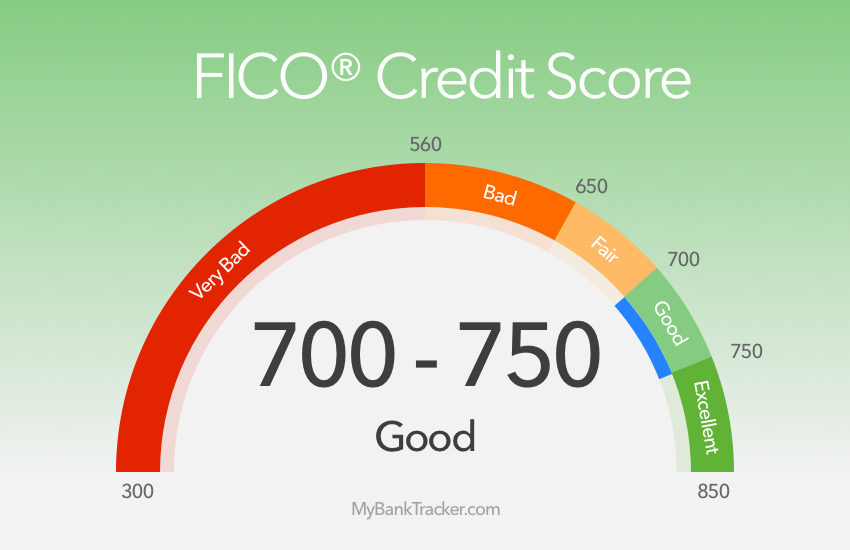

For a score with a range of 300 to 850, a credit score of 670 to 739 is considered good. Credit scores of 740 and above are very good while 800 and higher are excellent.

For credit scores that range from 300 to 850, a credit score in the mid to high 600s or above is generally considered good. A score in the high 700s or 800s is considered excellent. About a third of consumers have FICO® ScoresÎ that fall between 600 and 750âand an additional 48% have a higher score. In 2023, the average FICO® Score in the U. S. was 715.

Lenders use their own criteria for deciding whom to lend to and at what rates. But if your credit score is higher, you may be able to get a credit card or loan with better terms and a lower interest rate. The two main types of credit scores, the FICO® Score and VantageScore® credit scores, vary slightly in their ranges but have similar scoring factors.

Your credit score is one of the most important numbers in your financial life. It can determine whether you qualify for credit cards, loans, mortgages, rental applications, and more. But with scores ranging from 300 to 850, what does your number actually mean?

In particular, a credit score of 660 often leaves people wondering – is 660 a good credit score, or a bad one?

This guide will tell you everything you need to know about what a 660 credit score means about your creditworthiness and money habits.

- What a 660 credit score means

- Whether 660 is considered good or bad

- How a 660 credit score impacts your ability to get credit

- Tips for improving a 660 credit score

What Does a 660 Credit Score Mean?

A 660 credit score falls right on the border between fair and good credit, according to both the FICO and VantageScore scoring models.

Specifically:

-

If you have 660, your FICO score is near the top of the “fair” range (580–669).

-

On the VantageScore model, 660 is on the low end of the ‘good’ credit tier (660-740).

Even though it’s not great, a score of 660 is still pretty good and shows that you usually handle your credit responsibly. Some important things that a 660 credit score shows about your credit history are

-

You probably have a good mix of different types of credit, such as credit cards and loans that you pay back over time. Lenders want to know that you can handle different kinds of credit well.

-

You probably have a decent credit history length of at least 3-5 years. Time is an important factor in FICO and VantageScores.

-

You may have a late payment or two in the last couple years, but overall make payments on time. Payment history is the biggest factor in your scores.

-

Your credit card balances are under 50% of your total credit limits. High balances can drastically lower your scores.

While not perfect, these characteristics demonstrate pretty healthy credit management. But there’s still clear room for improvement to reach the 700+ “good” and 740+ “excellent” credit tiers.

Is a 660 Credit Score Good or Bad?

Given its position between fair and good credit ranges, whether a 660 credit score is good or bad depends on your perspective.

On the positive side:

-

A 660 FICO or VantageScore is above the U.S. average credit score of 716. It beats over half of consumers.

-

You should still qualify for most credit cards, loans, mortgages, apartments etc. Many lenders view 660 as an acceptable score.

-

Your interest rates may be reasonable – not the rock bottom rates of 700+ scores, but also not the sky-high subprime rates below 600.

-

You’re less likely to have a credit application denied compared to consumers with poor credit scores below 580.

On the negative side:

-

Many lenders do consider 660 fair rather than good credit. You may not get ideal rates or terms.

-

Approval for premium credit cards with the best rewards and offers will be challenging until you reach the good credit band.

-

Your credit limit on new credit cards may be lower than those with higher scores. This limits how much you can spend while keeping your utilization low.

-

You may need a larger down payment for a mortgage, auto loan, or other financing compared to buyers with 700+ credit.

Overall, while a 660 credit score certainly isn’t bad, it’s generally not regarded as good either. You can likely qualify for anything you need, but often not with the most favorable conditions.

How a 660 Credit Score Impacts Your Credit Applications

As a borderline fair/good score, a 660 credit score will impact your credit applications in a few key ways:

Credit Cards

-

You should qualify for unsecured cards, but likely won’t get premium travel and cashback rewards cards. Expect credit limits under $5,000.

-

Interest rates may be 15% – 25%. Average rates for good credit are 10% – 20%.

-

You’ll probably need to pay an annual fee for your card, unlike consumers with 700+ scores.

Auto Loans

-

You can likely get approved but should expect APRs in the 5% – 10% range, compared to 3% – 6% for buyers with good credit.

-

Your loan term may be shorter (48-60 months). Better rates come with longer 72-84 month terms.

-

You’ll probably need a 10% – 20% down payment. Those with 700+ scores often put 0% – 10% down.

Mortgages

-

660 meets most banks’ minimum score requirement for conventional mortgages. But your interest rate will be higher than buyers with 700+ credit.

-

You may need to look at FHA, USDA, or VA loans, which allow lower down payments but cost more long-term.

-

Your down payment may need to be 10% – 20%. Excellent scores often qualify for 3% – 5% down payments.

Apartment Rentals

-

A 660 credit score meets most basic apartment rental requirements. But luxury buildings may reject scores under 700.

-

You’ll likely have to pay a higher security deposit equal to 2+ month’s rent. Excellent scores often pay just 1 month.

-

If you have no rental history, you may need a cosigner with better credit to qualify.

The exact terms you qualify for will vary based on your entire credit profile. But in general, a 660 score puts you in a middle ground where you can get approved for credit and loans but won’t get the cream of the crop offers.

Tips for Improving Your 660 Credit Score

Since a 660 credit score is on the edge between fair and good, it’s a great starting point for taking your credit to the next level. Here are some tips to improve your 660 score:

-

Lower credit card balances – High balances hurt scores more than anything. Get balances below 30% of limits.

-

Pay all bills on time – Set up autopay and reminders to avoid late payments. Payment history is #1 factor in scores.

-

Check for errors on your credit reports – Mistakes like incorrect late payments can unfairly tank your scores. Dispute errors with the credit bureaus.

-

Avoid new credit card applications temporarily – Too many hard inquiries from applying for multiple cards will ding your scores temporarily. Let your reports cool off.

-

Monitor your credit with a free service – Use Credit Karma or a similar free platform to monitor your credit reports and scores. This helps you catch issues before they snowball.

-

Consider becoming an authorized user – Ask a family member with excellent credit to add you as an authorized user on a longstanding card. Their good history can boost your scores.

-

Build credit mix – Open an installment loan (mortgage, student, auto, personal) if you only have credit cards now. Variety boosts scores.

With consistent good credit habits, there’s no reason your score can’t reach the 700+ range in 6-12 months. Aim high!

The Bottom Line

A 660 credit score is right on the borderline between being considered fair vs. good. While far from terrible, it makes getting the very best rates and terms difficult.

The major advantage of a 660 score is that you should still qualify for any credit cards, loans, or other financing you need – though likely not with the rock bottom interest rates and lenient terms reserved for 700+ credit.

With dedicated effort through good financial habits, a 660 score can often be improved to good within less than a year.

Rather than getting discouraged by the limitations of a 660 score, focus on the many positive credit behaviors it takes to reach even that middle level. With diligence and patience, you can turn that fair credit into good – or even excellent.

What Is a Good VantageScore Credit Score?

The latest VantageScore 3. 0 and 4. 0 credit scores use a range of 300 to 850âthe same as the base FICO® Scoresâand a good score is 661 to 780.

VantageScore doesnt have industry-specific credit scores, but it has released updated models over the years. The first two VantageScore credit scores had a 501 to 990 range, but lenders dont commonly use those scores.

Why Having a Good Credit Score Is Important

Having good credit can make achieving your goals easier. It could be the difference between qualifying or being denied for an important loan, such as a home mortgage or car loan. It can also directly impact how much youll have to pay in interest or fees if youre approved.

For example, the difference between taking out a 30-year, fixed-rate $350,000 mortgage with a 620 FICO® Score and a 700 FICO® Score could be $138. 58 a month. Thats extra money you could be putting toward your savings or other financial goals. Over the lifetime of the loan, having the better score would save you $49,889 in interest payments.

Additionally, credit scores can impact non-lending decisions, such as whether a landlord will agree to rent you an apartment.

Your credit reports can also impact you in other ways. Some employers may review your credit reports (but not your credit scores) before making a hiring or promotion decision. In most states, insurance companies may use credit-based insurance scores to help determine your premiums for auto, home and life insurance.

| FICO® Score | Interest Rate, 30-Year Fixed-Rate Mortgage | Monthly Payment | Total Interest Cost |

|---|---|---|---|

| 620 | 7.71% | $2,806.11 | $549,199 |

| 700 | 7.13% | $2,667.53 | $499,310 |

| 840 | 6.69% | $2,564.49 | $462,214 |

Source: Curinos LLC, December 6, 2024; assumes a $350,000 mortgage and 30-day rate-lock period

Learn more: Facts About Credit You May Not Know

How Good Are Credit Scores Between 660-669?

FAQ

What does a 660 credit score mean?

Credit Karma strives to provide a wide array of offers for our members, but our offers do not represent all financial services, companies or products. A 660 credit score is generally a fair score.

Is a 580-669 credit score good or bad?

Credit scores within the 580-669 range are considered to be fair credit. With a 660 credit score, lenders will generally consider you to be a higher-risk borrower. In spite of the fact that your credit score is below average, it’s not “bad credit” and shouldn’t stop you from getting some types of loans.

What is the best credit card for a 660 credit score?

The best type of credit card for a 660 credit score is a card with low fees and either rewards or a low APR promotion. You should compare credit cards with rewards if you plan to use your card for everyday purchases that you can pay off by the end of the month.

Can I get a loan with a credit score of 660?

If your credit score is 660 or lower, you can still get a loan, but it might be harder to get and cost more. Your credit score is a key factor that lenders consider when assessing your creditworthiness.

Can I apply for a credit card with a 660 credit score?

You may be able to get credit cards with a score of 660, but the terms and interest rates will likely not be the best. Most of the best unsecured credit cards to apply for with a 660 credit score are secured cards.

Is a 660 credit score a dead end?

A 660 credit score is not a dead end, although it can limit your access to some credit products and you may face higher interest rates compared to those with higher scores. Nonetheless, a ‘Fair’ credit score is not a dead end.

What will a 660 credit score get me?

With a 660 credit score, you can still get approved for several types of loans and credit cards. Keep in mind that your options may come with higher annual percentage rates (APRs) than if you had a higher credit score (though other factors also apply).

How to increase credit score from 660 to 700?

Is 700 a good credit score?

For a score with a range of 300 to 850, a credit score of 670 to 739 is considered good. Credit scores of 740 and above are very good while 800 and higher are excellent. For credit scores that range from 300 to 850, a credit score in the mid to high 600s or above is generally considered good.

How common is a 600 credit score?