Have you ever wondered if naming a beneficiary on your accounts protects your wishes after death, or if your spouse could still claim those assets? This is a common concern in estate planning, and the answer isn’t as straightforward as you might think

At our law firm we often see clients confused about whether their spouse can override their chosen beneficiary designations. Let’s break down this complex topic into simple understandable terms.

The General Rule: Beneficiaries vs. Spouses

Generally speaking, a properly designated beneficiary on an account will receive those assets upon your death, even if your will states otherwise. This is because beneficiary designations typically supersede other estate planning documents.

However, this doesn’t mean your spouse has no rights. Several factors can determine whether a spouse can override a beneficiary designation

- Where you live (community property vs. non-community property states)

- Type of asset involved (bank accounts, retirement accounts, life insurance)

- Specific state laws governing spousal rights

- Federal regulations like ERISA for certain retirement accounts

Community Property States: A Special Case

If you live in a community property state, your spouse might have stronger claims against beneficiary designations. In these states, assets acquired during marriage are generally considered jointly owned.

Community property states include:

- Arizona

- California

- Idaho

- Louisiana

- Nevada

- New Mexico

- Texas

- Washington

- Wisconsin

For residents of Texas and other community property states, your spouse could potentially claim half of community property assets, regardless of beneficiary designations.

Bank Accounts: Can a Spouse Override a Beneficiary?

When it comes specifically to bank accounts, the designated beneficiary will typically receive the funds after the account holder’s death, regardless of the spouse’s wishes. As our colleagues at Bineham & Gillen explain:

“In most cases, a spouse cannot directly override a beneficiary designation on a bank account. The designated beneficiary will receive the funds regardless of the spouse’s wishes unless the account holder changes the beneficiary designation before their death.”

This means if you’ve named your child or another person as the beneficiary of your bank account, that designation usually stands even if your spouse objects.

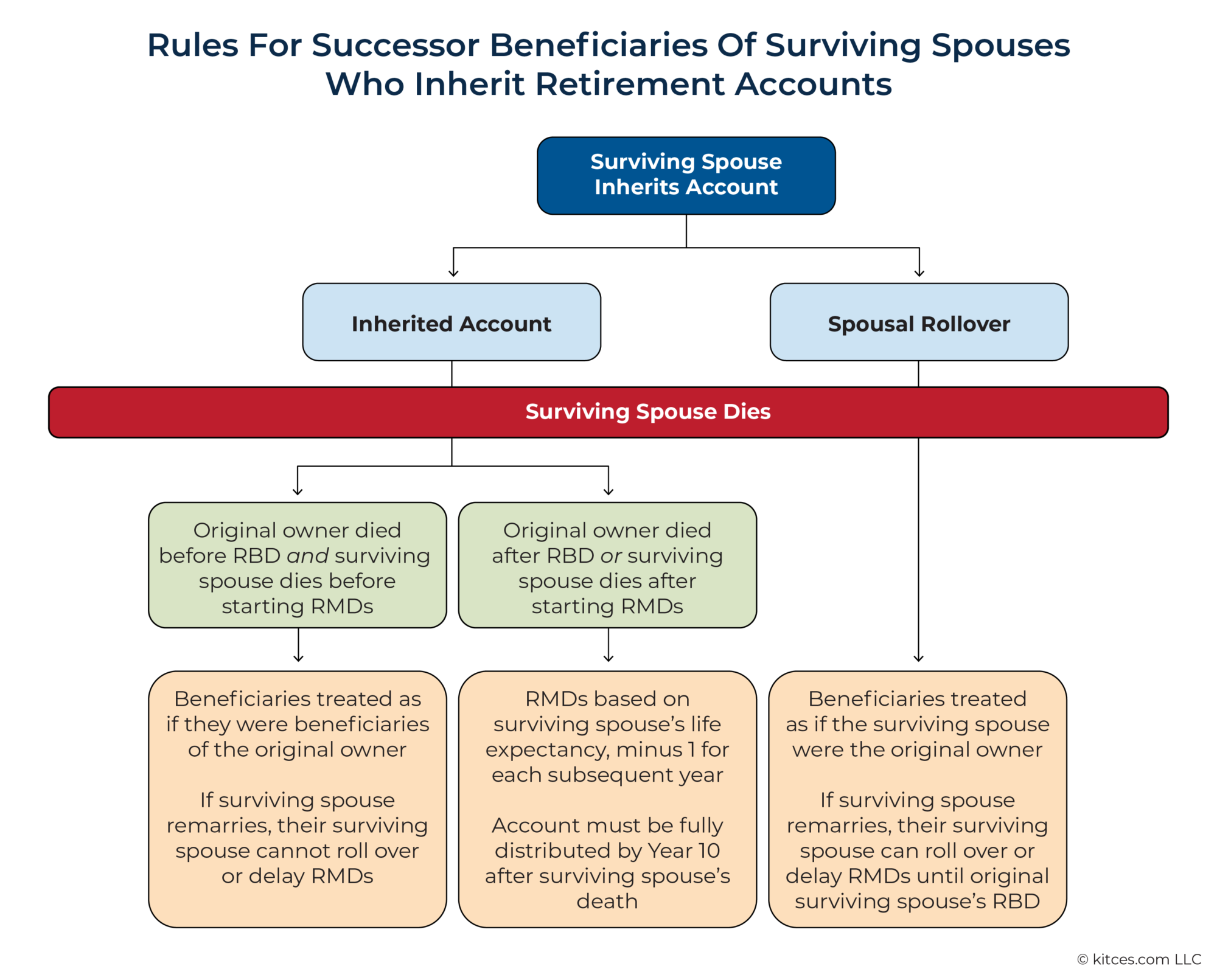

Retirement Accounts: A Different Story

Retirement accounts follow different rules, particularly employer-sponsored qualified pension plans governed by ERISA (Employee Retirement Income Security Act). These include:

- 401(k) plans

- 403(b) plans

- Employee Stock Ownership Plans (ESOPs)

- Simplified Employee Pension (SEP) plans

For these accounts, federal law provides special protections for spouses. Under ERISA rules, your spouse automatically inherits your qualified retirement plan assets, even if you’ve named someone else as beneficiary, unless your spouse has signed a waiver consenting to another beneficiary.

As one expert notes: “Under ERISA rules, the qualified pension plan automatically goes to your spouse even if you name another beneficiary. The only exception is if your spouse signs a waiver agreeing to your choice of another beneficiary.”

Life Insurance Policies: More Flexibility

With life insurance policies, you typically have more freedom to name non-spouse beneficiaries without spousal interference. However, in community property states, if premiums were paid with community funds, your spouse may have rights to a portion of the proceeds.

Can a Power of Attorney Change Beneficiaries?

A related question we often receive is whether someone with power of attorney can change beneficiary designations. The standard answer is no – unless the power of attorney document specifically grants this authority.

As estate planning attorneys note: “Typically, a standard POA does not grant the agent the power to change beneficiaries on bank accounts unless explicitly stated in the document.”

What Can Override a Beneficiary Designation?

While beneficiary designations are powerful, they can sometimes be challenged or overridden in specific situations:

-

Spousal rights in community property states – Your spouse may have legal claims to certain assets regardless of beneficiary designations

-

ERISA protections for qualified retirement plans – Federal law gives spouses automatic rights to these accounts

-

Legal challenges based on undue influence or coercion – If someone can prove you were forced or manipulated into naming a beneficiary

-

Divorce in some states – Some states automatically revoke ex-spouse beneficiary designations upon divorce (though not all do)

Practical Steps to Protect Your Wishes

To ensure your assets go to your intended recipients, consider these steps:

-

Regularly update beneficiary designations, especially after major life events like marriage, divorce, or having children

-

Consult with an estate planning attorney familiar with the laws in your state

-

If you want a non-spouse to receive retirement benefits, work with your spouse to complete the necessary waiver forms

-

Consider using trusts for more complex estate planning needs

-

Keep beneficiary designations and estate planning documents consistent where possible

The Importance of Clear Documentation

One of the most effective ways to avoid conflicts between spouses and beneficiaries is to maintain clear, updated documentation of your wishes. This includes:

- Current beneficiary designation forms

- A comprehensive, up-to-date will

- Detailed trust documents (if applicable)

- Written explanations of your intentions

So, does a beneficiary override a spouse? The answer is: it depends on several factors including the type of asset, where you live, and applicable state and federal laws.

For bank accounts, the named beneficiary generally prevails. For qualified retirement plans, federal law often gives spouses priority unless they’ve signed a waiver. And in community property states, spouses may have rights to assets regardless of beneficiary designations.

Estate planning is complex, which is why working with qualified professionals familiar with the laws in your state is essential. By understanding these nuances and taking proactive steps to document your wishes, you can help ensure your assets are distributed according to your desires.

Remember, proper estate planning isn’t just about directing where your assets go—it’s about providing clarity and peace of mind for yourself and your loved ones during difficult times.

Have you reviewed your beneficiary designations lately? It might be time for a check-up.

Legal Insights: Beneficiary Designations And Spousal Rights

When it comes to managing financial accounts and ensuring your wishes are honored following your passing, understanding the nuances of beneficiary designations is crucial. One common question that arises is whether a spouse can override a beneficiary on a bank account.

The team at Bineham & Gillen aims to clarify this issue and provide insight into related topics, such as the role of power of attorney and how to find assets after death.

A beneficiary designation on a bank account determines who will inherit the account’s funds after the account holder passes away. This designation typically precedes other forms of estate planning, such as a will.

For instance, if you name your child as the beneficiary of your bank account, that designation usually stands, even if your will states otherwise.

Can A Spouse Override A Beneficiary?

In most cases, a spouse cannot directly override a beneficiary designation on a bank account. The designated beneficiary will receive the funds regardless of the spouse’s wishes unless the account holder changes the beneficiary designation before their death.

However, certain circumstances, such as community property laws in some states, might affect how assets are distributed. It’s important to consult with an attorney to understand the specific laws applicable in our part of Texas.

Can a Will Override Beneficiaries from a Previous Marriage?

FAQ

Can a beneficiary override a spouse?

The general rule of thumb is that a beneficiarycould override a spouse when it comes to asset receipt, except in the following situations. Community property states. If you and your spouse live in a community property state, then your individual retirement account, life insurance policy, or real estate trust might be considered community property.

Can a spouse override a life insurance policy?

If you find out that someone else is the beneficiary on your spouse’s life insurance policy, you cannot override the policy. Generally, the policyowner — who is also usually the person who pays the premiums — can name anyone they choose as the beneficiary. No one else can make adjustments to the policy.

Can a spouse override a legatee’s rights?

On the other hand, even if you name a beneficiary other than your spouse to a retirement account or other asset, there are some instances in which the rights of your husband or wife might override those of the appointed legatee. But not always.

Can I name multiple beneficiaries?

You can name multiple beneficiaries to receive either equal or different portions. In most states, the primary beneficiary will receive the full payout even if they’re not your current spouse. (This applies even if you named your ex as your beneficiary and didn’t update your policy).

Can you have multiple beneficiaries on a life insurance policy?

You can list multiple primary and secondary beneficiaries on your policy and decide what portions of your payout should go to each. People assume that a will is ironclad, but a beneficiary designation supersedes it. This applies not just to beneficiaries for life insurance policies, but for annuities and retirement, brokerage, and bank accounts.

Is a spouse considered a beneficiary of a life insurance policy?

In community property states, a spouse is automatically considered the life insurance beneficiary unless they indicate explicitly otherwise in the policy. All property acquired during the marriage is considered jointly owned by both spouses, regardless of who earned it or whose name is on the title.

Does a life insurance beneficiary override the spouse?

Key takeaways. A life insurance beneficiary designation usually overrides a current spouse or a will.

Can my husband take me off as a beneficiary?

Whether you can remove your ex-spouse as a beneficiary depends on the terms of your divorce. If you’re the policyholder and won’t be supporting your ex after the divorce, you might be able to remove them. But if you have to pay alimony or child support, you may have to keep them as a beneficiary.

Is your spouse automatically your beneficiary if you are married?

Key Takeaways

Marital property generally transfers automatically to the surviving spouse. Separate property is divided according to the deceased person’s will or intestate laws if there is no will.

What can override a beneficiary?

An executor can override a beneficiary when they are acting in accordance with state statutes, the terms of a will and the level of legal authority they’ve been granted by the court to administer an estate.