Receiving a pre-screened offer or using a tool to check for pre-approval can be a great way to understand your credit card options. And getting pre-approved for a credit card typically wonât impact your credit scores.

Find out how the terms pre-approval, pre-qualify and pre-screen are used. Plus, learn how card issuers can check your eligibility without hurting your credit scores.

Before you buy a house, it’s important to get pre-approved for a mortgage. Sellers will see that you are a serious buyer who has been checked out by a lender. A lot of people who want to buy a house wonder if getting pre-approved for a mortgage will hurt their credit score. The short answer is that it might go down a few points for a short time. However, mortgage pre-approval has big advantages that far outweigh this small drawback.

In this article, we’ll explain:

- What mortgage pre-approval is

- Why pre-approval is recommended

- How pre-approval affects your credit score

- Tips for minimizing the credit impact

- How to offset any effects on your score

What Is Mortgage Pre-Approval?

Pre-approval involves submitting financial documents and undergoing a credit check so a lender can verify your finances. If approved you’ll receive a pre-approval letter stating the loan amount and terms you qualify for.

This shows sellers you’re a low-risk buyer who has been thoroughly vetted. Sellers often prefer offers from pre-approved buyers.

Pre-approval is not the same as pre-qualification, which is based only on verbal information and doesn’t check your credit or confirm your income.

Why Get Pre-Approved for a Mortgage?

Here are some key benefits of getting pre-approved:

-

Know your budget. You can find out how much of a home loan you can get by getting pre-approved. This helps you make a budget that you can stick to and keeps you from looking at homes that you can’t afford.

-

Stronger bargaining position. Sellers favor pre-approved buyers since there’s less risk of the sale falling through. This gives you an edge in competitive markets.

-

Speeds up the process. After your offer is accepted, the mortgage process goes faster because your credit and income have already been checked.

-

Lock in current rates. Interest rates fluctuate daily. Locking in your rate during pre-approval holds that rate for 60-90 days in most cases.

While pre-approval can slightly lower your credit score, the advantages make it an essential step for serious homebuyers.

How Does Pre-Approval Affect Your Credit Score?

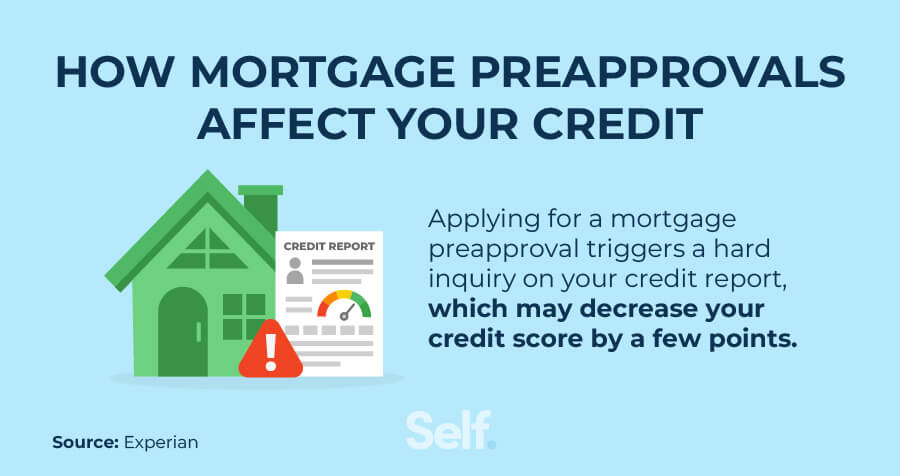

When you apply for mortgage pre-approval, the lender does a hard inquiry on your credit report. Too many hard inquiries in a short period can lower your score.

However, for pre-approval you can apply with multiple lenders in a short timeframe without accumulating multiple hard inquiries. The credit bureaus understand rate shopping is common with mortgages.

Here’s how multiple pre-approval inquiries affect your credit:

-

If you apply with several lenders within 14 days, the inquiries will be treated as a single inquiry.

-

With newer FICO models, you get a 45-day window for mortgage rate shopping.

So checking rates with 3 different lenders would count as a single hard inquiry as long as you apply within 14-45 days. This minimizes the impact to your score.

How Many Points Could Pre-Approval Drop Your Score?

The drop varies, but is generally minor. Here’s how much your credit score could decrease:

-

1-5 points – Typical impact of a single hard inquiry

-

10-15 points – If you apply outside the 14-45 day rate shopping window

This small drop will recover within a few months as you continue paying bills on time.

Tips to Minimize the Credit Score Impact

You can take a few steps to reduce the effect of pre-approval on your credit:

-

Compare rates in a short period – Applying within 14-45 days results in fewer hard inquiries.

-

Limit applications – Don’t apply for new credit cards or loans while getting pre-approved.

-

Avoid new hard inquiries – Soft inquiries from checking your own credit won’t affect your score.

-

Check all three credit reports – Make sure there are no errors that could negatively impact your credit.

How to Offset the Credit Score Effect

If your credit score drops after getting pre-approved, here are some ways to offset the dip:

-

Pay all bills on time. Payment history is the biggest factor affecting your credit. Stay diligent.

-

Pay down balances. Keep credit card balances low and pay off debt to lower your credit utilization.

-

Wait it out – Your score will recover within six months as long as you practice good credit habits.

-

Become an authorized user – Being added as an authorized user on someone’s credit card with good payment history can give your score a boost.

-

Dispute errors – If your credit report contains mistakes, file disputes to correct errors and raise your score.

The Bottom Line

While mortgage pre-approval can result in a minor temporary drop in your credit score, it signals to sellers you’re a serious buyer and paves the way for a smoother home buying process. As long as you minimize credit inquiries and continue using credit responsibly, the dip should be small and short-lived. The benefits of getting pre-approved far outweigh this negligible downside.

Is there a way to opt out of pre-approved credit card offers?

If youâd rather not receive pre-approval offers, you can opt out for five years or permanently at optoutprescreen.com or by calling 888-5-OPT-OUT (888-567-8688).

Does pre-approval affect your credit scores?

Pre-approval typically involves a soft credit inquiry. Also known as a soft pull or soft credit check, a soft inquiry doesnât affect your credit scores. Itâs simply a way for lenders to determine whether you may qualify for their credit card offer.

Does Pre-approval Affect Credit Scores? – CreditGuide360.com

FAQ

Does a credit card preapproval affect your credit score?

A preapproval letter tells you how likely it is that you will be approved for new credit and what interest rate you might get. Some types of preapprovals, like for a credit card, won’t hurt your credit, but getting preapproved for a mortgage or car loan might.

Does a mortgage preapproval affect your credit score?

A mortgage preapproval can result in a hard inquiry on your credit report, which can temporarily lower your credit score by a few points. So, getting preapproved for a mortgage is a smart move that should be made before you buy a house. The good news is that this ding on your credit score is temporary.

Do preapproved offers affect my credit score?

Generally, preapproved offers, such as those from credit card issuers, don’t directly impact your credit score. But once you accept the preapproval, the lender will likely review your credit history as part of a more thorough final approval process, which will result in a hard inquiry.

Will preapproval affect my FICO score if I’m a first-time homebuyer?

Green said mortgage preapproval could lead to a five- to 10-point drop in a borrower’s FICO score if they’re a first-time homebuyer with limited credit history. Applicants with a long history of responsible credit use may see less impact, depending on the information in their application.

How long does a better mortgage pre-approval take?

A Better Mortgage pre-approval takes as little as 3 minutes to complete and uses a soft credit check to give you an idea of how much you can borrow without impacting your credit score. If you receive a promotional letter from a bank stating that you’ve been pre-approved for a new credit card, the bank has run a soft credit check on you.

Does a prequalification affect my credit score?

A prequalification typically won’t affect your credit score because a hard inquiry usually isn’t involved, while a preapproval may affect your credit score since hard inquiries are more common. But not all lenders will use these definitions so be sure to find out what’s involved before starting the process.

How many points does your credit drop when getting pre-approved?

Getting pre-approved does not hurt your credit score. As we discussed earlier, a pre-approval may require running a soft inquiry, which, unlike a hard inquiry, does not hurt your credit score.

How much does a pre-approval affect credit score?

How much does 1 credit check affect credit score?

In general, credit inquiries have a small impact on your FICO Scores. For most people, one additional credit inquiry will take less than five points off their FICO Scores. For perspective, the full range for FICO Scores is 300-850. Inquiries can have a greater impact if you have few accounts or a short credit history.

Does credit one pre-approval affect credit score?

Pre-qualifying won’t harm your credit score.