Extending credit to customers is a common practice for many businesses. However there is always a risk that some customers will be unable to repay their debts, leading to bad debts. Properly accounting for these potential losses is crucial for accurate financial reporting and tax compliance. In this article, we will explain the key differences between recognizing bad debt expenses and writing off uncollectible accounts.

Overview of Bad Debts

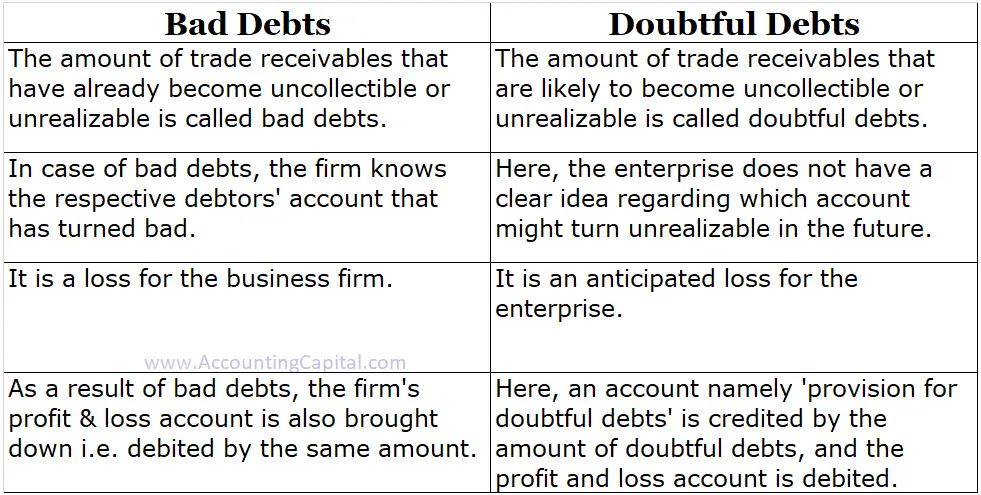

Bad debts, also known as uncollectible accounts receivable, are amounts owed to a company that have little or no chance of being paid. This happens when customers go bankrupt, face financial hardship, or simply refuse to pay.

There are two main methods for accounting for bad debts

- The direct write-off method

- The allowance method

When certain receivables are marked as uncollectible, the direct write-off method writes them off as bad debts. Rather, the allowance method guesses how much bad debt there will be ahead of time and keeps track of an expense every so often.

Bad Debt Expense

Recording a bad debt expense is a way of anticipating potential losses from customers not paying their debts in the future. This method adheres to the matching principle in accounting, which seeks to match expenses to the related revenue in the same reporting period.

Here are some key facts about bad debt expense:

- Recorded based on an estimate before an actual write-off occurs

- Reduces net income for the period on the income statement

- Uses previous experience or aging analysis to estimate uncollectible percentage

- Allows a company to be proactive in planning for bad debts

For instance, if a business thinks that 1% of their credit sales will not be able to be collected because of historical patterns, they would record a bad debt expense equal to 1% of their total credit sales for the period. This decreases net income on the income statement.

In order to “anticipate” future write-offs, the bad debt expense lets you know about the losses ahead of time.

Writing Off Bad Debts

In contrast to bad debt expense, writing off bad debts is the process of removing specific uncollectible accounts from the accounting records. This happens after collection efforts fail and management concludes that the amounts will not be received.

Some key characteristics of write-offs include:

- Occurs after the loss is confirmed, not before

- Directly reduces accounts receivable on the balance sheet

- Impacts allowance for doubtful accounts, not net income

- Based on actual uncollectible amounts, not estimates

For example, if a customer that owes $5,000 is declared bankrupt, the company would write off the $5,000 account, reducing accounts receivable and allowance for doubtful accounts. The write-off doesn’t affect the income statement.

Write-offs acknowledge a loss has happened, while bad debt expenses anticipate losses.

Key Differences Summarized

Here is a table summarizing the major differences between bad debt expense and the write-off of uncollectible accounts:

| Bad Debt Expense | Write-Off |

|---|---|

| Timing | Recorded before write-off occurs |

| Purpose | Anticipates future credit losses |

| Impact | Reduces net income on income statement |

| Based On | Estimate of uncollectible percentage |

Why Understanding the Distinction Matters

Maintaining sound accounting practices regarding bad debts is important for several reasons:

-

Accurate financial statements – Properly estimating and recording bad debt expenses and write-offs ensures receivables and revenues are not overstated.

-

Tax implications – Bad debt expenses are tax deductible in the year recognized for income tax purposes.

-

Credit risk management – Tracking bad debt expenses helps assess customer credit policies and make changes to minimize future losses.

-

Adherence to accounting principles – The process reflects the matching and revenue recognition principles.

Examples of Bad Debt Accounting

Let’s walk through some examples to illustrate the bad debt expense and write-off process.

Example 1

- ABC Company has credit sales of $100,000 in Year 1

- Based on past experience, they estimate 2% of receivables will be uncollectible

- ABC records a bad debt expense of 2% x $100,000 = $2,000

This reduces net income on the income statement by $2,000. It is anticipating future write-offs.

Example 2

- In Year 2, a customer that owes ABC $1,000 goes bankrupt

- ABC writes off the $1,000 account as uncollectible

- This directly reduces accounts receivable by $1,000 on the balance sheet

- No impact on the income statement

The write-off shows a real loss from a bad debt, while the bad debt expense from earlier showed losses that were expected and estimated.

Key Takeaways

-

Bad debt expense aims to recognize potential credit losses before they occur using estimates. Write-offs acknowledge actual losses from uncollectible amounts.

-

Bad debt expenses reduce net income on the income statement. Write-offs reduce accounts receivable on the balance sheet.

-

Prudent companies analyze historical trends and customer payment patterns to forecast bad debts and record timely expenses.

-

Maintaining sound bad debt accounting provides investors and stakeholders with transparency about credit risk and receivables management.

Properly differentiating between bad debt expense vs. write-offs requires a nuanced understanding of accounting methods and principles. But mastering this discipline can pay major dividends through improved financial reporting. Companies that excel at accounts receivable management will reap rewards of efficiency, transparency, and better decision-making.

Automate debt collection to reduce future write-offs

Manual collection processes often result in delays, missed follow-ups, and limited visibility into at-risk accounts. Using debt collection automation software can help your team focus on high-risk accounts, send reminders at the right time, and escalate accounts based on a set workflow. Automation not only improves recovery rates but also reduces the number of accounts that become uncollectible. With built-in analytics, you can look for patterns in late payments, guess how much bad debt there will be, and take steps to avoid having to write off debts in the first place.

Stop Chasing Payments: Tackle These Common Collection Excuses Head-On

Please fill in the details below

That is because any company that gives credit to customers knows that bad debt is a real risk. Despite best efforts and rigorous credit assessment processes, the risk of customers defaulting on payments looms large.

Whether you’re a seasoned business owner or just starting out, navigating the realm of bad debt write-offs requires a solid understanding of the process and its implications.

In this guide, you’ll learn about bad debt write-offs, including what they entail, how to write off bad debt, and much more.

- Introduction

- What is Bad Debt?

- What Is Bad Debt Write-Off?

- When Should Businesses Consider Writing Off Bad Debts?

- Why Is It Crucial to Write off Bad Debts?

- How to Write off Bad Debts

- What Are Some Alternatives to Writing off Bad Debt?

- Wrapping Up

Accounting for Bad Debts (Journal Entries) – Direct Write-off vs. Allowance

FAQ

What is the difference between write-offs and bad debt expenses?

The direct write-off method is used when a specific invoice is deemed uncollectible, and the bad debt expense is recognized immediately. Conversely, the allowance method involves establishing a bad debt reserve based on anticipated losses, which is then used to write off bad debts as they occur.

What is the difference between bad debts and bad debts written off?

The Bad Debt is the debt that can’t be paid back and can’t be gotten from the Debtor. The process is called writing off Bad Debt.

What is considered a bad debt expense?

Bad debt expense reflects the amount of accounts receivable that a company is unable to collect now and may not be able to collect in the future.

How long before bad debt is written off?

It generally takes seven years for settled debts to fall off your credit report. But, aside from paying off your debt, you can take other steps to rebuild and repair your credit even while old debts remain on your report, including: Making payments on time.