Having incorrect or inaccurate information on your credit report can negatively impact your credit score and make it harder to get approved for loans, mortgages, credit cards, and other financial products. If you find errors on your credit report, you have the right under the Fair Credit Reporting Act (FCRA) to dispute them with the credit bureaus and have them corrected. But what exactly should you include in a credit dispute letter to improve your chances of success?

Why Accurate Credit Reports Matter

Your credit reports from the three main credit bureaus—Experian, Equifax, and TransUnion—show a lot of information about your credit history.

- Loan and credit card accounts

- Payment history

- Current balances

- Credit inquiries

- Public records like bankruptcies and judgments

Lenders rely heavily on credit reports and the credit scores derived from them when making decisions about whether to approve financing and at what terms. Inaccurate or incomplete information can unfairly drag down your credit score, costing you thousands in higher interest rates.

Getting mistakes fixed can help you get approved and save you money. So, dispute letters are a useful way to keep your credit in good shape.

Common Credit Report Errors to Watch For

While the credit bureaus have processes in place to ensure accuracy, mistakes do happen. Here are some of the most common errors to look for when reviewing your credit reports:

-

Accounts that don’t belong to you: This could be a sign of identity theft. If you see any accounts you don’t recognize, you should dispute them.

-

Account status that isn’t correct, like an open account that you know you closed or an account that still shows as having a balance even though you paid it off.

-

Late payments you made on time: Always check payment history and dispute any late payments that are reported in error.

-

Incorrect balances Make sure all balances match your records. Dispute any discrepancies.

-

Duplicate accounts: One legitimate account that gets counted twice can look much worse than it is.

-

Outdated personal information: Dispute any incorrect addresses, employers, or other personal data.

Staying on top of your credit reports allows you to find and dispute errors before they do too much damage.

What to Include in Your Credit Dispute Letter

Disputing errors on your credit report is usually as simple as writing a letter. Here are some tips on what information to include:

-

Your identifying information: Include your full name, date of birth, current address, phone number, and Social Security number so the credit bureau can confirm your identity.

-

Account information: Note the creditor name, account number, and type of account for each item you are disputing.

-

Reason for dispute: Explain concisely why you believe the information is inaccurate. For example, state that the late payment was made on time according to your records.

-

Supporting documentation: Include copies (not originals) of any evidence you have like bank statements, cashed checks, or communication with the creditor.

-

Desired resolution: Specify whether you want the item deleted or updated. For example, ask for a late payment to be removed or a balance to be updated.

-

Signature: Sign and date the letter. Sending by certified mail provides proof of delivery.

Stick to the facts and be clear about the specific change needed. Avoid lengthy descriptions and emotional appeals. Keeping your letter short, direct and professional gives you the best chance of success.

Helpful Tips for an Effective Credit Dispute

Follow these tips when drafting your credit dispute for the best results:

-

Dispute online for fastest resolution: The credit bureaus allow you to initiate disputes online and track progress through an online portal. This is often faster than mail.

-

Dispute with each bureau separately: Dispute the item with Experian, Equifax, and TransUnion individually as they don’t share dispute documents.

-

Be persistent: Continue disputing until errors are corrected. Some errors take multiple disputes to resolve.

-

Notify the creditor: Consider also sending a dispute letter directly to the creditor reporting the error.

-

Request account updates: Ask creditors to report your updated status to all bureaus after resolving disputes.

-

Monitor changes: Check your credit reports periodically to ensure corrections are made and new errors didn’t arise.

Examples of Effective Credit Dispute Letters

To see how a thorough dispute letter comes together, here are some examples:

Example Letter Disputing a Late Payment:

To Whom It May Concern:

I am disputing a late payment reporting on my credit report for my Citibank credit card account #1234567890. The payment due on 04/12/2019 is incorrectly listed as late on my Equifax credit report.

I have included a copy of my checking account statement showing the payment for $426 was processed on 04/05/2019, a week before the due date. As evidenced by my on-time payment, I request that you remove the late payment marker from my credit history immediately.

Thank you for your prompt attention to this matter.

Sincerely,

[Your Name]

Example Letter Disputing an Incorrect Balance:

Dear [Bureau Name]:

I am writing regarding account #123456789 at Chase Bank reporting inaccurately on my TransUnion credit report. The current balance is incorrectly listed as $1,564, but I have documentation showing I paid this account in full last year.

Enclosed is a copy of the account statement from Chase Bank showing the account was paid and closed on 10/13/2020 with a $0 balance. Please update or remove this account from my credit report to reflect that the balance is fully paid as of 10/13/2020.

I appreciate you taking the time to investigate this error and request that you send me confirmation once it has been corrected.

Thank you,

[Your Name]

Don’t Let Errors Hold Down Your Credit Score

Checking your credit reports regularly and disputing any inaccurate information is an important way to protect your credit standing. With the right dispute letter contents, you can increase your chances of getting credit bureaus to promptly fix errors.

Taking the time to draft complete, compelling dispute letters can save you thousands down the road on higher loan and credit costs. Don’t let mistakes weigh down your credit score unfairly. Know what to include in credit disputes and use this process to keep your credit report in top shape.

What If The Information is Right…But Not Good?

If there’s information in your credit history that’s correct, but negative — for example, if you’ve made late payments — the credit bureaus can put it in your credit report. But it doesn’t stay there forever. As long as the information is correct, a credit bureau can report most negative information for seven years, and bankruptcy information for 10 years.

Dispute mistakes with the credit bureaus

You should dispute with each credit bureau that has the mistake. Explain in writing what you think is wrong, include the credit bureau’s dispute form (if they have one), copies of documents that support your dispute, and keep records of everything you send. If you send your dispute by mail, you can use the address found on your credit report or a credit bureau’s address for disputes.

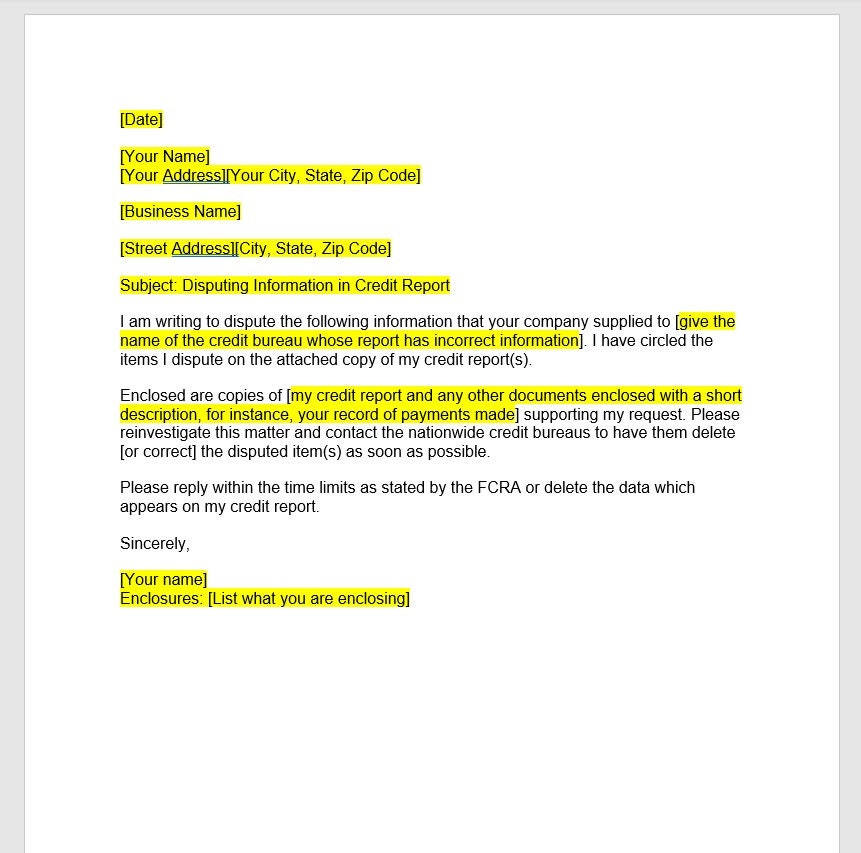

- Use this sample letter to help write your own.

- Your letter should:

- Ask the credit bureau to remove or correct the inaccurate or incomplete information.

- Include:

- your complete name and address

- each mistake that you want fixed, and why

- copies (not originals) of documents that support your request

- a copy of your report (circle the mistakes you want fixed),

- Send your letter by certified mail and pay for a “return receipt” so you have a record the credit bureau got it.

- Keep copies of everything you sent. The credit bureaus also accept disputes online or by phone:

- Experian (888) 397-3742

- Transunion (800) 916-8800

- Equifax (866) 349-5191

- However you filed your dispute, the credit bureau has 30 days to investigate it.

- If the credit bureau considers your request to be “frivolous” or “irrelevant,” they will stop investigating, but they need to notify you of that and give the reason. For instance, you may need to give them additional evidence to support your request.

- The credit bureau will also forward all the evidence you submitted to the business that reported the information. Then, the business must investigate and report the results back to the credit bureau. If the business finds the information they reported is inaccurate, it must notify all three nationwide credit bureaus so they can correct the information in your file.

- The credit bureau must give you the results in writing and, if the dispute results in a change, a free copy of your credit report. This doesn’t count as your free annual credit report.

- The credit bureau

- must send notices of the correction(s) to anyone who got your report in the past six months, if you ask

- must send notice of the correction to anyone who got a copy for employment purposes during the past two years, if you ask

- You can ask that a statement of the dispute be included in your file and in future reports. Also, you can ask that the credit bureau give your statement to anyone who got a copy of your report in the recent past — you can expect the credit bureau to charge you a fee to do this.

How I REMOVED A COLLECTION from my CREDIT REPORT in 24 HOURS!

FAQ

What should I say to dispute on my credit report?

Just a letter stating “you are reporting a debt in my name, account xxxxxx, in the amount of xxxxxx. I wish to dispute this debt, as I have no knowledge of this account. ” It could look the same through all three bureaus, just change the address in the header.

What is the best reason to put when disputing a collection?

Incorrect Balance or Payment Status For example, the debt might show as unpaid even after you’ve settled it, or the amount might be inflated due to fees. If you find errors in the balance or payment status, dispute them right away to have the information corrected or removed.

What’s the best dispute reason?

Fraudulent Transactions: One of the most common reasons for a chargeback is fraud. A customer might notice charges on their credit card statement for purchases they did not authorize. Upon investigation, they discover their credit card information was stolen and contact their bank to file chargebacks.

What to say when filing a dispute?

Your letter should identify each item you dispute, state the facts, explain why you dispute the information, and ask that the business that supplied the information take action to have it removed or corrected.