Youâve finally sold your house and are happy with the deal. Naturally, your next question is: When do I get my money after closing? Getting your money can take anywhere from a few days to a few weeks, depending on how you choose to be paid and how the closing goes. Â.

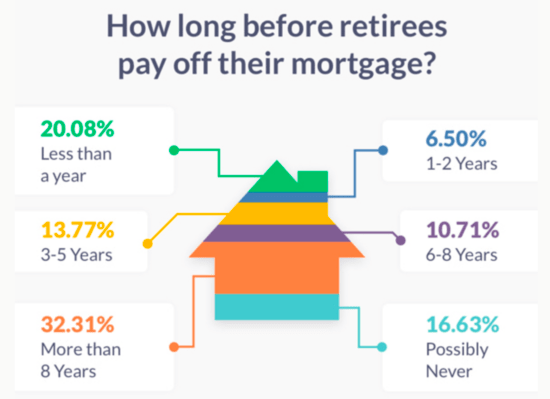

Paying off your mortgage is a major financial milestone that many homeowners aspire to reach. However, the path to being mortgage-free isn’t always straightforward. If you’ve recently closed on a home loan, you may be wondering: how long after closing will my mortgage be fully paid off?

The answer depends on a few important factors that affect how long it takes you to pay back the loan. This guide has all the information you need to know about how long it takes to pay off your mortgage after closing. It also has tips to help you get to mortgage freedom faster.

Understanding the Basics: Loan Term, Interest Rate and Amortization

When you close on a mortgage three essential elements determine your repayment period

-

Loan Term – The agreed upon length of time to repay the loan, commonly 15, 20 or 30 years. Longer terms mean lower monthly payments but higher total interest paid over the life of the loan.

-

Interest Rate – The annual percentage rate charged on the mortgage loan, Lower interest rates reduce the total interest paid and allow more of your payment to go towards paying down the principal balance

-

Amortization – The schedule of principal and interest payments. An amortization table shows how each payment is allocated and tracks the declining loan balance over time.

Most mortgages today use level amortization, with payments structured so the amount applied to principal slowly increases over the loan term while interest decreases. This means in the early years of your mortgage, the majority of your payment covers interest costs.

The Impact of Your Loan Term

The loan term you choose significantly impacts how long it takes to pay off the mortgage. Let’s compare:

-

15 Year Mortgage – With 180 monthly payments, a 15 year mortgage is paid off in 15 years. Total interest paid is lower compared to longer terms. Monthly payments are higher.

-

20 Year Mortgage – 240 monthly installments pay off the loan in 20 years. Interest paid is moderate and monthly payments are manageable.

-

30 Year Mortgage – The longest common term at 360 months (30 years). This allows lower monthly payments by spreading repayment over more time, but total interest paid is higher.

A shorter term means you pay off your mortgage faster, but make sure you can afford the higher monthly payment before you sign. Know how much you can spend and pick a term length that works for you.

Accelerating Your Mortgage Payoff Timeline

You don’t have to be stuck with the standard amortization schedule and original payoff date. There are several ways to pay your mortgage down faster and reduce the years until payoff:

-

Make Extra Principal Payments—Even adding $50 to $100 more to your principal balance every month can cut years off of your loan.

-

Pay Biweekly – Making half your normal payment every two weeks (26 per year) equates to one extra monthly payment annually, accelerating paydown.

-

Recast/Re-amortize – After making large lump sum payments, you may be able to recast the loan to lower your payment while keeping the same payoff date.

-

Refinance – If rates drop significantly, refinancing to a lower rate can shorten your term and reduce total interest paid.

Careful planning and discipline are needed to implement these accelerated strategies. But with consistent effort, you could pay off your 30 year mortgage in closer to 20 or 25 years and become mortgage free sooner.

Your First Mortgage Payment After Closing

You’ll begin making mortgage payments shortly after the loan closes:

-

The first payment is usually due 30 to 60 days after the closing. Your lender will inform you of the exact date.

-

This first payment will be for the same amount as your regular monthly mortgage installments going forward.

-

Payments must remain current every month until the loan is satisfied. Late or missed payments can damage your credit score and lead to fees.

Coordinate with your lender to set up your payment method, whether automatic bank drafts, online, by phone or mailed checks. Making on-time payments is essential.

Special Considerations for Prepayment and Payoff

While paying your mortgage off early can save on interest, some loans contain restrictions to watch for:

-

Prepayment Penalties – Some mortgages, especially older loans, penalize paying too far ahead or refinancing within a certain timeframe. Check your loan documents.

-

Escrowed Funds – Any money reserved in your escrow account for taxes and insurance will be reimbursed after the loan is satisfied.

-

Home Equity Loans – If you have a HELOC, home equity loan/line, or second mortgage, these amounts will also need to be paid off when you pay off your primary mortgage.

Consult your lender regarding any prepayment clauses or other loan stipulations that may impact your payoff plans. Being aware of these details ensures you can pay off your mortgage smoothly and avoid any unexpected fees or complications.

Staying the Course Towards Mortgage Freedom

Embarking on your journey to pay off your home loan can seem daunting at first. But taking it step-by-step and keeping the end goal in mind will help you make consistent progress. Here are some final tips for achieving mortgage payoff success:

-

Maintain open communication with your lender so you fully understand your loan’s terms, balance paydown and the payoff process.

-

Make a budget, trim expenses where possible, and allocate those savings towards extra principal payments. Small amounts add up over time.

-

Monitor your amortization schedule and loan balance so you can track your payoff progress and stay motivated.

-

Refinance when appropriate to secure better rates and accelerate your timeline if possible.

-

Celebrate important milestones like when you’ve paid off 10%, 25% and halfway! Mark your calendar for the exciting day your long-awaited mortgage payoff finally arrives.

The more informed you are about your mortgage repayment process, the smoother your journey will be towards reaching mortgage freedom. With a thoughtful approach and consistent effort, you can take charge of your situation and achieve the dream of paying off your home loan ahead of schedule.

Pros and Cons Of A Cashierâs Check

| Pros | Cons |

|---|---|

| â¢Typically costs less. â¢Can be more secure than an electronic transfer. â¢Can be ready in as little as one business day. | â¢More potential for delays either from the bank or the mail carrier. â¢Less convenient. â¢You may have to visit a local branch in person. |

What Is Delayed Disbursement?Â

Sometimes, there can be a delay in the payment of escrow funds after closing. When this does happen, itâs often because of an issue with the lenderâs underwriting or loan documentation. In the worst situations, it could be because the buyer’s finances changed in a big way that caused the mortgage to fall through. Â Â.

It’s been a week since the closing, and you still haven’t been paid. You should call the escrow agent to find out what happened and when you can expect to get the money. Then, review the purchase agreement to see if there are any penalties for a delay that requires the buyer to pay you interest in the interim. Â.

What happens when you make your last mortgage payment?

FAQ

How long does it take to pay off a mortgage?

When you pay off a mortgage, the original deed of trust is sent back to you by the mortgage holder marked “paid” or “cancelled. Usually, this takes up to sixty days. But since deeds are public records, you can check with your county registrar to see how things are going. Why you shouldn’t pay off your house early?.

How will my mortgage be paid off at closing?

At closing, your mortgage will be paid off using the proceeds from the sale. Here’s how it typically unfolds: A few days before closing, your lender will provide a “payoff statement” showing the exact amount needed to pay off your mortgage.

What happens if you sell a house before closing?

You’re responsible for mortgage payments until the day of closing. The proceeds from the sale are used to pay off your existing mortgage at closing. Any remaining balance after paying off the mortgage and closing costs becomes your profit. Continue making regular payments throughout the selling process to avoid credit issues.

When should I make my last payment before closing?

So read on for helpful information about the payoff process and the timing of your last payment before you close your sale. TL/DR; The timing of the last payment depends on the date of the closing and the seller’s mortgage terms. In general, we recommend sellers make the final payment 7 days before closing.

What happens if my mortgage is paid off?

If you’re like most people, your taxes and insurance were part of your monthly mortgage payment. Your loan servicer held the funds in escrow and made the payments on your behalf. But now that your mortgage is paid off, your lender will close your escrow account and send you the remaining balance.

What happens if I make my last mortgage payment?

Once you’ve made your last mortgage payment, it’s your responsibility to make sure that your mortgage note or deed of trust is released from your county’s office of land records. You can do this by filing a certificate of satisfaction. Some lenders do this for their clients. What happens when you make your last mortgage payment?.

How long after closing on a house do you pay a mortgage?

Your first payment will be due the first of the month 30 days after closing. For example, if you close your loan on February 15, your first mortgage payment on your new loan will fall on April 1. You will not have a payment due on March 1.

How long after closing are funds disbursed?

“In states that require postclosing lender review [known as ‘dry funding’], disbursement may take two to three business days. ” The states that have dry-funding laws: Arizona. California.

What is the 2% rule for mortgage payoff?

If you want to pay off your mortgage quickly, the 20%222% rule says to try to get a new interest rate that is 2% lower than your current rate. This helps ensure that the savings generated by refinancing outweigh the costs associated with it.

How long does it take for a mortgage to show as paid off?

Please allow 60 to 90 days after your loan is paid in full before contacting them for a copy of the lien.