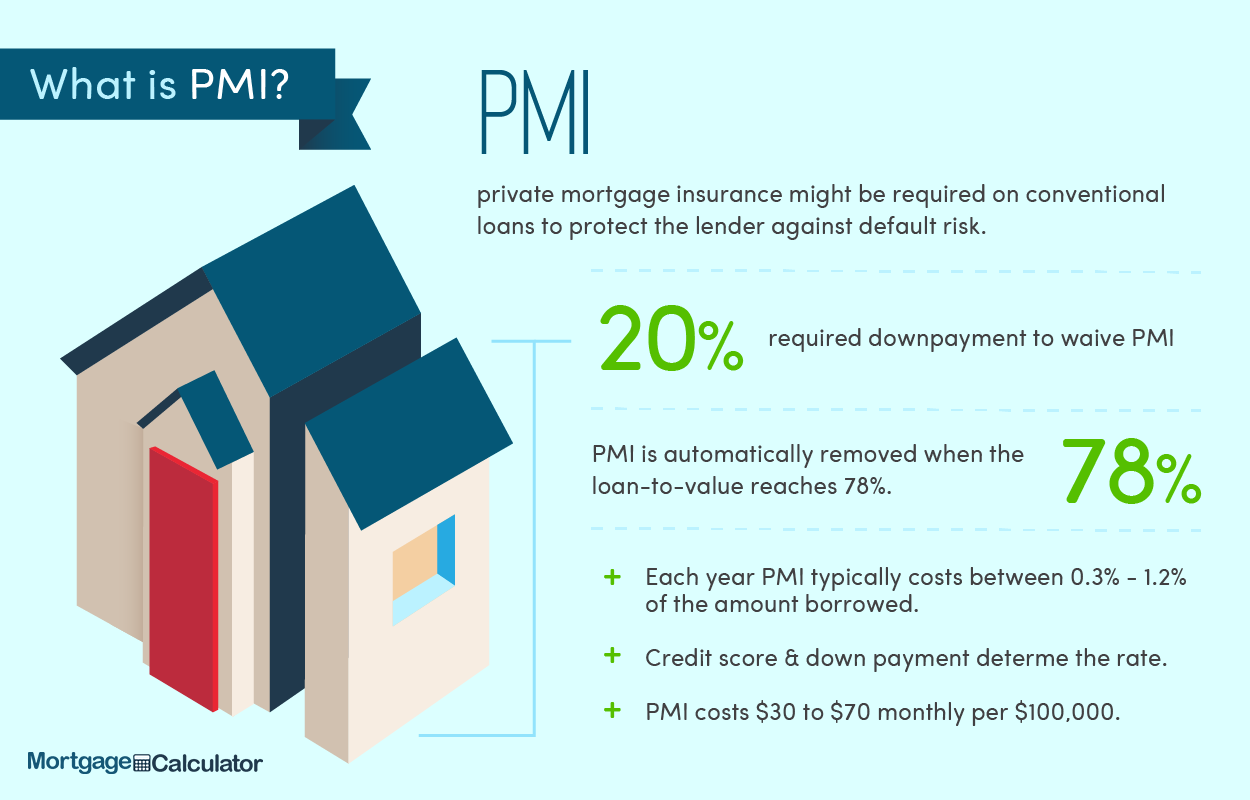

Private mortgage insurance (PMI) is an extra fee that buyers must pay if they buy a house with less than 20% down. This kind of insurance protects the lender in case the borrower defaults. Unfortunately, for many buyers, a down payment of less than 20% is the only option for buying a home. Learn more about why you should avoid paying PMI, and what you can do to stop paying it sooner.

The cost of homeownership can go up a lot if you have private mortgage insurance (PMI). But why is PMI so expensive?

This comprehensive guide will examine the key reasons behind PMI’s high costs and provide strategies to avoid paying these expensive premiums. We’ll also look at whether PMI can benefit some homebuyers despite its drawbacks.

What is Private Mortgage Insurance?

First, let’s quickly review what PMI is

PMI is an insurance policy that protects the lender if the borrower doesn’t pay back the loan. It is usually needed when buyers put down less than 20% of the purchase price.

Lenders think that borrowers who put down less than 20% are a bigger risk. PMI helps mitigate that risk. The lender can file an insurance claim to get their money back if the borrower stops paying.

PMI premiums are paid by the borrower as part of their monthly mortgage payment. The insurance stays in place until the borrower builds 20% equity in the home.

Key Reasons Why PMI is So Expensive

There are several key factors that contribute to PMI’s steep costs:

1. Mitigating Lender Risk

As mentioned, PMI primarily exists to protect the lender if the borrower defaults. Naturally, lenders charge higher premiums to offset this increased risk.

Borrowers with smaller down payments are statistically more likely to default. So PMI rates for these buyers are inflated to account for the heightened default risk.

2. Administrative Costs

Servicing PMI policies generates considerable administrative expenses for insurance providers. These include costs for underwriting, claims processing, risk monitoring, and more.

These overhead costs get passed along to borrowers through higher premiums.

3. Profit Motive

Like any insurance product, PMI policies need to be profitable for the insurers. The premiums must not only cover claims and overhead, but also generate an adequate return for shareholders.

This profit motive contributes to inflated costs that exceed the true risks and expenses involved.

4. Limited Competition

The PMI industry is dominated by a handful of major providers. This lack of competition enables the existing companies to charge higher premiums.

If there were more players in the market, competitive pressures would likely bring down costs. But currently, only a few insurers control the majority of the PMI market.

5. Policy Guidelines

PMI providers establish guidelines dictating the minimum length of time a policy must remain in effect and when PMI can be canceled. This locks borrowers into paying for coverage even after they’ve built substantial equity.

For FHA loans in particular, PMI can’t be removed over the life of the loan no matter how much equity the borrower has.

6. Housing Price Growth

In many markets, home prices have gone up faster than incomes, making it harder for buyers to make down payments.

This growing gap makes PMI necessary for more home purchases. As usage increases, insurers can charge higher premiums across the board.

Strategies to Avoid Paying PMI

Given the hefty costs, it’s smart to explore options to avoid PMI if possible. Here are some tactics to reduce or eliminate your PMI payments:

Make a 20% Down Payment

The most straightforward way to avoid PMI is to put at least 20% down upfront. This exempts you from mortgage insurance requirements completely.

Of course, this strategy only works if you have substantial savings or other sources to draw from like gifts or inheritance.

Use a Piggyback Loan

With a piggyback loan, you take out a first mortgage for 80% of the purchase price plus a second mortgage for 10% to reach 90% total financing. This structure lets you skip PMI while still putting down less than 20%.

However, second mortgages often have less favorable terms than first mortgages. And you’ll have higher total monthly payments than with PMI.

Ask Your Lender

Some lenders may be willing to waive PMI for borrowers with excellent credit and finances. It never hurts to negotiate with lenders to see if they’ll remove PMI as a closing gift or concession.

Just keep in mind that most lenders will be hesitant to forego this risk protection. But it can’t hurt to politely ask.

Shop Around

PMI rates can vary significantly between providers. Spend time shopping and comparing quotes. A little legwork could uncover much lower PMI rates than what your initial lender quoted.

Boost Your Credit

Buyers with higher credit tend to qualify for lower PMI rates or exemption from PMI requirements altogether. Work on improving your score before applying for a mortgage.

Consider Government Loans

Certain government-backed loans like VA and USDA mortgages don’t require PMI at all. Of course, these programs have eligibility rules, and the rates may be higher. But they present another potential route to avoid PMI.

Make a Higher Down Payment

Even if you can’t make a full 20% down payment, chipping in extra from your savings could help. Most lenders charge lower PMI rates for buyers who put 10% or 15% down versus 5%.

When Can PMI Make Sense?

Despite the drawbacks, PMI isn’t always a bad option. Here are some cases where accepting PMI could be beneficial:

You Can’t Afford 20% Down

For many buyers, a 20% down payment simply isn’t feasible given their finances. The monthly PMI premiums may be cheaper than waiting years longer to save up a full 20% down payment.

You Have Excellent Credit

Buyers with top credit scores can often secure low PMI rates around 0.25% – 0.5% annually. At those levels, PMI adds just $25-$50 to the monthly payment on a $250,000 mortgage. That modest extra cost may be worthwhile to get into your dream home sooner.

You Plan to Move Again Quickly

If you expect to move again in 3-5 years, paying PMI for a short time can be manageable. You likely won’t pay more than a few thousand dollars before moving and eliminating PMI.

You Can Remove PMI Soon

Likewise, if your particular home is likely to appreciate quickly, you may be able to cancel PMI within a couple years by requesting reappraisal once your equity tops 20%.

You Need to Stretch Financially

Opting for PMI could make homeownership possible if the incremental monthly cost fits within your budget better than higher mortgage payments without PMI.

You Value Flexibility

Going without PMI requires tying up more money in your down payment. Some buyers may prefer to conserve their liquid savings and investments even if that means paying PMI.

Key Takeaways

-

PMI drives up the cost of homeownership significantly. But legitimate reasons explain its high premiums like covering lender risk and administrative expenses.

-

Reducing or eliminating PMI should be a priority for most buyers. But exceptions exist where PMI can be the optimal choice based on your finances and circumstances.

-

No single approach is right for everyone. Carefully weigh the costs against the benefits before making your PMI decision.

While less than ideal, PMI may be a necessary stepping stone to homeownership for some buyers. The key is going in with eyes wide open about the added costs. With diligent research and comparison shopping, you can minimize your PMI expense and determine if it fits into your homebuying budget.

How Can I Avoid Paying PMI?

If you put down more than 20% on a mortgage, you can avoid paying PMI. Mortgages with down payments of less than 20% will require PMI until you build up a loan-to-value ratio of at least 80%. You can also avoid paying PMI by using two mortgages, or a piggyback second mortgage.

PMI Is Not Tax Deductible

Until 2017, PMI was tax-deductible, but only if a married taxpayer’s adjusted gross income was less than $110,000 annually. The 2017 Tax Cuts and Jobs Act (TCJA) ended the deduction for mortgage insurance premiums entirely, effective 2018. PMI was also deductible during the COVID-19 pandemic but is no longer deductible.

Is PMI Actually Expensive?

FAQ

Is it better to pay PMI or put 20% down?

The Bottom Line. PMI is expensive. Unless you think you can get 20% equity in the home within a couple of years, it probably makes sense to wait until you can make a larger down payment or consider a less expensive home, which will make a 20% down payment more affordable.

Why is my PMI so high?

PMI is priced primarily on your mortgage credit score, your debt to income (DTI) ratio, and your % down. If your DTI > 45% your PMI goes up quite a lot. If your credit score is < 720 your PMI goes up quite a lot. If both are true, your PMI goes up a lot a lot. And the less you put down, the higher the PMI rate.

How do you avoid paying PMI?

To avoid paying Private Mortgage Insurance (PMI), the most straightforward way is to make a down payment of at least 20% of the home’s purchase price when getting a conventional loan. If you can’t afford a 20% down payment, other options include getting a VA or USDA loan, using a piggyback loan, or paying a higher interest rate.

Can PMI be removed if house value increases?

Yes, you may be able to have PMI removed if your home’s value increases. But it ultimately depends on whether your home’s LTV is now below 80%. For instance, if you owe $300,000 on your mortgage and the home is worth $360,000, you could divide $300,000 by $360,000 to get 0. This would give you your LTV. 83.