Ever found yourself staring at your retirement account balance and wondering, “Is this enough?” You’re not alone. I’ve spent countless nights crunching numbers and worrying if my nest egg will keep me comfy through my golden years. The truth is figuring out how much you need monthly to retire comfortably can feel like solving a complex puzzle with missing pieces.

But don’t worry – I’ve done the heavy lifting for you. In this article, we’ll break down exactly what you need to know about monthly retirement income requirements without the financial jargon that makes your head spin.

The Big Question: How Much Money Do I Actually Need?

Let’s cut to the chase. According to recent analyses, the annual cost to retire comfortably varies drastically across the United States – by as much as $66000 between states! When we break this down monthly the differences are still substantial.

For example:

- In Mississippi (the cheapest state for retirees), you’ll need about $4,589 per month ($55,074 annually)

- In Hawaii (the most expensive), prepare to shell out around $10,102 monthly ($121,228 annually)

That’s a HUGE difference! And these figures aren’t just basic living expenses – they include what experts call a “comfort buffer” of 20% on top of essential costs to ensure you can actually enjoy your retirement.

The Reality Check: Common Retirement Funding Rules

Before we dive deeper, let’s talk about some common rules of thumb that financial experts use. These can give you a starting point for your retirement planning:

The 10% Rule

This suggests saving 10-15% of your gross income each year during your working life. If you make $60K yearly, that means setting aside $6,000-$9,000 annually for retirement. Honestly, I wish someone had told me this when I started working!

The 4% Rule

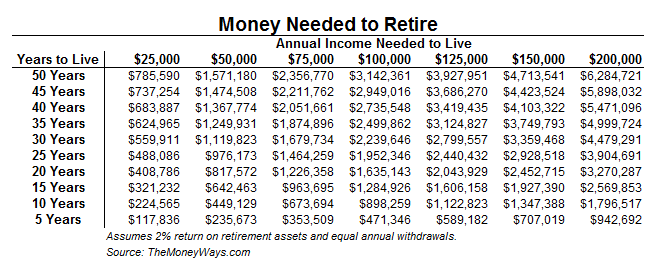

This is a biggie. It suggests you can withdraw 4% of your total savings in the first year of retirement, then adjust for inflation after that. So if you need $40,000 per year, your magic number would be $1 million in savings ($40,000 ÷ 0.04).

The 25x Rule

Similar to the 4% rule, this suggests saving 25 times your expected annual spending. Planning to spend $50,000 yearly in retirement? You’ll need $1.25 million saved up.

The 80% Rule

Another popular guideline suggests you’ll need 70-80% of your pre-retirement income to maintain your standard of living. So if you make $100,000 now, plan for $70,000-$80,000 annually in retirement.

I personally think the 80% rule makes the most sense for most people. Your mortgage might be paid off, but healthcare costs typically go up, and you’ll want extra cash for all those retirement activities you’ve been dreaming about!

Breaking Down Your Monthly Retirement Needs

Now let’s get practical. To determine your monthly needs, we gotta consider several factors:

1. Basic Living Expenses

These vary wildly depending on where you live:

| Expense Category | Monthly Cost Range |

|---|---|

| Housing | $800-$3,000+ |

| Food | $300-$600 |

| Healthcare | $400-$1,000 |

| Transportation | $200-$600 |

| Utilities | $200-$500 |

Living in California? Expect to need about $7,533 monthly ($90,399 annually). Prefer Tennessee? You could get by on around $4,904 monthly ($58,854 annually).

2. Lifestyle Choices

This is where things get personal. Ask yourself:

- Do you want to travel extensively?

- Plan to dine out frequently?

- Have expensive hobbies?

- Want to help support family members?

Each “yes” adds to your monthly requirement. Be honest with yourself here! There’s no point planning for a bare-bones retirement if you’re gonna be miserable.

3. Healthcare Considerations

This is the expense that surprises most retirees. Even with Medicare, you’ll face out-of-pocket costs. The average 65-year-old couple retiring today might need around $300,000 saved JUST for healthcare throughout retirement! That breaks down to roughly $500-$1,000 monthly depending on your health.

State-by-State: Where Your Retirement Dollar Goes Furthest

Location matters ENORMOUSLY for retirement planning. Let’s look at some monthly figures for comfortable retirement across different states:

Most Affordable States (Monthly):

- Mississippi: $4,589

- Kansas: $4,741

- Oklahoma: $4,709

- Alabama: $4,731

- Iowa: $4,790

Most Expensive States (Monthly):

- Hawaii: $10,102

- District of Columbia: $8,332

- Massachusetts: $8,142

- California: $7,533

- New York: $7,370

I was shocked to see such big differences! If you’re flexible about location, moving from California to Mississippi could literally cut your required monthly retirement income in half.

Sources of Retirement Income: Covering Your Monthly Needs

Now that we know what we need, where’s all this money coming from? Most retirees rely on a combination of:

Social Security

The average Social Security benefit is around $1,700 monthly in 2023. That’s nowhere near enough for most people to live comfortably! Social Security was designed to replace only about 40% of your working income, yet approximately one-third of workers and 50% of retirees expect it to be their major income source.

Retirement Accounts

Your 401(k), 403(b), 457 Plan, or IRA will likely form the backbone of your retirement income. If you withdraw using the 4% rule from a $1 million nest egg, that’s about $3,333 monthly.

Pensions

If you’re lucky enough to have one! Traditional pensions are becoming rare, but government employees and some corporations still offer them. This could provide anywhere from a few hundred to several thousand dollars monthly.

Personal Savings

This includes your regular savings accounts, CDs, and other investments outside retirement accounts. While important for liquidity, these often don’t keep pace with inflation.

Passive Income

Rental properties, dividends, or even a small business can generate ongoing monthly income. I have a friend who bought two rental properties specifically for retirement income and now collects about $3,000 monthly!

Calculating Your Personal Monthly Number

Ready to figure out your own number? Let’s break it down into steps:

Step 1: Estimate Your Monthly Expenses in Retirement

Start with your current expenses, then adjust:

- Subtract: work-related costs, mortgage (if it’ll be paid off)

- Add: increased healthcare, travel, hobbies

- Don’t forget: taxes, insurance, and inflation!

Step 2: Determine Your Retirement Income Gap

- Calculate expected monthly Social Security benefits

- Add expected pension income (if applicable)

- The difference between these and your monthly expenses is your “gap”

Step 3: Calculate How Much You Need to Save

To generate the monthly income to fill your gap, you’ll need to save:

- For every $1,000 of monthly income needed (using the 4% rule), you need $300,000 saved

- So if your gap is $3,000 monthly, you’d need approximately $900,000 saved

I used the retirement calculator at SmartAsset to run some scenarios, and it was eye-opening. For someone making $80,000 annually who wants to retire at 65 with 80% of their pre-retirement income, they’d need to save about $700 monthly starting at age 40 to avoid a shortfall.

Adjusting Your Plan: Making the Numbers Work

If there’s a gap between what you need and what you’re on track for, don’t panic! You have options:

Work a Few Extra Years

Working until 67 instead of 65 can increase your monthly retirement income by 15-20% through:

- More time to save

- Fewer years of withdrawals

- Higher Social Security benefits

Reconsider Your Location

As we’ve seen, moving from Hawaii to Mississippi could save you over $5,500 monthly! Even less drastic moves can make a huge difference.

Boost Your Savings Rate

Increasing your savings by even 3-5% of your income can translate to hundreds of thousands more over time. I recently upped my 401(k) contribution by just 2% and was surprised how little I noticed it in my paycheck!

Create Additional Income Streams

Consider rental properties, dividend stocks, or part-time work in retirement. Many retirees I know actually enjoy working 10-15 hours weekly – it provides structure and social connection along with income.

Common Mistakes to Avoid

Through my research and conversations with financial advisors, I’ve identified these common pitfalls:

1. Underestimating Longevity

Plan to live to at least 95! Running out of money is the worst-case scenario.

2. Forgetting About Inflation

What costs $50,000 today will cost about $90,000 in 20 years with just 3% inflation. Your monthly needs will increase significantly over time.

3. Overlooking Healthcare Costs

Medicare doesn’t cover everything, and long-term care can devastate savings. Consider long-term care insurance or setting aside specific funds.

4. Withdrawing Too Much Too Soon

The early years of retirement can be the most active and expensive, but withdrawing too aggressively can derail your entire plan.

5. Not Diversifying Income Sources

Relying too heavily on any one source (even a 401(k)) can leave you vulnerable to market downturns or policy changes.

Real-Life Example: Meeting Monthly Retirement Needs

Let me share a quick example of how this might work:

Meet Sarah:

- Current income: $75,000/year

- Retirement goal: $5,000 monthly ($60,000 annually)

- Expected Social Security: $2,200/month

- Small pension: $800/month

- Income gap: $2,000/month

To generate $2,000 monthly using the 4% rule, Sarah needs about $600,000 saved. She’s 45 with $150,000 already saved. Using a retirement calculator, she determined she needs to save about $850 monthly for the next 20 years to reach her goal.

This felt overwhelming until she:

- Increased her 401(k) contribution to get her full employer match

- Set up an automatic monthly transfer to her IRA

- Decided to work part-time for the first 5 years of retirement

With these adjustments, her plan became much more achievable!

Take Action Today

Here’s what you can do right now to figure out your monthly retirement needs:

-

Use a retirement calculator – The SmartAsset retirement calculator is a great place to start. It considers factors like your location, current savings, and expected retirement age.

-

Meet with a financial advisor – Even one session can provide valuable insights tailored to your situation.

-

Track your current spending – You can’t plan for retirement expenses if you don’t know your current ones!

-

Maximize your employer match – This is literally free money toward your monthly retirement income.

-

Consider opening an IRA – If you’ve maxed out your employer plan or don’t have one, an IRA offers tax advantages that can boost your retirement savings.

Remember, the journey to retirement is a marathon, not a sprint. Small, consistent actions today will pay off hugely in your monthly retirement income later.

Final Thoughts

So, how much do you need monthly to retire? The answer varies widely based on location, lifestyle, and longevity. But now you have the tools to figure out YOUR number.

For most people, monthly retirement needs fall between $4,000 and $8,000 for a comfortable lifestyle. That typically requires retirement savings between $1 million and $2 million, depending on your other income sources.

What’s your retirement number? Have you calculated how much you’ll need monthly? I’d love to hear your thoughts and plans in the comments below!

And remember – it’s never too late to improve your retirement outlook. Even small changes today can mean thousands more in monthly income during your golden years.

Happy planning!

How Much Do I Need to Retire? 5 Numbers to Help You Decide.

FAQ

How much money do you need to retire?

For example, the most common retirement goal among Americans is a $1 million nest egg. But this is faulty logic. The most important factor in determining how much you need to retire is whether you’ll have enough money to create the income you need to support your desired quality of life after you retire.

How much should you save for retirement?

Some experts claim that savings of 15 to 25 times of a person’s current annual income are enough to last them throughout their retirement. Of course, there are other ways to determine how much to save for retirement. The calculations here can be helpful, as can many other retirement calculators out there.

How much should you budget for retirement?

A common rule is to budget for at least 70% of your pre-retirement income during retirement. This assumes some of your expenses will disappear in retirement, and 70% will be enough to cover essentials. Remember, that’s a general guideline, and your needs may vary. Here’s more on how much to save for retirement.

How much money can you take out during your first year of retirement?

The 4% rule says that in your first year of retirement, you can withdraw 4% of your retirement savings. So, if you have $1 million saved, you would take $40,000 out during your first year of retirement either in a lump sum or as a series of payments.

How much money do you need for a 20 year retirement?

Retirees with less than $500,000 in savings can fund 20 years of a comfortable retirement in just four states. These include Louisiana ($499,020), Arkansas ($489,937), Mississippi ($442,620) and West Virginia (the cheapest state for a comfortable 20-year retirement at $434,501 in savings).

How much money can you make a year after retirement?

For example, if a person made roughly $100,000 a year on average during his working life, this person can have a similar standard of living with $70,000 – $80,000 a year of income after retirement. This 70% – 80% figure can vary greatly depending on how people envision their retirements.

Is $4000 a month enough to retire?

If your Social Security and other retirement savings allow you to retire on $4,000 per month, you’re likely in good shape to retire in many cities nationwide or abroad. Aside from the most expensive markets, $48,000 annually is enough for a comfortable retirement for many retirees.

Can I retire at 60 with 500k in savings?

Can you retire at 70 with $400,000?

It is 100% possible to retire with $400,000, provided you’re not looking to enjoy a particularly expensive retirement lifestyle or hoping to leave the workforce notably early.

Is $5000 a month good for retirement?

To retire comfortably, many retirees need between $60,000 and $100,000 annually, or $5,000 to $8,300 per month. This varies based on personal financial needs and expenses.