Hey there, friend! Have you ever thought about what would happen if you put an extra $300 a month toward your mortgage? Oh, boy, it would make a huge difference. You’ll pay off your loan much faster, save a lot of money on interest, and own your home outright a lot sooner than you thought. We did the math and have the lowdown for you here in our little corner of financial wisdom. So get a coffee and let’s talk about how this extra money can change your mortgage journey.

The Big Deal: Why Extra Payments Matter

First off let’s get why paying more on your mortgage is such a big freakin’ deal. When you got a home loan—say, a 30-year mortgage—most of your early payments go straight to interest not the actual debt. It’s like renting money from the bank, and it sucks. But when you toss in an extra $300 each month, that cash usually hits the principal (the real loan amount) directly. Less principal means less interest piling up over time. Boom! You’re cutting down both the cost and the length of your loan.

Here’s the quick and dirty

- Lower Interest Costs: Since interest is calculated on the remaining balance, shrinking that balance early saves you big bucks.

- Shorter Loan Term: Extra payments speed up how fast you pay off the whole dang thing.

- Financial Freedom: No mortgage payment? That’s more cash for vacations, investments, or just chillin’ without stress.

Now, let’s put some real numbers to this and see what $300 extra a month can actually do for ya.

Crunching the Numbers: A Real Example with $300 Extra

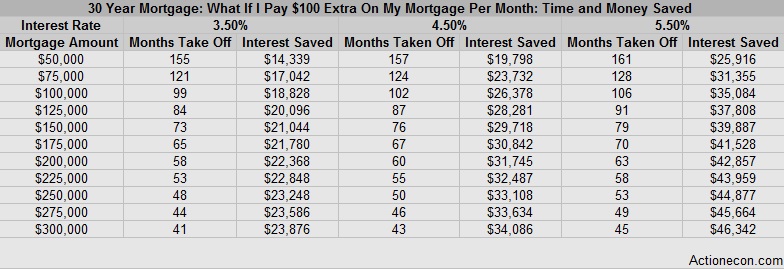

Picture this: you owe $300,000 on a 30-year loan with a 4% interest rate. 125% interest rate. About $1,454 is your monthly payment for the loan’s principal and interest. You’d have to pay a huge $523,440 over 30 years, with a big chunk of that going to interest. Dang, that’s a lotta money just for borrowing!.

First, let’s say you pay an extra $300 a month right away. This would make your new payment $1,754. What happens? Hold onto your hat, ‘cause it’s wild:

- Time Saved: You’d pay off your loan in just over 23 years instead of 30. That’s almost 7 years chopped off!

- Money Saved: You’d save around $60,000 in interest over the life of the loan. Sixty grand! That’s a car, a fancy vacay, or a nice nest egg.

Wanna see it broken down? Check this lil’ table I whipped up:

| Scenario | Monthly Payment | Total Paid | Loan Term | Interest Saved |

|---|---|---|---|---|

| Standard Payment | $1,454 | $523,440 | 30 years | $0 |

| With Extra $300/Month | $1,754 | $463,000 (approx) | 23.3 years | ~$60,000 |

Do you see that? A little more each month isn’t just a drop in the bucket—it’s a waterfall of money saved! Another thing that might sound like a lot of money is $300. But if you skip a few takeouts and cut back on subscription junk, you might find that money in your budget.

How Does This Magic Work?

Alright let’s break it down real simple. When you pay extra on your mortgage that money don’t just sit there lookin’ pretty—it goes straight to the principal balance. Early in your loan, most of your payment covers interest, and only a tiny bit chips away at what you owe. By adding $300 to the mix, you’re attacking the principal faster, which means less interest gets tacked on each month.

Think of it like this: Imagine you owe a buddy $100, and he’s charging ya 5% interest a month. If you only pay $5, most of it covers the interest, and you barely dent the debt. But if you pay $10, more goes to the actual $100, and next month’s interest is smaller. Same deal with a mortgage, just on a way bigger scale.

The earlier you start paying extra, the better. Why? ‘Cause interest compounds over time, and slashing the principal early stops that snowball from getting outta control. If you wait 10 years to start paying extra, you’ve already paid a ton of interest, and the savings won’t be as juicy.

What If My Mortgage Ain’t $300,000?

No worries, fam! The beauty of extra payments is they work no matter your loan size or interest rate—tho’ the exact savings and time cut will vary. Let’s peek at a couple other scenarios so you get the full picture.

- Smaller Loan Example: Say you’ve got a $200,000 mortgage at 5% for 30 years. Your standard payment is around $1,073. Add $300 extra each month, and you’re paying $1,373. You could knock off about 8 years and save close to $45,000 in interest. Not too shabby!

- Bigger Loan Example: Got a $400,000 loan at 3.5% for 30 years? Standard payment is about $1,796. Toss in $300 extra (total $2,096), and you might cut off 5-6 years and save over $50,000 in interest.

The point? That extra $300 packs a punch, whether your mortgage is big or small. The higher the interest rate, the more you save by paying early, ‘cause you’re dodging those pricey interest charges.

Pros of Paying an Extra $300 a Month

Now that we’ve seen the numbers, let’s chat about why paying extra is often a sweet move. Here’s the good stuff:

- Save a Boatload on Interest: As we’ve seen, you can save tens of thousands over the life of your loan. That’s real money back in your pocket.

- Own Your Home Sooner: Cutting years off your mortgage means you’re debt-free way quicker. Imagine no house payment in your 40s or 50s instead of your 60s!

- More Cash Flow Later: Once the mortgage is gone, that monthly payment can go to savings, fun, or whatever you fancy.

- Peace of Mind: Ain’t nothing like knowing your home is 100% yours, no bank breathing down your neck.

For many of us, paying extra feels like taking control of our financial future. It’s empowering, y’know?

Cons and Stuff to Watch Out For

But hold up—paying an extra $300 a month ain’t always the perfect plan for everyone. There’s some pitfalls to keep an eye on, and I wanna be real with ya:

- Prepayment Penalties: Some lenders ain’t thrilled when you pay off early, and they might slap ya with a fee. It’s rare these days, and usually capped at like 2% in the first couple years, but check with your bank first. Don’t get caught off guard!

- Credit Score Weirdness: Paying off a mortgage early can sometimes ding your credit a lil’ bit, ‘cause it closes out a long-term account. It’s usually temporary, but if credit’s a big deal for ya, keep that in mind.

- Liquidity Issues: If you’re pouring every spare dime into your mortgage, you might be strapped for cash if an emergency hits. Homes ain’t liquid—you can’t sell ‘em overnight for quick money. Make sure you’ve got an emergency fund before overpaying.

- Other Debts Matter More: Got credit card debt at 15% interest? Heck, pay that off before throwing extra at a 4% mortgage. High-interest debt eats your wallet way faster.

So yeah, while $300 extra can be awesome, weigh your whole money situation first. Don’t just jump in blind.

Alternatives to Paying $300 Monthly

Maybe $300 a month feels like a stretch, or you wanna mix things up. No prob! There’s other ways to tackle your mortgage faster:

- Bi-Weekly Payments: Instead of paying once a month, pay half your payment every two weeks. Since there’s 26 bi-weekly periods in a year, you end up making an extra full payment annually. It’s like sneaking in extra without feeling the pinch.

- Lump Sum Payments: Got a bonus, tax refund, or some birthday cash? Throw a one-time chunk at your principal. It won’t change your monthly bill, but it cuts down the loan term and interest.

- Round Up Your Payment: If $300 is too much, just round up to the nearest $50 or $100. Even $20 extra a month adds up over time.

These options give ya flexibility. You don’t gotta commit to $300 every single month if life throws a curveball.

Tips to Make Paying Extra Work for Ya

If you’re hyped to start paying an extra $300—or whatever you can swing—here’s some practical tips from us to keep things smooth:

- Check with Your Lender: Make sure they apply extra payments to the principal, not future interest. And double-check for any penalty nonsense.

- Set Up Auto-Payments: Automate that extra $300 so you don’t forget or spend it on somethin’ dumb like another streaming service.

- Start Small If Needed: Can’t do $300? Start with $50 or $100 and ramp up when you get a raise or cut expenses.

- Keep an Emergency Fund: Stash at least 3-6 months of living costs in savings before overpaying. Don’t leave yourself high and dry.

- Reassess Yearly: Life changes, man. Check your budget and goals each year to see if $300 still makes sense.

We’ve seen folks turn their mortgage game around with these lil’ tweaks. It’s all about finding what fits your vibe.

What If I Can’t Do $300 Every Month?

Hey, no sweat if $300 ain’t doable right now. Life’s expensive, and we get it. The cool thing is, even smaller amounts make a dent. Paying an extra $50 or $100 still cuts interest and time, just at a slower pace. For instance, on that $300,000 loan at 4.125%, just $100 extra a month could save ya over $20,000 in interest and cut off a couple years. Not bad for a little effort!

Or, if you’re flush one month but tight the next, do what you can when you can. Every bit helps. And like I mentioned earlier, a lump sum here and there works wonders too. Maybe use a holiday bonus or side hustle cash to knock down the principal once a year.

Does the Timing of Extra Payments Matter?

Heck yeah, it does! The sooner you start paying extra, the more you save. Why? Early in your mortgage, interest is the biggest part of your payment. If you wait 10 or 15 years to pay extra, you’ve already shelled out a ton on interest, and the savings ain’t as sweet. Start year one, and that $300 slashes interest from the jump.

But even if you’re midway through your loan, don’t think it’s too late. Paying extra still helps—it just won’t save as much as starting early. So don’t wait for the “perfect” moment. Start now, even if it’s been a few years.

Should I Pay Extra or Invest Instead?

This is a biggie question I hear all the time. Paying an extra $300 on your mortgage is awesome, but sometimes investing that cash might get ya a better return. If your mortgage rate is super low—like 3%—and you can invest in somethin’ with a higher return, like stocks averaging 7-8%, you might come out ahead by investing.

But here’s the rub: Investments got risk. Markets crash, and you could lose dough. Paying off your mortgage is a guaranteed “return” equal to your interest rate, with zero risk. Plus, there’s the emotional win of being debt-free. So, it’s a personal call. If you’re risk-averse or just wanna own your home ASAP, pay extra. If you’ve got an emergency fund and love playing the market, maybe invest. Or split the difference—pay $150 extra and invest $150.

How Do I Know If My Lender Allows Extra Payments?

Most lenders are cool with extra payments nowadays, but ya gotta confirm. Call ‘em up or check your loan docs. Ask:

- Do extra payments go to principal automatically?

- Are there fees for paying early, especially in the first few years?

- Can I set up bi-weekly payments or lump sums easily?

If your lender’s a pain about it, don’t stress too much. You might still pay extra, just watch for penalties. And if it’s a real bummer, look into refinancing with a lender who’s more chill about overpayments.

Wrapping It Up: Is $300 Extra Worth It?

So, what happens if you pay an extra $300 a month on your mortgage? In short, you save a boatload of cash—often tens of thousands in interest—and cut years off your loan term. You could be mortgage-free way sooner, giving ya financial freedom to live life on your terms. But it ain’t a one-size-fits-all deal. Check for penalties, weigh other debts, and make sure you’ve got cash stashed for emergencies.

At the end of the day, we think paying extra is a dope move for most folks, especially if you start early. It’s like investing in your future self. So dig into your budget, see if you can swing $300—or even $50—and take that step. Your wallet (and your stress levels) will thank ya down the road. Got questions or wanna chat more about your specific mortgage? Drop a comment below, and let’s keep this convo rollin’!

How many years does one extra mortgage payment take off?

When it comes to making an extra mortgage payment, the amount extra amount you pay is as flexible as your budget allows. You can make a full extra payment, or maybe it’s better for you to round up to the nearest hundred. No matter how much extra you pay each month, that amount can help shorten the life of your loan. Even making one extra mortgage payment each year on a 30-year mortgage could shorten the life of your loan by four to five years. Using the calculator above, you can input your loan specifics to learn how making an extra payment could affect your mortgage.

Do extra payments automatically go toward principle?

The original amount you borrowed for your mortgage is called the “principal” balance. The interest that accrues on your loan is determined by your loan’s interest rate. When you make an extra payment, the funds are first applied to the outstanding accrued interest. After that, the rest of the money will be applied to your principal balance. If your loan terms allow it, you may be able to say that you want your extra payment to go toward the principal balance. If you can do this, the extra money will be used to pay down the principal balance.

What Paying an Extra $1000/Month Does To Your Mortgage

FAQ

What happens if you make an extra payment on a mortgage?

When you make an extra payment or a payment that’s larger than the required payment, you can designate that the extra funds be applied to principal. Because interest is calculated against the principal balance, paying down the principal in less time on your mortgage reduces the interest you’ll pay. Even small additional principal payments can help.

How often do you pay extra on a mortgage?

Making mortgage payments every two weeks is one of the most common ways that people pay more on their loans. There is an extra mortgage payment every year because payments are made every two weeks instead of just twice a month. There are 26 bi-weekly periods in the year, but making only two payments a month would result in 24 payments.

How do you pay extra on a mortgage?

Bi-weekly payments are another popular way to pay extra on a mortgage. There are 12 months and 52 weeks in a year, so making 26 payments every two weeks is the same as making 13 payments every month. The 13th payment goes directly toward the loan’s principal.

How much interest is paid on a mortgage without extra payments?

Just look at the amount of interest paid each month after the extra mortgage payment is made versus the same home loan without extra payments below. As you can see, payment 14 above consists of $310.30 in interest, while it’s $326.96 for the mortgage without extra payments.

What happens if I pay more than my mortgage payment?

By paying more than your required monthly mortgage payment, you can put that extra money directly toward the principal amount on your loan. Your interest payment is based on your principal balance, so by applying your extra payment to your principal, you could pay less in interest over time. Click to call and get help from a loan expert.

What happens if a borrower makes an extra monthly payment?

If a borrower makes an extra annual payment, the savings on interest can be quite substantial. On a 30-year mortgage with the original principal total of $250,000 and an interest rate of 6.5 percent, the monthly payment is $1,580, including both principal and interest.

What happens if I pay an extra $300 a month on my mortgage?

How to pay off a 30-year mortgage in 15 years?

What happens if I pay $500 extra a month on my mortgage?

How many years does one extra payment take off a mortgage?