

Provide explanation letters – Draft letters explaining any complexities or discrepancies in your finances to reassure lenders.

The bottom line is that you need to demonstrate your ability to repay the mortgage according to the lender’s conventional loan program guidelines. While unlikely, it is possible in certain situations if you take proactive steps to provide alternative documentation and mitigate risk.

Tips for Borrowers With Complex Tax Situations

If you have a convoluted tax scenario due to self-employment, investments, business ownership, or other complexity, here are some tips that can help your application:

-

Consult an accountant – They can explain deductions, advise on minimizing red flags, and provide necessary documentation.

-

File an extension – Get more time to sort through your paperwork if your taxes aren’t ready. Just make sure to provide returns once available.

-

Gather additional statements – Have documents beyond returns available to give lenders more context, like business bank statements, invoices, commercial leases, etc.

-

Clarify one-time events – If returns were impacted by a onetime life event, draft an explanatory letter highlighting that it doesn’t reflect your normal situation.

-

Consider an alternative loan – If your tax quagmire makes documentation too difficult, non-conforming loans may offer more flexibility and options.

-

Apply with multiple lenders – Complex borrowers may want to cast a wider net and apply with several lenders to increase chances of approval.

-

Talk to lenders upfront – Have candid conversations with lenders early about your scenario to determine what alternative documents could work instead of assuming tax returns are an absolute requirement.

With proactive planning, advice from tax professionals, and smart communication, even borrowers with tangled tax histories can get conventional mortgages approved.

Key Takeaways

-

Tax returns are generally required for conventional loans to verify income, stability, deductions, and creditworthiness. However, exceptions exist in some cases.

-

Alternatives like written VOE, 1099s, P&L statements, CPA letters, and asset statements may suffice if your tax situation is complicated.

-

Improving your credit, having a larger down payment, finding flexible lenders, and providing explanatory documentation can help secure approval without returns.

-

Proper preparation, input from tax experts, collecting supplemental docs, and having open talks with lenders enables borrowing even with complex tax scenarios.

While daunting, a conventional mortgage without tax returns is possible in special cases with the right game plan and persistence. But make sure to be upfront with lenders about your particular situation. With some work, you can hopefully transform the tax return roadblock into an approved loan!

Step 2: Maximize your credit score

Lenders use tax returns or W-2s and pay stubs to confirm your income, but your credit score helps them evaluate how likely you are to pay your debts (and how much debt you have). No matter which type of loan you apply for, you must meet certain credit score requirements.

Of course, those are credit score minimums in “normal” times. During the pandemic, many mortgage lenders are imposing overlays on loans, which means that minimum scores will likely be higher.

The better your credit score, the better your rate and likelihood of qualifying for a loan, particularly a non-QM loan, if you don’t want to share your tax returns.

Step 6: Get pre-approved for a loan

It’s now time to get pre-approved for a loan.

A loan pre-approval is an early approval based on information you give the lender, which may or may not be checked by them. It lets you know how much of a loan you can afford and the terms the lender is willing to give you.

If you’re in the market for a non-QM loan, tell lenders that you want a bank statement or low-document loan and see what they have to offer.

You should talk to more than one lender about any type of loan you want to make sure you get the best terms.

5 Ways to Qualify for a Mortgage Without Tax Returns!

FAQ

Does a conventional loan require tax returns?

Conventional Loans (Fannie Mae & Freddie Mac) Require at least two years of tax returns for self-employed borrowers. If a borrower is a W-2 worker, tax returns may not always be needed as long as their income is stable and pay stubs are enough proof.

Do you need to show tax returns to get a loan?

What you’ll need: Tax returns – The lender will need to see full versions of your federal tax returns, typically the two most recent years.

Can you get a mortgage without showing tax returns?

A no-doc mortgage, also known as a no-income verification mortgage, allows you to get a home loan without having to prove how much you make through a pay stub …Feb 26, 2025.

Do I need 2 years of tax returns to buy a house?

How many years of tax returns do I need for a mortgage? Most lenders will need between one and two years of your personal and business (if applicable) tax returns in order to figure out how much money you make.