The FHA loan program, insured by the Federal Housing Administration, has long been a popular option for homebuyers, especially first-time buyers. But over the last decade or so, the percentage of buyers obtaining FHA financing has been on a downward trend.

The Declining Popularity of FHA Loans

At its peak in 2009, FHA loans accounted for 21.1% of all mortgage originations by loan count In the wake of the housing crisis and Great Recession, FHA lending surged as conventional mortgage credit tightened FHA loans, with their low down payment requirements and flexibility on credit scores, helped many buyers purchase homes when mortgages were hard to come by.

The share of FHA loans started to go down as the housing market got better, though. By 2022, FHA loans made up just 12. 57% of the mortgage market by loan count.

This declining market share can be attributed to a few key factors

-

The return of low down payment conventional loans – In 2014, Fannie Mae and Freddie Mac introduced 97% LTV conventional loan programs to compete directly with FHA. These loans offer similar benefits but with lower mortgage insurance costs.

-

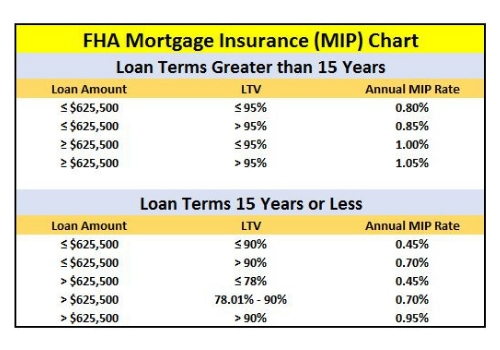

** Rising FHA mortgage insurance** – FHA mortgage insurance premiums have increased over time, making conventional loans with private mortgage insurance more affordable in comparison.

-

Tightened credit standards – After the crisis FHA tightened its underwriting, requiring higher credit scores and debt-to-income ratios. This disqualified many marginal buyers from obtaining FHA financing.

-

Better buyer finances—As the economy got better, buyers’ credit got better, their incomes went up, and they were able to make bigger down payments, which made it easier for more people to get conventional mortgages.

The Profile of the Typical FHA Buyer

FHA loans are good for buyers whose credit isn’t perfect and who might have trouble getting a conventional mortgage because they are easy to get.

The latest Home Mortgage Disclosure Act data from 2020 shows that the typical FHA borrower has:

-

A median household income of $72,000.

-

A median FICO score of 680.

-

A debt-to-income ratio of 43%.

-

84% were first-time buyers.

-

19% were minority buyers.

FHA borrowers have lower incomes, credit scores, and debt ratios compared to the overall market. They are also more likely to be first-time buyers and people of color. This means that a lot of families who might not have been able to before can become homeowners through FHA.

Recent Trends in FHA Lending

In the last few years, FHA lending has stabilized, hovering between 10-15% of the mortgage market. But looking closer, there are some interesting trends emerging:

FHA purchase lending rebounding – The FHA purchase share hit a low of 10.58% in Q1 2022 but was back up to 11.76% by Q1 2023. This aligns with rising rates pricing more buyers out of conventional loans.

FHA refis continue to decline – FHA refis were 15.92% of the market in Q4 2022 but fell to just 9.11% in Q1 2023. With interest rates high, few qualify for refinancing.

Conventional purchases growing – Conventional purchase lending hit a record 89.24% market share in Q1 2023 as government programs lost ground.

VA loans gaining share – VA loan usage rose from 10.69% in Q1 2022 to 13.40% in Q1 2023. Their zero down payment option gives VA an edge over FHA.

First-time buyers favor conventional – In January 2021, 59% of first-time buyers used conventional financing compared to just 24% using FHA. Conventional loans are now more competitive.

The Benefits and Drawbacks of FHA Loans

FHA loans come with unique advantages and disadvantages homebuyers should understand before choosing FHA or conventional financing:

Benefits

-

Low 3.5% down payment requirement

-

Down payment gifts allowed

-

Lower credit score requirements

-

More flexible debt-to-income ratios

-

Ability to finance closing costs into loan

Drawbacks

-

Upfront and lifetime mortgage insurance premiums

-

Limited loan amounts in high-cost areas

-

Required appraisal from FHA roster

-

Stricter occupancy and income requirements

-

More complex approval process and guidelines

The bottom line – FHA loans provide an affordable gateway to homeownership for underserved buyers. But conventional loans often offer lower costs and easier qualifications for those that can qualify.

The Outlook for FHA Lending in 2023 and Beyond

Looking ahead, here are some predictions for how FHA loan usage may evolve in coming years:

-

Purchase share will rise – As rates and prices rise, more conventional borrowers will be pushed to FHA, boosting its purchase activity.

-

Refinance share will stay depressed – Unless rates fall dramatically, fewer will refi and FHA refis will remain low.

-

First-time share will grow – With affordability worsening, first-timers will flock to FHA given the low down payment option.

-

VA competition intensifies – VA usage is surging and will likely keep eating into FHA purchase share thanks to zero down payments.

-

Conventional dominates – For buyers that can qualify, conventional loans will remain the product of choice given their lower costs.

-

FHA modernizes – Efforts are underway to streamline FHA lending through appraisal and manual underwriting changes.

While FHA may never regain its past peak levels, it will continue filling an important role in promoting sustainable homeownership. For buyers lacking resources, FHA provides an accessible path to achieving the dream of homeownership.

Report: 83% of FHA Loans Go to First-Time Buyers

During summer 2018, the Washington, D. C. -based Urban Institute published a study that analyzed key mortgage lending trends across the country. Among other things, this report offered some insight into FHA loans and who uses them.

Apparently, a lot of first-time home buyers in New Jersey use the FHA loan program to finance their purchases. Across our state and nationwide, roughly 83% of FHA mortgage originations are for first-time buyers. During the recession, usage among first-timers was at 75%. So it seems that more of these buyers are turning to FHA financing these days.

Definition: The Federal Housing Administration does not lend money directly to borrowers. Instead, it insures the loans made by banks and lenders in the private sector. This insurance gives lenders some protection against default-related losses. It also gives borrowers the benefit of a low down payment and flexible criteria.

Here’s a relevant quote from the August 2018 report:

As a result of offering low-down payment loans to people with bad credit, the Federal Housing Administration (FHA) has mainly focused on first-time homebuyers, who make up about 80% of all loans they originate. That share fell to around 75 percent during the recession but has slowly crept up to nearly 83 percent today. ”.

Small Down Payment, Flexible Requirements

This report clearly shows that many first-time home buyers in New Jersey prefer the FHA loan program as a financing option. And we’ve touched on some of the reasons for this already. This program offers borrowers a relatively low down payment, along with flexible qualification criteria.

- Down payment: As of now, FHA rules say that New Jersey home buyers who use this program can put down as little as 3. 5% of the purchase price or appraised value. Aside from the VA and USDA programs (which are only for certain borrowers), that’s one of the lowest minimum investments you can make these days.

- Eligibility: FHA loans aren’t just limited to first-time home buyers. This program is open to anyone who meets the minimum requirements. Compared to conventional or non-FHA mortgage loans, the minimum requirements for credit scores, debt ratios, and other things are not as strict.

These are the primary reasons why a lot of first-time buyers in New Jersey turn to this program. It allows for a relatively low upfront investment, and it offers flexible qualification criteria for borrowers.

NEW FHA Loan Requirements 2024 – First Time Home Buyer – FHA Loan 2024

FAQ

How much do I need to make to buy a $300K house with an FHA loan?

Some people need to make around $80,000 a year to buy a $300,000 house. This is based on the assumption that they will put down 30%. 5% interest rate, and moderate existing debts.

What is the FHA 85% rule?

The FHA 85% rule states that you can’t borrow more than 85% of your home’s value, and only applied to FHA cash-out refinance loans. However, the 85% rule no longer applies; the current LTV ratio limit for FHA cash-out refinances is 80%.

Why are sellers not accepting FHA loans?

Some sellers might not want to accept an FHA offer because they think FHA loans take longer to close or have stricter property requirements; having

What is the current FHA loan percentage?

| Product | Interest Rate | APR |

|---|---|---|

| 30-Year FHA Rate | 6.82% | 6.87% |

| 30-Year Fixed Rate | 6.83% | 6.90% |

| 15-Year Fixed Rate | 6.04% | 6.13% |

| 30-Year VA Rate | 6.86% | 6.91% |