It can be easy and convenient to pay your bills with a credit card, which can also help you earn rewards, get extra time to pay, and make your finances easier by putting all of your expenses on one statement. But could using plastic to pay all of your monthly bills hurt your credit? The short answer is “it depends.”

When used responsibly credit cards can help build your credit history and scores. But charging bills you can’t afford or carrying balances can damage your credit. To understand the potential impact you need to consider both how and which bills you pay by card.

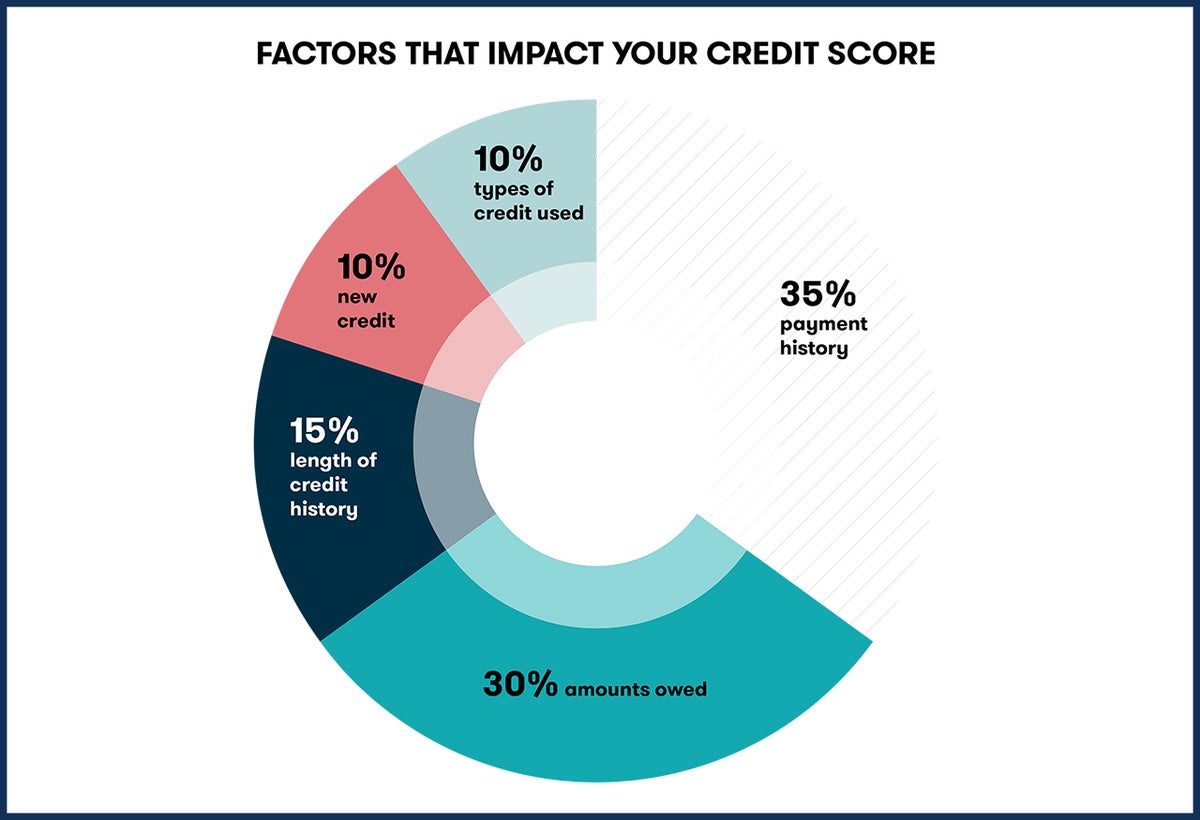

How Credit Card Use Affects Your Credit Scores

The two biggest factors credit scoring models like FICO and VantageScore use to calculate your scores are payment history and credit utilization. Together, these two categories make up 65% or more of your scores

-

Your payment history shows if you always pay your bills on time every month. Making payments on time for a long time raises your credit score; late payments lower it.

-

Credit utilization is the percentage of your total credit limits you’re using. Experts recommend keeping this below 30%. Maxing out cards hurts your scores.

So using a credit card to pay for things could help you build your credit history if you pay it off on time and in full every month and don’t use too much of your available credit.

But if you carry balances, miss payments, or max out your cards, relying on credit cards to pay bills can damage your credit through late payments and high utilization.

Which Bills Help or Hurt Your Credit When Paid by Card

Not all bills are created equal when it comes to how paying them with a credit card affects your credit.

Bills That Help

-

Credit cards: Since credit card payments are sent to credit bureaus automatically, always paying your bills on time can help your credit score.

-

Loans – Installment loans like personal loans, student loans, and auto loans are also regularly reported. Paying these with a card if allowed can build your credit history.

-

Utilities – If your utility company reports on-time payments, charging these bills to earn rewards can help. Many don’t report, however.

-

Rent – Paying rent with a card through a service like Plastiq has potential to help. But fees often make this impractical.

Bills That Hurt

-

Mortgage – Most lenders don’t accept credit cards for mortgage payments to avoid processing fees. If yours does, the high balance could hurt through utilization.

-

Medical Bills – Paying medical expenses with a card is generally not recommended. If unpaid, medical bills can seriously damage your credit.

-

Bills You Can’t Afford – Putting bills on a card when you don’t have the cash to pay hurts through high utilization and potential late payments.

Neutral Bills

-

Cell Phone – On-time cell phone payments typically aren’t reported unless seriously delinquent. But rewards could make using a card worthwhile if no fees.

-

Insurance – Paying insurance bills with a card earns rewards with no credit impact as long as you pay on time. But some insurers charge fees.

-

Cable/Internet – Like cell phones, on-time payments usually aren’t reported. Rewards cards can make sense for these if no fees.

Tips to Pay Bills With a Credit Card Without Hurting Your Credit

Paying bills with a credit card strategically can help your credit while earning rewards. Follow these tips to avoid hurting your scores:

-

Only charge bills you can afford to pay in full each month to avoid interest and credit damage.

-

Keep utilization low by limiting charges to 30% or less of your credit limits.

-

Make sure payments post on time by setting payment reminders and automating payments.

-

Avoid fees that erase rewards by researching which providers accept cards at no cost.

-

Be selective about which bills go on your card, avoiding large recurring costs like rent and mortgage.

-

Compare cards to find the best fit based on the types of bills you pay regularly. Cash back cards may suit utility bills, for example, while travel rewards work for insurance.

-

Consider the sign-up bonus when applying for a new card, and meet minimum spend organically through bills rather than overspending.

The Bottom Line

When used wisely and with financial discipline, credit cards can help establish positive payment history and improve your credit profile over time. But paying bills you can’t afford or carrying a balance can hurt your credit through late payments and high utilization.

Being selective about which bills you charge, keeping balances low, paying on time, and avoiding fees allows you to earn rewards without credit damage. Monitoring your credit scores also helps you catch any impacts early before they become lasting problems.

Other ways to build credit

Building credit can be simple, but it takes some discipline. Here are our top tips to improve your credit score:

How to get credit for your bills

It’s possible to get credit for paying your bills on time, even if your payments aren’t reported to the credit bureaus. Here’s how:

- Use a credit card when possible. It’s possible to use a credit card to pay some bills. As long as you pay your credit card bills on time every month, this can help you build credit. In the table above, you can see what bills you can pay with bank cards. Keep an eye out for surcharges and convenience fees, though. If using a credit card costs more, find another way to pay. There are other, cheaper ways to build credit.

- Sign up for Experian Boost. You can add your cell phone, utility, and rent payments to your Experian credit report for free with Experian Boost. You can raise your FICO Score and show that you’ve made payments on time on your Experian credit report for this. One thing to keep in mind is that Experian Boost only lets you add payments to your Experian credit report. Your TransUnion and Equifax reports won’t be affected.

- Report your rent payments. There are companies that will report your rent payments to the credit bureaus, but most of them will charge you a fee. For example, Boom costs $3 a month to report your rent, and Credit Rent Boost costs $6. 95 a month.

Along with LendingTree Spring, you can get free, personalized advice on how to improve all the things that affect your credit score. We’ll show you how your credit stacks up and what to do to boost your score.

Does Carrying a Balance on a Credit Card Hurt Your Credit Score? (Q&A)

FAQ

Is it bad to use a credit card to pay bills?

It might affect your credit scores: If you can’t pay off your credit card balance after paying your bills with a credit card, you could increase your credit …Feb 27, 2025.

Does paying bills on credit card affect credit score?

If you use a credit card or the company reports the payment to the credit bureaus, paying a bill will hurt your credit. When a person or company reports your payments (or nonpayments), the credit bureaus will add this information to your credit report — this will impact your credit score.

How much does paying off a credit card affect your credit score?

Paying off debt is more likely to help your credit scores than to hurt them. You are likely to see your credit scores improve after paying off debt unless the debt you repaid meets the unique criteria listed above.

Does your credit score go down when you use your credit card?

No, the act of using a credit card itself won’t necessarily lower your credit score. Actually, being smart about how you use a credit card—like making payments on time every month and keeping your balance low—can help your score.