Vega measures an options sensitivity to changes in the implied volatility of the underlying asset. While vega is included in the group of “Greeks” used in option analysis, it is the only one not represented by an actual Greek letter.

Vega essentially reports on the sensitivity of an option to fluctuations in volatility. If the vega value is high, the option price will be more affected by changes in volatility. If the vega value is low, the option price will be less affected by changes in volatility.

In the world of options, the “Greeks” are a set of parameters that show how risky an options position is. The Greeks are often used to help traders and investors manage the risk of each option position and the portfolio as a whole.

The Greeks are referred to as such because each dimension of risk is represented by a Greek letter. The primary Greeks are: delta, gamma, theta, vega and rho.

I’ve been there: you buy an options contract, and then the price of it goes through the roof even though the underlying stock doesn’t change much. It’s very frustrating when you can’t figure out why your options positions are acting so strangely. A lot of the time, the answer lies in a mysterious Greek letter called “vega,” which controls the price of options.

As an options trader for over 8 years, I’ve learned that understanding vega isn’t just some fancy technical term – it’s a practical necessity that can make or break your trading strategy. Let’s break down what vega really means in simple terms, with real examples that’ll help you make better trading decisions.

What Is Vega in Options Trading?

Vega measures how sensitive an option’s price is to changes in implied volatility. Specifically, vega tells you how much an option’s price will change for every 1% move in implied volatility.

For example, if an option has a vega of 0. 20, its price will increase by $0. 20 per share when implied volatility rises by 1%. That’s a $20 change in the total price of the standard options contract, which is equal to 100 shares.

Vega is like a “volatility meter” because it tells you how much your option will change when the market is nervous or calm.

Why Vega Matters to Options Traders

New traders often only think about whether a stock will go up or down, not how volatility will affect it. This is a big mistake! Here’s why you should pay attention to vega:

- Both calls and puts have positive vega – meaning both increase in value when volatility rises

- Volatility can change rapidly – especially around earnings announcements or economic news

- You can profit from volatility changes alone – even if the stock price doesn’t move as expected

- Vega helps explain “unexplained” price movements – when your options move differently than expected

I remember buying Apple calls before an earnings announcement, expecting the stock to rise. The stock did go up slightly, but my options actually lost value! Why? Implied volatility dropped significantly after the announcement (a phenomenon called “volatility crush”), and the high vega of my options meant they were highly sensitive to this change.

How Vega Affects Option Pricing

Vega’s impact on option pricing follows some predictable patterns that can help guide your trading:

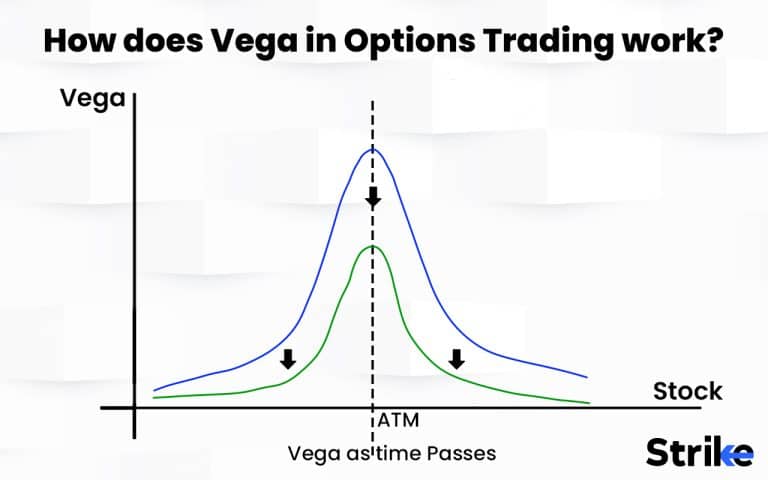

At-the-Money Options Have Highest Vega

Options that are at-the-money (when strike price equals current stock price) typically have the highest vega. This makes sense because these options have the greatest uncertainty about whether they’ll expire in-the-money.

Longer-Term Options Have Higher Vega

The more time until expiration, the higher the vega. An option expiring in 3 months will generally have a much higher vega than one expiring next week. This happens because there’s more time for volatility to impact the option’s outcome.

Let me show you a real-world example with an Apple (AAPL) option:

AAPL Stock Price: $225

Option type: Call option with $225 strike (at-the-money)

Expiration: 3 months out

Implied volatility: 25%

Initial premium: $10 per share ($1,000 total for one contract)

Vega: 0.20

If implied volatility rises from 25% to 30% (a 5% increase):

- Vega impact: $0.20 × 5 = $1.00 per share

- New premium: $11 per share ($1,100 total)

- Profit from volatility change alone: $100

That’s a 10% return just from a volatility change, even if the stock price doesn’t move at all!

The Relationship Between Volatility and Vega

Let’s be clear about something that confuses many traders: volatility and vega aren’t the same thing.

- Volatility measures how much and how quickly a stock’s price moves

- Vega measures how much an option’s price responds to changes in implied volatility

Implied volatility reflects what the market expects about future price fluctuations. When traders anticipate more dramatic price swings (like before earnings announcements), implied volatility typically rises.

Time’s Impact on Vega

Vega doesn’t stay constant throughout an option’s life. Here’s what happens as time passes:

- Vega typically decreases as expiration approaches – the “vega decay” phenomenon

- Options approaching expiration have much lower vegas – making them less sensitive to volatility changes

- Future-dated options have positive vega – while options expiring immediately have negative vega

This time element creates interesting trading opportunities. For instance, if you expect volatility to increase in the future, buying longer-dated options with higher vega gives you more exposure to that volatility change.

Vega and Other Option Greeks

Vega is just one of several “Greeks” that measure different factors affecting option prices. Understanding how vega interacts with other Greeks gives you a more complete picture:

Vega vs. Theta

While vega measures sensitivity to volatility changes, theta measures time decay – how much an option loses value each day as it approaches expiration.

These two often work against each other. An option with high vega might gain value from increasing volatility, but lose value from theta decay. It’s like having one foot on the gas and one on the brake.

Vega in Relation to Delta

Delta measures how much an option’s price changes relative to the underlying stock’s movement. Options with high delta (deeply in-the-money) tend to have lower vega because their prices are more tied to the stock price than to volatility.

Trading Strategies Using Vega

Now that you understand the concept, let’s look at some practical ways to use vega in your trading:

Vega-Neutral Strategies

Some advanced traders create “vega-neutral” positions that balance positive and negative vegas, protecting against volatility changes. For example:

If you buy one at-the-money call with a vega of 0.30 and sell two out-of-the-money calls each with a vega of 0.15, your net vega would be:

(1 × 0.30) – (2 × 0.15) = 0

This position would theoretically be unaffected by volatility changes (though other factors would still impact it).

Speculating on Volatility Changes

If you anticipate increasing market uncertainty (like before major economic announcements), buying options with high vega can be profitable even if you’re not sure which direction the market will move.

I’ve personally used this strategy before Fed announcements, buying both calls and puts with high vega to profit from the expected volatility spike.

Calendar Spreads

Calendar spreads involve selling shorter-term options while buying longer-term options at the same strike price. Since longer-dated options have higher vega, these spreads can profit from volatility increases.

Vega as a Market Sentiment Indicator

Vega can also serve as a barometer for market sentiment. When vegas are generally high across many options, it suggests traders expect turbulence ahead.

The VIX (often called the “fear gauge”) essentially measures implied volatility of S&P 500 options. When the VIX is high, vega is elevated across many S&P 500 options, signaling widespread market anxiety.

Common Misconceptions About Vega

Let’s clear up some common misconceptions:

-

“Vega is a Greek letter” – Surprisingly, vega isn’t actually in the Greek alphabet! It’s a made-up term that options traders adopted.

-

“Only calls have positive vega” – Both calls AND puts have positive vega, meaning both increase in value when volatility rises.

-

“Vega only matters for long-term options” – While longer-dated options have higher vega, even short-term options can be significantly affected by volatility changes, especially around key events.

Calculating and Using Vega in Real Trading

Most trading platforms will calculate vega automatically, but understanding the basic calculation helps appreciate what it represents:

Vega is highest for at-the-money options and decreases as options move either in-the-money or out-of-the-money.

For example, if an option is trading at $7.50 with implied volatility at 20% and vega of 0.12:

- If volatility increases to 21.5% (a 1.5% increase): Option price increases by 1.5 × 0.12 = $0.18 to $7.68

- If volatility decreases to 18% (a 2% decrease): Option price decreases by 2 × 0.12 = $0.24 to $7.26

Practical Tips for Managing Vega Risk

Based on my experience, here are some practical tips for handling vega in your trading:

-

Always check the vega of your options before entering a trade, especially before high-volatility events

-

Be cautious of “volatility crush” after scheduled announcements like earnings – high-vega options can lose value quickly

-

Consider selling options when volatility is unusually high and buying when it’s unusually low

-

Use spreads to reduce vega exposure if you’re primarily betting on price direction rather than volatility

-

Monitor changes in implied volatility as carefully as you watch the underlying stock price

Final Thoughts: Why You Can’t Ignore Vega

I’ve seen too many traders (including myself in my early days) get burned by ignoring vega. They make perfect predictions about stock price movements but still lose money because they didn’t account for volatility changes.

Vega isn’t just some abstract concept – it’s a practical tool that explains why options behave the way they do. By understanding and managing vega, you can:

- Avoid unpleasant surprises when volatility changes

- Create more precise trading strategies

- Find profit opportunities in volatility alone

- Better understand the total risk profile of your options positions

Whether you’re a beginner or experienced trader, paying attention to vega will make you a more effective options trader. It might seem complicated at first, but once you grasp it, you’ll wonder how you ever traded without it!

Have you had any experiences where vega significantly impacted your options trades? I’d love to hear your stories and questions in the comments below.

Vega’s Impact on Option Pricing

Owned options (both calls and puts) have positive vega, which means they typically increase in value when volatility increases, and decrease in value when volatility decreases. Short options (both calls and puts) have negative vega, and work in the opposite fashion—they theoretically decline in value when volatility increases, and increase in value when volatility decreases.

Options with longer dated maturities generally have a higher percentage of vega than closer dated maturities. Additionally, vega is typically higher for at-the-money (ATM) options as compared to out-of-the-money (OTM) options.

A trader that believes implied volatility will increase might therefore gravitate toward owning options with higher vega, to benefit from that potential scenario.

On the other hand, traders who think volatility will go down might want to buy options with lower vega to protect themselves from losing money if prices go down. Alternatively, a trader expecting a decline in implied volatility might elect to sell an option, to capitalize on a potential drop in volatility.

Positive and Negative Vega

Vega essentially reports on the sensitivity of an option to fluctuations in volatility. If the vega value is high, the option price will be more affected by changes in volatility. If the vega value is low, the option price will be less affected by changes in volatility.

Both calls and puts that are owned have positive vega, which means that their value usually goes up when volatility goes up and down when volatility goes down. Short options, like calls and puts, have negative vega and work the opposite way. In theory, their value goes down when volatility goes up and up when volatility goes down.

Option Vega Explained (The Volatility Greek Tutorial)

FAQ

Is high Vega good for options?

Traders use vega when they expect big changes in market volatility. For instance, if the volatility of a stock is anticipated to increase because of an upcoming earnings announcement, they might buy options with higher vega to benefit from the expected increase in volatility.

What does Vega tell you in options?

Vega is an options “Greek” that measures an option’s sensitivity to changes in implied volatility. This number tells you how much the price of an option is likely to change for every 1% change in implied volatility.

Is a negative Vega good?

Vega is one of option Greeks, which measures how the value of an option (or a combination of options) changes when implied volatility increases. Positive vega means that the position gains value with rising volatility, while negative vega means it loses.

Do I want a low or high Vega buying call?

But it would have a negligible impact on low Vega call premiums. So, adjusting the Vega when trading options allows for better volatility risk management. Low Vega protects your position if volatility moves against your expectation, while high Vega lets you profit more if it shifts your way.