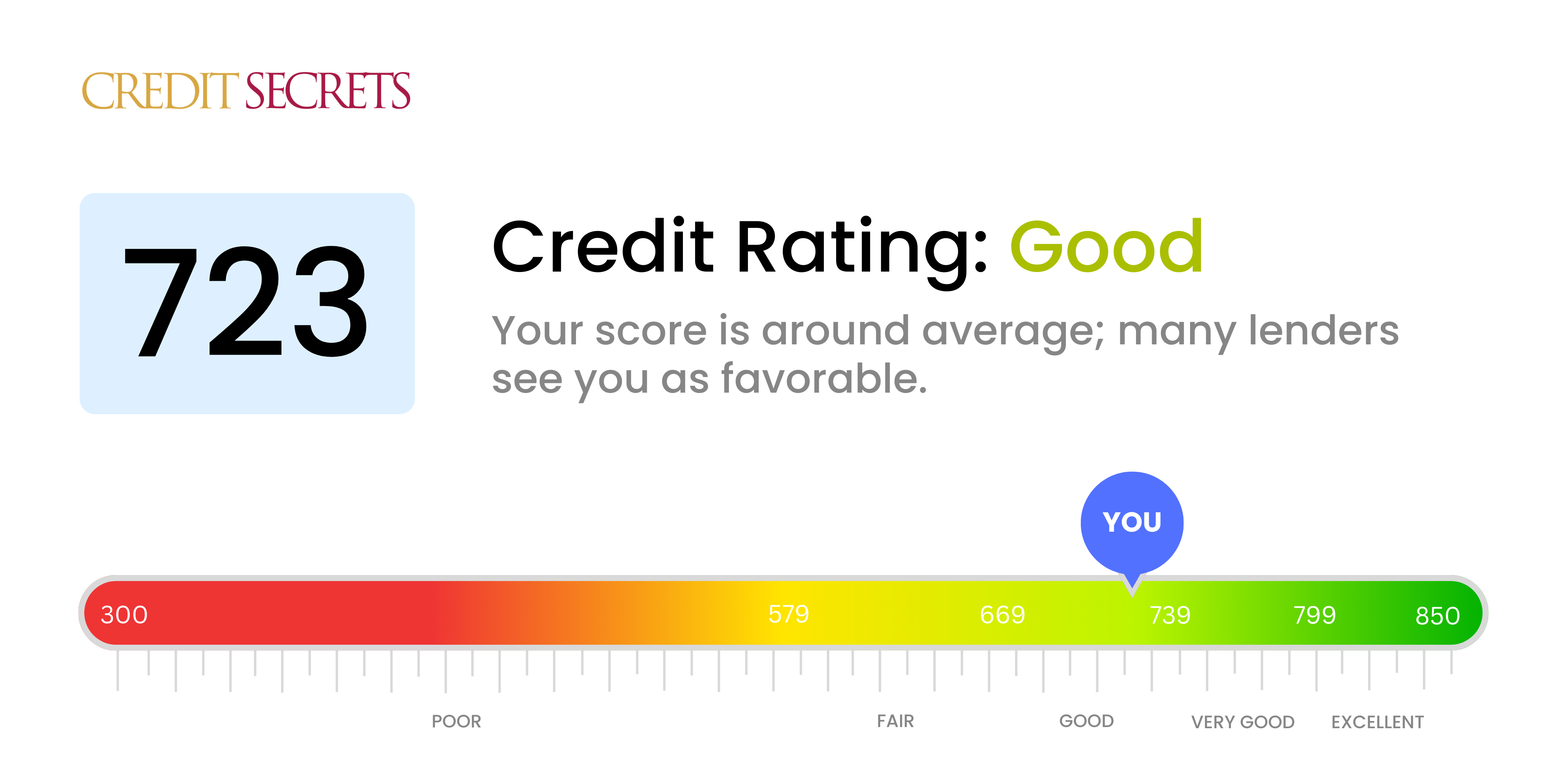

For a score with a range of 300 to 850, a credit score of 670 to 739 is considered good. Credit scores of 740 and above are very good while 800 and higher are excellent.

For credit scores that range from 300 to 850, a credit score in the mid to high 600s or above is generally considered good. A score in the high 700s or 800s is considered excellent. About a third of consumers have FICO® ScoresÎ that fall between 600 and 750âand an additional 48% have a higher score. In 2023, the average FICO® Score in the U. S. was 715.

Lenders use their own criteria for deciding whom to lend to and at what rates. But if your credit score is higher, you may be able to get a credit card or loan with better terms and a lower interest rate. The most common credit scores are the FICO® Score and the VantageScore® Credit Score. Their ranges are a little different, but their scoring factors are the same.

If you want to get loans and credit cards with low interest rates, you need to have a good credit score. But what exactly is a “good” credit score? For example, do lenders think that a score of 723 is good?

The short answer is yes, a credit score of 723 is generally considered good This article will explain what credit scores mean, the benefits of having a score of 723, and tips for maintaining or improving your credit

What is a Credit Score?

Your credit score is a number calculated based on information in your credit report, which shows your history of borrowing money and repaying debts. The most commonly used credit scoring model is the FICO score, which ranges from 300 to 850.

Higher scores indicate lower credit risk to lenders. People with higher credit scores are seen as more likely to make their payments on time and less likely to default on loans. As a result, they can qualify for better interest rates from lenders.

Credit scores are classified into ranges

- 800-850: Exceptional

- 740-799: Very Good

- 670-739: Good

- 580-669: Fair

- Under 580: Poor

So where does a 723 credit score fall? Right in the middle of the “good” range.

Why is a 723 Credit Score Considered Good?

Scores in the lower 700s, like 723, are good because they show lenders that you can handle your credit well. Even though it’s not high enough to get the best rates, a 723 score tells lenders that you are a pretty safe borrower.

Specifically, people with scores around 723 typically have:

- A moderate length of credit history

- Mostly on-time payments, with perhaps some minor delinquencies

- Manageable amounts of debt relative to available credit

This level of creditworthiness allows access to a wide variety of credit products, even if not at the most favorable terms reserved for exceptional credit.

Benefits of Having a 723 Credit Score

Most lenders will give you a loan if your credit score is at least 723. You can expect to see benefits such as:

- High approval odds for credit cards and loans

- Access to low interest rates

- Larger credit limits and borrowing amounts

- Less stringent underwriting requirements

Even though a score in the mid-700s is good, it’s not quite exceptional. This means you might not get the lowest interest rates or the highest credit limits there are. But your 723 score makes it possible for most lenders to offer you very low rates.

Credit Cards

A 723 FICO score gives you an excellent shot at approval for a variety of credit card offers. You can likely qualify for cards offering rewards like:

- Cash back

- Travel miles

- Retail store points

- 0% intro APR promos

Just don’t expect access to ultra-exclusive cards meant for consumers with exceptional scores above 800. You may also receive lower initial credit limits than people with higher scores.

Personal Loans

Your 723 credit score makes you a prime candidate for a personal loan at a competitive rate. Whether you need debt consolidation, home improvements, or major expenses, lenders will like your low-risk profile.

While interest rates vary by lender, applicants with scores in the low 700s typically see personal loan rates between 10-15%. Your solid credit score helps keep your rate toward the lower end of that range.

Auto Loans

723 is an excellent score for a car loan. You should have no problem getting approved for auto financing from a lender. Expect very competitive interest rates since your credit score indicates low risk.

For comparison, subprime borrowers with poor credit pay average auto loan interest rates over 20%. But with your 723 score, you should see much lower single-digit rates from most lenders.

Mortgages

A credit score of 723 or higher makes you eligible for conventional mortgage loans from private lenders. This includes popular loan types like conventional, FHA, and VA loans.

While mortgage lenders look at multiple factors, your 723 score gives you a major advantage in getting approved. You may not receive the rock-bottom mortgage rates reserved for exceptional borrowers above 760. But you should still qualify for highly competitive interest rates.

Tips for Maintaining a 723 Credit Score

Now that you know the benefits of having a 723 credit score, here are some tips for keeping it in good standing:

-

Pay all bills on time. Payment history is the most important factor in your score. Set up autopay or reminders to avoid late payments.

-

Keep credit utilization low. Try to keep balances below 30% of your credit limits on each card.

-

Monitor credit reports. Check reports regularly for errors or suspicious activity. Dispute any inaccuracies with the credit bureaus.

-

Limit new credit applications. Too many hard inquiries from applying for new credit can ding your score temporarily. Apply conservatively.

-

Build diverse credit history. Having a mix of installment loans and revolving accounts looks best for your score.

How to Improve Your 723 Credit Score

While a 723 credit score is good, you can potentially improve it further with time and good financial habits. Here are some tips:

- Pay down balances to decrease credit utilization

- Become an authorized user on a spouse or family member’s old account

- Dispute any inaccuracies dragging down your score

- Let time pass and build a longer credit history

With prudent money management, you could see your 723 score start creeping higher into the “very good” territory. Monitoring your score regularly lets you track your progress.

The Takeaway

A FICO credit score of 723 falls squarely in the “good” range between 670-739. This level of creditworthiness makes you eligible for approval from a wide variety of lenders at competitive rates, though not necessarily the lowest rates reserved for exceptional credit. Scores in the low 700s strike a balance showing responsible borrowing behavior with some potential room for improvement. By maintaining healthy credit habits, you can preserve a good 723 score over time or potentially bump it higher.

What Information Credit Scores Do Not Consider

FICO and VantageScore do not consider the following information when calculating credit scores:

- Where you live: Including your current and previous addresses.

- Demographics and beliefs: Your age, race, color, religion, national origin, sex, sexual orientation, gender identity and marital status. The Equal Credit Opportunity Act prohibits creditors from considering this information, or using credit scores that consider this information, when making lending decisions.

- Income and employment: Your salary, occupation, title, employer, date employed or employment history. However, lenders may consider this information when making decisions.

- Soft inquiries: A record of when someone checks your credit for a non-lending purpose. Soft inquiries are often the result of companies reviewing existing customers credit reports, creating marketing lists or responding to preapproval requests. They can also occur when you check your own credit report or when you use credit monitoring services from companies like Experian.

What to Do if You Don’t Have a Credit Score

Credit scoring models cant score credit reports that dont have enough information.

For FICO® Scores, you need:

- An account thats at least six months old

- An account that has been active in the past six months

VantageScore can score your credit report if it has at least one active account, even if the account is only a month old.

If you arent scoreable, you can:

- Sign up for Experian Goâ¢. Experian Go helps you jump-start your credit by creating an Experian credit report for you even if you dont have any credit accounts yet. It then provides you with personalized insights on how to move forward with building credit.

- Use Experian Boost®ø. Once you have an Experian credit report, you can use Experian Boost to get credit for certain qualifying bills, such as utility bills, streaming subscriptions, insurance and eligible rent payments. These payments can be added to your credit history and instantly increase your FICO® Score.

- Become an authorized user. When someone adds you as an authorized user on one of their credit cards, the accounts details and history might be added to your credit report. It can help you establish your credit, although the account could also help or hurt your score depending on how the primary cardholder manages the card.

- Open new credit accounts. It can be difficult to qualify for new credit accounts when you dont already have a credit score. But there may be some low- and no-fee options, such as credit-builder loans, lending circles and secured credit cards that dont have an annual fee.

Learn more: Ways to Build Credit if You Have No Credit History

Is A 723 Credit Score Good? – CreditGuide360.com

FAQ

Is a 723 credit score a good credit score?

The first thing you need to do to improve your credit is to learn how to read and understand your credit reports and scores. A 723 credit score is considered a good credit score by many lenders. Here’s what it means to have good credit and how you can maintain your score.

Can a 723 credit score qualify for a car loan?

Absolutely. Your 723 credit score will qualify you for an auto loan, assuming your income justifies it. That being said, it’s important to know that the interest rate you get can depend on your credit score. And this is especially true in auto lending.

What is a good credit score for a mortgage?

For conforming mortgages (conventional loans that meet Fannie Mae or Freddie Mac standards), you need a score of 620. For FHA mortgages with low down payments, you need a score of 580. Your score puts you comfortably over both thresholds. Having said that, there are a few things to keep in mind.

What can I get with a 723 credit score?

With a 723 score, you should easily be able to access personal loans, car loans, and mortgage loans, as well as rewards credit cards. That said, you’re still below the top two FICO tiers — “very good” and “exceptional.”

What loan can I get with a 723 credit score?

A credit score of 723 is considered excellent and is indicative of a responsible borrower who manages credit and debt well. If you have a credit score of 723 or higher, you are likely to have access to a wide range of financial products and services, including personal loans with favorable terms and conditions.

What is an extremely good credit score?

- 800 to 850: Excellent Credit Score. Individuals in this range are considered to be low-risk borrowers. …

- 740 to 799: Very Good Credit Score. …

- 670 to 739: Good Credit Score. …

- 580 to 669: Fair Credit Score. …

- 300 to 579: Poor Credit Score.

How rare is a 700 credit score?