With most credit scores, any damage from a high credit card utilization goes away when credit bureaus have up-to-date information on your new, lower balances.

When you report a new, lower balance to the credit bureaus, a high credit card balance usually stops hurting your credit score. The main way to reduce your credit card utilization is to pay down your balances. Once you do that, your score might recover within a couple months, all other things being equal.

Having a credit utilization ratio of 80% or higher can definitely hurt your credit score But how bad is it really? And how long does the damage last? Let’s take a closer look at why high utilization matters and what you can do to improve it.

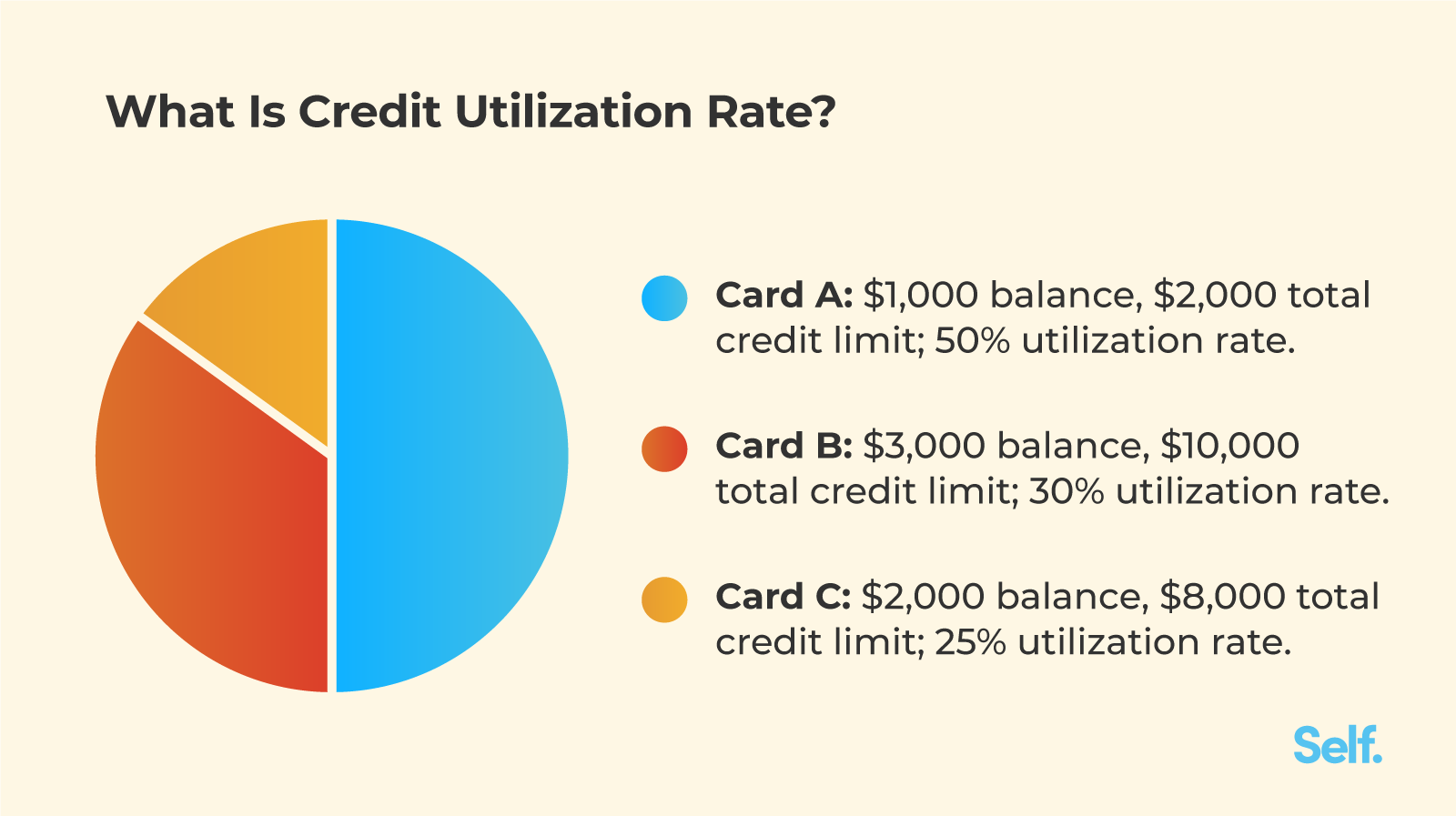

What is Credit Utilization and How is it Calculated?

When you use credit, it means how much of your available credit you are using at any given time. To get it, divide your credit card balances by your credit limits.

For example if you have a total credit limit of $10000 across all your cards and your current balances add up to $8,000, your credit utilization is 80% ($8,000/$10,000).

This ratio is calculated for each card individually and also for all your cards together. The latter is known as your total revolving utilization.

Why Does Credit Utilization Matter?

About 30% of your FICO credit score is based on how well you use your credit. High utilization is seen as a sign of credit risk by the scoring model because it means you depend too much on credit cards.

FICO actually looks at two main factors:

- Your utilization on each card

- Your total revolving utilization

Scoring models punish you more if you have any cards that are heavily used. But your total ratio matters as well.

How High is Too High?

Experts often recommend keeping utilization below 30%. Once you exceed that threshold, your score could start taking a hit. The higher your utilization, the worse the impact.

Here’s a rough guide to various utilization levels:

- 0-9% – Excellent

- 10-29% – Good

- 30-49% – Fair

- 50-74% – Poor

- 75-89% – Very Poor

- 90-100% – Extremely Poor

A utilization of 80% would fall in the “very poor” range. Not only will this hurt your score, but it may make lenders view you as a risky borrower.

The Severity of Impact Depends on Other Factors

Keep in mind your credit history plays a role too. Someone with a long credit history, low balances, and lots of available credit will likely see a smaller score drop than someone with a shorter history and 80% utilization.

For instance, if you have a $2,000 limit card and only use $1,600 of it, your utilization rate is 80%. If you only have that one card, though, it makes a bigger difference than if you have five other cards with low balances and lots of credit available.

How Long Does the Damage Last?

The good news is high utilization only hurts your score while it remains high. As soon as you pay down balances, your score should start to improve.

Most credit scoring models look at your most recent balances when calculating utilization. So if you reduce balances before your next statement cuts, your score could bounce back within a billing cycle or two.

The one exception is VantageScore 4.0, which looks at utilization trends over the past 24 months. But most lenders rely on FICO scores, which emphasize your current utilization.

5 Tips to Reduce Your Credit Utilization

If you have high balances, here are some strategies to reduce utilization and limit damage to your credit:

- Make an extra payment mid-cycle to lower your balance faster

- Ask for a credit limit increase to boost your total available credit

- Pay down balances aggressively and pay in full each month

- Use your highest limit cards for big purchases to avoid maxing out cards

- Open a new card if you need more available credit

The most important thing is to pay down existing balances. But a credit limit increase can also provide immediate relief by lowering your ratio.

The Takeaway: Keep Utilization Low Whenever Possible

Having a credit utilization ratio of 80% or higher is generally considered very risky. The higher your utilization, the more it can negatively impact your credit scores.

Aim to keep individual cards and total utilization below 30% whenever possible. Pay off balances monthly or make extra payments during the month.

The good news is that as soon as you reduce your balances, your credit score should start to recover fairly quickly. So focus on lowering your utilization now to minimize long term damage.

How Credit Utilization Rate Affects Credit Scores

Credit card utilization is the portion of your credit card limit that is in use. Credit utilization is an important factor in calculating “amounts owed,” which makes up about 30% of your FICO® ScoreÎ. FICO® Scores are used by 90% of top lenders, so its an important consideration.

You can calculate your credit card utilization by dividing your cards balance by its credit limit. Similarly, overall credit utilization is the sum of your total credit card debt across all cards divided by the sum of your credit card limits and multiplied by 100.

Heres an example of how this could work.

Lets say you have a retail credit card with a credit limit of $300, and you charge $150 worth of merchandise. You now have a credit card utilization rate of 50%âwell above the recommended 30% ceilingâfor that particular credit card.

Now lets say you have a second credit card that you mainly use to buy coffee. It has a credit limit of $5,000 and the typical monthly balance is also about $150. The utilization on that card is just 3% ($150 divided by $5,000, multiplied by 100).

If you only have these two cards, overall utilization would be slightly less than 6% ($300 divided by $5,300, multiplied by 100). Thats an excellent overall credit utilization rate.

How Long Does High Credit Card Utilization Impact Your Credit Score?

For most credit scoring models, a high credit card utilization can impact your credit score as long as your balances remain high. If you pay down your balance and your card issuer reports the lower credit card utilization to the credit bureaus, you could see a positive effect on your scores in as little as 30 days.

Credit scores are sensitive to your credit utilization ratioâthe amount of credit youre using relative to your total credit limits. The lower your utilization, the better for your credit score.

However, some newer scores, namely VantageScore® 4.0 4.0 and FICO® 10 T Score, use something called trended data. Those credit scores include utilization data from up to 24 months ago. You can think of traditional credit scores as a snapshot and scores using trended data as a video. As the name implies, they look at the trend over time. Are your balances overall growing or shrinking? They arent yet used for mortgages, but they will be in the future. The use of trended data means that paying off credit card debt all at once, whether through a loan or a windfall, is unlikely to keep a history of high balances from affecting your credit score.

Most credit experts suggest keeping credit utilization under 30%. That means if you have a credit card with a $3,000 limit, you should keep the balance under $900 to avoid doing more serious damage to your credit score. If your credit utilization changes significantly, the impact to traditional scores can be large.

Is 0% Utilization Bad For Your Credit Score?

FAQ

Is 80% credit usage bad?

The lower your credit utilisation ratio the better. But generally, it’s best to keep your credit utilisation ratio at 30% or below.

Can I use 80% of my credit limit?

Yes, high credit utilisation is bad for your credit score. In general, it is advised to keep the utilisation under 30% of the overall credit limit. However, if it’s not possible to keep it below 20%, it’s recommended to do so at all costs.

Does 0% utilization hurt credit?

Yep, having 0% utilization can sometimes cause a small score drop because credit scoring models like to see some activity. It’s weird, but they prefer you to use credit rather than have a $0 balance reported.

Is it bad to use 75% of your credit limit?

If you spend over 50%, it could negatively impact your credit score. And if you use over 75% of your limit, it’s quite likely this will have a negative impact.