Mortgage servicers play a crucial behind-the-scenes role in the home lending industry. But how exactly do these companies turn a profit? In this comprehensive guide, we’ll demystify mortgage servicing and break down the key ways servicers generate revenue.

What Is a Mortgage Servicer?

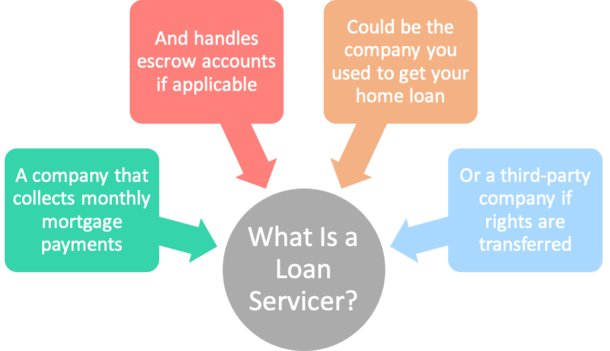

A mortgage servicer is a business that takes care of the day-to-day management and administration of mortgage loans. Servicers act as intermediaries between borrowers and investors. Their key responsibilities include:

- Collecting monthly mortgage payments

- Maintaining escrow accounts and paying property taxes and insurance

- Sending account statements and paperwork to borrowers

- Distributing payments to mortgage investors

- Overseeing foreclosures and loan modifications

In essence, servicers take care of all the grunt work associated with mortgage loans after they are originated. This frees up lenders to focus on their core business – originating new loans.

Now let’s look at the main ways mortgage servicers generate income from this administrative work.

1. Servicing Fees

The primary source of revenue for servicers is servicing fees. These fees are typically expressed as a percentage of the outstanding principal balance of the mortgages in a servicer’s portfolio.

Servicing fees range from 0.25% to 0.50% per year. So for a $200000 mortgage the servicer would earn between $500 to $1000 annually in servicing fees. These fees are collected monthly, so the servicer earns 1/12th of the annual fee each month.

Servicers collect higher fees for riskier loans with lower credit scores. Subprime loans often have servicing fees of 0.50% or more. Meanwhile, prime conventional loans with good credit can have fees as low as 0.25%.

2. Float Income

Mortgage servicers collect payments from borrowers at the beginning of each month but may not remit them to investors until weeks later During this time, the servicer can invest the accumulated payments and earn interest income – known as float income

For large servicers with tens of billions worth of monthly payments, even a small amount of float income can add up to significant profits.

3. Ancillary Fees

Servicers earn various ancillary fees and charges in the normal course of mortgage administration:

-

Late fees – Typically around 5% of the monthly payment amount, charged when borrowers pay after the due date.

-

Modification fees – Fees for processing loan modifications, forbearances, or repayment plans for delinquent borrowers.

-

Convenience fees – Charges for online payments, expedited payments, or over-the-phone payments.

-

Prepayment penalties are fees that people have to pay when they pay off their mortgage early or switch lenders.

These many small fees can add up to a big profit center, especially when the economy is bad and more people fall behind on their payments.

4. Mortgage Servicing Rights (MSRs)

Mortgage servicing rights, or MSRs, are things that servicers get in exchange for taking care of a group of loans. Servicers can buy and sell MSRs, just like they can buy and sell loans.

When mortgage rates decline, existing MSRs become more valuable because borrowers are less likely to prepay or refinance their mortgages. Servicers can then sell the rights at a profit.

Conversely, when rates rise, prepayments accelerate, decreasing the value of MSRs.

5. Interest on Escrow Accounts

Servicers collect borrowers’ property tax and insurance payments into escrow accounts before disbursing them annually or semi-annually. Until those payments are made, the funds sit in the servicer’s accounts earning interest.

While not a primary profit driver, any interest earned contributes incrementally to a servicer’s bottom line.

The Controversial Nature of Servicing Compensation

The servicing fee structure has attracted controversy over the years. Critics argue it incentivizes some negative servicer behaviors:

- Disincentives to help borrowers build equity and pay off loans faster.

- Perverse incentives to drag out or avoid loan modifications.

- More incentives to foreclose than facilitate alternative options.

Reform advocates have called for changes to the servicer compensation model to better align with positive borrower outcomes. But the industry maintains the current model is necessary to compensate servicers for the effort and risks involved.

Key Takeaways: How Mortgage Servicers Generate Revenue

- Main source of income is servicing fees charged as a percentage of outstanding loan balances.

- Additional revenue streams from float income, ancillary fees, mortgage servicing rights sales, and interest on escrow accounts.

- Compensation structure controversial due to disincentives perceived to harm borrowers.

- Reforms proposed but fiercely resisted by the industry.

Understanding how mortgage servicers make money provides key insights into this little-understood sector critical to housing finance in America. Appropriate compensation balances the needs of borrowers, servicers, and investors – but striking that balance remains an ongoing debate.

What Is Loan Servicing?

Loan servicing refers to the administrative aspects of a loan from the time the proceeds are dispersed to the borrower until the loan is paid off. Loan servicing includes sending monthly payment statements, collecting monthly payments, maintaining records of payments and balances, collecting and paying taxes and insurance (and managing escrow funds), remitting funds to the note holder, and following up on any delinquencies.

- Loan servicing is a function carried out by the bank or financial institution that issued the loan, a third-party vendor, or a company that specializes in loan servicing.

- Loan servicing functions include collecting monthly payments, paying taxes, and other aspects of the loan that occur from the time the proceeds are dispersed until the loan is paid off.

- Securitization of loans made loan servicing less profitable for banks.

- Loan servicing is now an industry in and of itself and companies are compensated by receiving a small percentage of loan payments.

Loan Servicing Example

Loan servicing is now an industry in and of itself. Loan servicers are compensated by retaining a relatively small percentage of the outstanding balance, known as the servicing fee or servicing strip. This fee usually amounts to 0.25 to 0.5 percentage points of each periodic loan payment.

For example, if the monthly mortgage payments are $2,000 and the servicing fee is 0.25%, the servicer is entitled to retain $5—or (0.0025 x 2,000)—of each payment before passing the remaining amount to the note holder.

How Do Mortgage Servicers Make Money? – CountyOffice.org

FAQ

How does mortgage servicing work?

Mortgage servicing has a few layers. The mortgage note holder and the groups that get paid from an escrow account for things like property tax, homeowners insurance, mortgage insurance premiums, HOA dues, and so on get paid by the servicer. The lender originated your loan. How do mortgage lenders make money?.

How do mortgage servicers make money?

Mortgage servicers also earn income from sources such as interest on escrow accounts and float income. Funds held for property taxes and insurance premiums earn interest on escrow accounts. Float income comes from holding borrower payments for a short time before sending them to investors.

How do mortgage lenders make money?

There are many ways for mortgage lenders to make money, such as through origination fees, discount points, closing costs, mortgage-backed securities (MBS), loan servicing, and yield spread premiums. Closing costs fees that lenders may make money from include application, processing, underwriting, loan lock, and other fees. What does a mortgage servicer do?.

What does a mortgage servicer do?

Mortgage servicing rights are sold by the originator of a mortgage to another financial institution, which then takes over the administration of the mortgage, which includes such tasks as collecting payments and forwarding them to the originator. The original lender pays the servicer a fee for performing this work. How much do loan servicers make?

What are some additional ways loan servicers earn money?

Loan servicers make their dough by taking a slice of the pie—specifically, a cut of each mortgage payment you make. They also earn a few extra bucks from fees for late payments or other loan management services. It’s a bit like being a landlord, but for loans.

How do loan servicers generate revenue?

Loan servicers generate revenue by taking a cut of each mortgage payment you make. Additionally, they earn money from fees for late payments or other loan management services. This is similar to how a landlord makes money, but for loans.

How do mortgage services make money?

The income from servicing mortgage loans derives from a number of sources: the servicing fee paid by the mortgage loan investor, the interest earned on the …

How does the loan servicer generate profit?

Loan servicing is now an industry in and of itself. Loan servicers are compensated by retaining a relatively small percentage of the outstanding balance, known as the servicing fee or servicing strip. This fee usually amounts to 0.25 to 0.5 percentage points of each periodic loan payment.

How much do mortgage servicers get paid?

How much does a Mortgage Servicing make in California? As of Jun 11, 2025, the average hourly pay for a Mortgage Servicing in California is $20.93 an hour.

How do loan servicers get paid?

Loan servicers are compensated by collecting a small percentage of each periodic loan payment, known as a servicing fee.