You might think making a lot of money can automatically grant you access to the best interest rates on things like mortgages, credit cards, auto loans and more. But thats not true.

When it comes to borrowing money, “credit score is usually king,” J. R. George, senior vice president at Trustco Bank, tells CNBC Make It.

Straight up: Is it possible to make so much money that your credit score doesn’t matter? “Absolutely not,” George replies.

Higher earnings can certainly help you attain good credit, but only if youre managing your money and debt payments wisely.

Hey everyone! Today we’re going to have a heated debate about money: is income or credit score more important? If you’re like me, you’ve probably wondered if making more money automatically makes you good with lenders, or if that mysterious three-digit number on your credit report is the real boss. That’s right, you can’t just choose one over the other. Stay with me while I explain this in simple terms, share some personal stories, and help you figure out where to put your money-making efforts.

Where we live on the web, we like to keep things real when we talk about money. To cut to the chase, your credit score is usually more important to lenders right away, but your income is what keeps everything together. Confused? Don’t worry, I gotchu. We’ll talk about how these two big things affect your money in different ways and why you can’t ignore either of them.

What’s the Big Deal with Income and Credit Score?

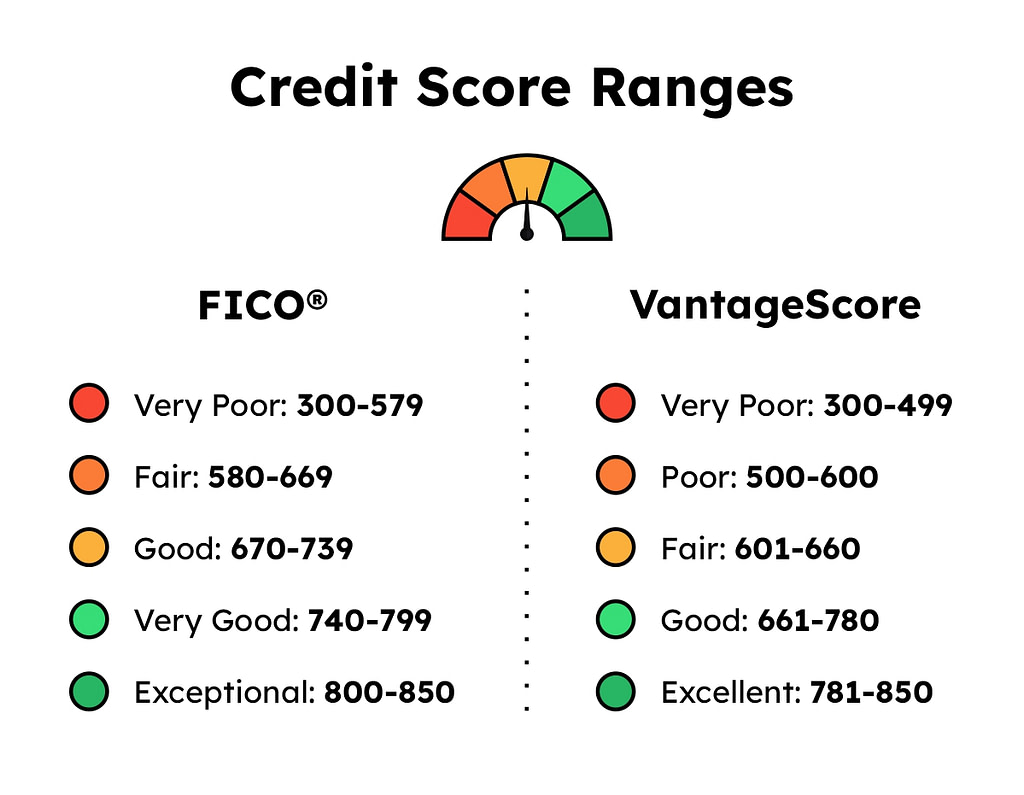

Let’s make sure we know what we’re talking about before we get into a fight. Your income is the money you make, like from a job, a side job, or anything else that puts money in your bank account. What lenders really want to know is your credit score, which is a number between 300 and 850 that shows how well you handle debt. Think of it as your financial report card.

Here’s the catch: a lot of people think that a big paycheck means a great credit score. I know I did when I was living off of ramen and dreams, but they’re not really linked. Let’s see why.

Credit Score: The Gatekeeper to Financial Goodies

I’m puttin’ credit score in the spotlight first ‘cause, honestly, it’s often the first thing lenders eyeball Whether you’re applyin’ for a credit card, a car loan, or even a mortgage, that number can make or break your shot Here’s why it’s such a big deal

- Loan Approvals Depend on It: Lenders use your credit score to decide if you’re worth the risk. A high score (think 700+) can get you approved faster than you can say “new car smell.” A low one? You might get the cold shoulder or slapped with crazy interest rates.

- Interest Rates and Terms: Got a good score? You’ll likely snag lower rates, savin’ you heaps of cash over time. Bad score? You’re payin’ through the nose with high interest.

- Credit Card Offers: Ever notice how some peeps get fancy cards with cashback and travel perks? That’s ‘cause a solid credit score unlocks those sweet deals.

- Beyond Loans: In some places, a crappy score can hike up your insurance premiums or even mess with job apps, especially if the gig involves money stuff.

So, what builds this all-important score? It ain’t rocket science, but it’s worth knowin’ the breakdown. Here’s the recipe for a FICO score, the most common type lenders check:

| Factor | Weight | What It Means |

|---|---|---|

| Payment History | 35% | Do ya pay bills on time? Late payments hurt big time. |

| Amounts Owed | 30% | How much debt you got vs. your credit limit. Keep it low! |

| Length of Credit History | 15% | How long you’ve had credit. Older is better. |

| New Credit | 10% | Applyin’ for lotsa new accounts can look risky. |

| Credit Mix | 10% | Having different types of credit (cards, loans) helps. |

See? Income ain’t even on the list. Your paycheck doesn’t get a say in this score, no matter how big or small. But don’t count income out yet—it’s got its own sneaky ways of matterin’.

Income: The Silent Powerhouse Behind the Scenes

Alright, let’s flip the coin and talk income. Even though it don’t directly touch your credit score, it’s like the engine keepin’ your financial car runnin’. Without decent cash flow, you’re gonna struggle to keep up with bills, and that’s where things get messy. Here’s how income flexes its muscles:

- Ability to Pay Bills: Lenders wanna know if you got the moolah to cover what you owe. They call this your “capacity.” If your income’s too low to handle monthly payments, you might miss ‘em—and that tanks your credit score faster than a bad TikTok trend.

- Credit Limits: When you apply for a card or loan, they often ask for your income. Why? ‘Cause they might set your credit limit based on what you earn. Higher income can sometimes mean a bigger limit, which helps keep your usage rate low (a good thing for your score).

- Loan Approvals and Pre-Qualifications: Some loans or cards got minimum income requirements. Don’t meet ‘em? You’re outta luck, no matter how shiny your credit score is.

- Interest Rates (Sometimes): In a few cases, a higher income might score you better rates or lower fees. It ain’t guaranteed, but it can tip the scales.

I remember when I landed my first decent-paying gig. Thought I was hot stuff, ready to borrow big. But my credit score was still trash from old mistakes, so lenders didn’t care about my new paycheck. On the flip side, I’ve seen friends with so-so income but killer scores get approved for stuff I couldn’t touch. It’s a weird dance, y’all.

Head-to-Head: Which One Wins in Real Life?

Now that we got the basics, let’s pit these two against each other in real-world scenarios. I’m gonna walk ya through some common situations to see where income or credit score takes the crown.

Scenario 1: Applyin’ for a Mortgage

- Credit Score’s Role: King of the hill here. Lenders check your score first to see if you qualify and what rate you’ll get. A score below 620 might mean you’re stuck with higher rates or flat-out denied for conventional loans.

- Income’s Role: Still crucial, though. They’ll look at your debt-to-income ratio (DTI)—that’s your monthly debt payments divided by your monthly income. A high DTI, even with a great score, can mess up your approval. They wanna know you can afford the house payments.

- Winner: Credit score edges out slightly ‘cause it’s the first hurdle. But income ain’t far behind.

Scenario 2: Gettin’ a Credit Card

- Credit Score’s Role: Again, the big player. Your score decides if you get the card and what kinda perks or limits come with it. Low score? You’re lookin’ at secured cards or high-interest junk.

- Income’s Role: They’ll ask for your income on the app to gauge what limit to give ya. Too low, and you might not meet their minimum, even with a decent score.

- Winner: Credit score, hands down. It’s the gatekeeper for most card offers.

Scenario 3: Rentin’ an Apartment

- Credit Score’s Role: Landlords often pull your credit to see if you’re reliable. A bad score can make ‘em think twice, even if you got cash.

- Income’s Role: They’ll wanna see proof of income—usually 2-3 times the rent. No steady paycheck? Good luck convincin’ ‘em, no matter your score.

- Winner: Income might take it here. Many landlords prioritize knowin’ you can pay over a shiny credit number.

Scenario 4: Car Loan or Lease

- Credit Score’s Role: Huge. Your score sets the interest rate on that loan. Good score = cheap loan. Bad score = ouch, them payments sting.

- Income’s Role: They check if you can afford the monthly hit. Low income might limit how much car you can buy, even if your score is solid.

- Winner: Credit score, ‘cause it directly impacts cost. But income sets the stage.

From these, ya can see it’s situational. Credit score often opens the door, but income keeps you from trippin’ on the way in.

Why Ya Can’t Ignore Either: A Personal Wake-Up Call

Lemme get real with y’all for a sec. A few years back, I was hustlin’ with a patchy income—some months flush, others bone-dry. My credit score wasn’t terrible, but it wasn’t great neither. I figured, “Hey, I got some cash now, I’ll just apply for this loan.” Denied. Why? ‘Cause my score screamed “risky,” even though I coulda paid. Later, when I had a steadier gig but let some bills slip, my score dropped, and suddenly no one wanted to touch me, even with proof of income.

Point is, ya gotta play both sides. Ignore your credit score, and you’re locked outta opportunities. Ignore your income, and you can’t sustain the game—missed payments will bite ya in the butt and drag that score down. It’s like tryna ride a bike with one wheel missin’. Ain’t gonna work.

How to Boost Your Financial Game: Tips for Both

Since we’re pals, I ain’t leavin’ ya hangin’ without some actionable goodies. Here’s how to level up both your income and credit score game. Start with these, and you’ll be flexin’ financially in no time.

Beefin’ Up Your Credit Score

- Pay on Time, Every Time: This is 35% of your score, fam. Set reminders, auto-payments, whatever it takes. Late payments are the devil.

- Keep Debt Low: Don’t max out them cards. Aim to use less than 30% of your limit. Got a $1,000 limit? Keep the balance under $300.

- Don’t Apply for Too Much at Once: Every app can ding your score a bit. Space ‘em out.

- Check for Errors: Sometimes your credit report got mistakes. Dispute ‘em for free through the big bureaus. I caught a wrong late payment once—fixed it and my score jumped!

- Mix It Up: If you only got cards, maybe get a small loan to show you can handle different credit. Don’t overdo it, tho.

Pumpin’ Up Your Income

- Side Hustle Hard: Drive for rideshares, freelance, sell stuff online. Every extra buck helps pad your capacity to pay.

- Ask for a Raise: If you been killin’ it at work, march into that boss’s office and make your case. Worst they can say is no.

- Cut Expenses: More money saved = more money to handle debts. Ditch that overpriced latte habit (yeah, I’m guilty too).

- Upskill: Learn somethin’ new—coding, design, whatever—and snag a higher-payin’ gig. I took a cheap online course once and doubled my freelance rates.

- Update Lenders: If your income jumps, tell your card issuers. Might get a limit bump, which helps that utilization rate.

Debt-to-Income Ratio: The Secret Sauce

One thang I wanna toss in here is your debt-to-income ratio, or DTI. It’s a fancy way of sayin’ how much of your income goes to debt each month. Lenders love lookin’ at this to see if you’re stretched thin. Here’s the quick math:

- DTI = (Monthly Debt Payments) / (Monthly Income) x 100

Example: You pay $500 in debt monthly and earn $2,000. Your DTI is 25%. Most lenders want this under 36-40% for big loans like mortgages. High income can keep this low, even if you got debt. But if income’s tight, even small debts make your DTI ugly. It’s another spot where income shines indirectly.

Strikin’ the Balance: My Final Take

So, which is more important, income or credit score? If I gotta pick, I’d say credit score often steals the show ‘cause it’s the first thing checked for most financial moves. It’s like your ID at the club—don’t got it, don’t get in. But income is the fuel in your tank. Without it, you ain’t goin’ nowhere, no matter how pretty your ID looks.

Truthfully, tho, ya need both in harmony. A banging credit score with no cash flow means you can’t pay what you owe, and that score will crash. A hefty income with a trash score means doors stay shut, or you pay stupid fees to squeeze through. At our blog, we reckon it’s about buildin’ both—keep earnin’ more while managin’ credit like a pro.

What’s Next for You?

I’m curious—where you at with this? Is your credit score holdin’ ya back, or is income the struggle? Drop a comment if ya wanna share. And hey, if you found this helpful, spread the love with your crew. We’re all tryna climb this money mountain together.

Also, keep peekin’ at our blog for more straight-up financial chatter. Next time, we might dig into boostin’ that score quick or weird ways to grow income. ‘Til then, keep hustlin’ and don’t let neither of these slip. You got this, homie!

Good pay doesn’t mean good habits

Your credit score on its own doesnt say much about your income. Because its based on your borrowing behavior and history, as well as your ability to manage debt, you can have good credit on a low income or bad credit on a high income.

No matter how much you earn, you can damage your credit history by making late payments on debt or other bills.

“Someone who makes a million dollars a month and doesnt pay their $20 Verizon bill or their $20 credit card bill — for whatever reason that happens — that can turn into a significant amount of problems for the bank,” George says.

In the worst situations, “that’s a sign that if we give this person a car loan, we’ll probably have to take it back.” “.

George says that if you want to borrow money for any reason, your credit will almost certainly be checked. But your income isnt always given the same weight.

“Every lender is a little bit different — it may depend on [the] loan amount, it may depend on the score — but a lot of times, proof of income may not even be required,” George says. If you want to borrow money, on the other hand, you always need a credit score that has been checked by the lender. “.

Youre unlikely to find a lender who only considers your income and not your credit score, he adds.

Which Credit Score Type Is Most Important?

FAQ

Does income matter more than credit score?

Your income doesn’t directly impact your credit score, though how much money you make affects your ability to pay off your loans and debts, which in turn affects your credit score. “Creditworthiness” is often shown through a credit score.

Is debt to income more important than credit score?

Debt-to-credit and debt-to-income ratios can help lenders assess your creditworthiness. Your debt-to-credit ratio may impact your credit scores, while debt-to-income ratios do not. Lenders and creditors prefer to see a lower debt-to-credit ratio when you’re applying for credit.

What is more important, money or credit?

You might think that getting the best interest rates on mortgages, credit cards, auto loans, and other loans just because you make a lot of money is a given. But that’s not true. When it comes to borrowing money, “credit score is usually king,” J. R. George, senior vice president at Trustco Bank, tells CNBC Make It.

Is credit limit based on income or credit score?

Your credit card limit is based on based on income among other factors, including payment history, payment amounts, credit score, utilization and, in the case of a credit limit increase, the tenure of the card member’s relationship with the card issuer.