In today’s uncertain economic landscape, many of us are wondering if £1 million is truly enough to fund a comfortable retirement. While this may seem like an enormous sum at first glance, the reality might surprise you. As someone who’s spent years researching retirement planning, I can tell you that the answer isn’t as straightforward as you might hope.

Is £1 Million Really Enough? The Million-Pound Question

Let’s be honest – £1 million sounds like a lot of money. But when you stretch it across 20, 30, or even 40 years of retirement, things get complicated fast. The simple answer is yes, you can retire with £1 million, but whether it’s enough depends on several factors unique to your situation.

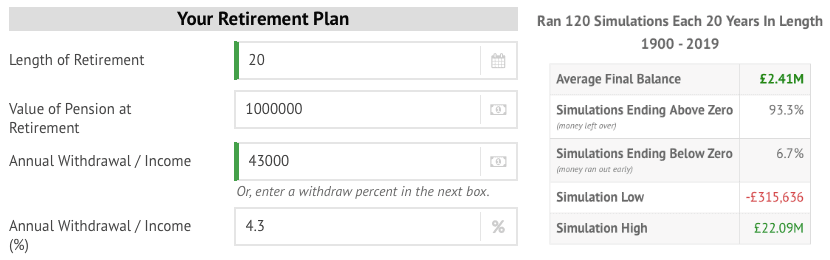

According to the Pensions and Lifetime Savings Association (PLSA), a ‘comfortable’ lifestyle in retirement costs about £43,100 annually for a single person or £59,000 for a couple after tax This level of income would allow

- £130 weekly food budget

- Up to £1,500 yearly on clothing and footwear per person

- Three weeks of European holidays annually

- £600 yearly for property maintenance (plus a £300 buffer for unexpected expenses)

But is this your idea of “comfortable”? You might want more—or be perfectly happy with less.

Breaking Down the Numbers: How Long Will £1 Million Last?

One popular approach to retirement planning is the 4% rule. This suggests withdrawing 4% of your retirement savings annually, meaning a £1 million pension pot would provide about £40,000 per year. Under ideal conditions, this should last between 25-30 years.

However, real-world analysis shows more nuanced figures:

A 66-year-old retiree with a £1 million pension who chooses income drawdown could receive:

- £63,000 annually until age 86

- £50,000 annually until age 95

This assumes:

- 5% annual investment growth after fees

- 2% inflation rate with income increasing accordingly

Remember though a 66-year-old woman today has an average life expectancy of 88 years, with a 25% chance of living to 94 and a 10% chance of reaching 98. That’s a lot of years to fund!

Alternative Retirement Income Options

If you’re worried about outliving your money (a valid concern!), you might consider an annuity instead of income drawdown. Currently, a 66-year-old purchasing an annuity with a £1 million pension fund could receive a guaranteed annual income of up to £67,000 for life.

But don’t forget about these additional income sources that can supplement your pension

- State Pension: Currently provides £230.25 weekly (about £11,502 annually) if you’ve accumulated 35 qualifying years of National Insurance contributions

- Private Pensions: Additional workplace or personal pensions

- ISAs: Particularly stocks and shares ISAs offering tax-free growth

- Property: Potential rental income or equity release

- Other Investments: Dividends, bonds, etc.

Key Factors Affecting How Far Your £1 Million Will Stretch

1. Your Retirement Lifestyle

Be brutally honest with yourself here. Your lifestyle choices significantly impact how long your money will last:

- Basic retirement: Covering essentials only (housing, utilities, groceries, healthcare)

- Moderate retirement: Basic needs plus leisure activities and occasional luxuries

- Luxurious retirement: Frequent international travel, high-end dining, expensive hobbies

Each level requires vastly different funding.

2. Life Expectancy

People in the UK typically need to plan for 20-30 years of retirement, but increasing life expectancy means your money might need to stretch even further. A £1 million pot feels much less secure if you need to fund 30+ years of retirement.

3. Housing Costs

Do you own your home outright? Still paying a mortgage? Planning to rent? Housing costs can easily consume a significant portion of your retirement income. Even if your home is paid off, maintenance costs don’t disappear.

4. Healthcare Expenses

While the NHS covers many healthcare needs, dental care, private treatments, and especially long-term care can be expensive. These costs typically increase as we age, potentially putting pressure on your retirement savings.

5. Inflation

This is the silent retirement killer! Even moderate inflation gradually erodes your purchasing power. What costs £1,000 today might cost £1,600+ in 20 years with just 2.5% annual inflation. Your retirement plan MUST account for this.

Strategies to Make Your £1 Million Last Longer

1. Pension Drawdown

This flexible approach keeps your pension invested while allowing you to withdraw income as needed. You can adjust your withdrawals based on your changing circumstances, but remember that investment values can fall, potentially reducing your overall pot.

2. Consider an Annuity

While they offer lower initial income than aggressive drawdown strategies, annuities provide guaranteed income for life. This peace of mind is valuable, especially if you’re worried about outliving your savings. Some annuities even include inflation protection, though these start at lower rates.

3. Create a Realistic Budget

This sounds boring, but it’s crucial! Tracking your spending and sticking to a carefully planned budget can significantly extend the life of your retirement savings. Many retirees are shocked by how quickly money disappears without proper monitoring.

4. Diversify Your Investments

Even in retirement, maintaining a diversified investment portfolio is essential to balance risk and potential returns. Spreading investments across different asset types can protect your savings from market downturns while still capturing growth opportunities.

5. Consult a Financial Adviser

This might be the most important strategy of all. A professional financial adviser can help tailor a plan based on your specific circumstances and retirement goals. They’ll guide you through investment strategies, withdrawal rates, and tax-efficient approaches that maximize your retirement savings.

Real Talk: Is £1 Million Enough for YOU?

I’m not gonna sugar-coat this – whether £1 million is enough for your retirement depends entirely on your personal circumstances. For some, it’s more than sufficient; for others, it may fall short.

Before making any decisions, ask yourself:

- What kind of lifestyle do I want in retirement?

- How long might I live (consider family history)?

- What other income sources will I have?

- What major expenses do I anticipate?

- How might inflation affect my plans?

My Final Thoughts

A £1 million pension pot puts you in a strong position compared to most UK retirees. With careful planning and management, it can provide a comfortable retirement for many people.

However, retirement planning isn’t a one-size-fits-all proposition. The earlier you start seriously planning (ideally with professional guidance), the better your chances of achieving the retirement you desire.

Remember that retirement finances aren’t just about having “enough” – they’re about having enough to support the lifestyle you’ve worked hard to enjoy in your later years. Don’t leave this to chance!

Have you started planning for your retirement yet? What steps are you taking to ensure your financial security? I’d love to hear your thoughts and experiences in the comments below!

Disclaimer: This article provides general information only and should not be considered financial advice. The value of investments can fall as well as rise, and you may get back less than you invested. Tax treatment depends on individual circumstances and may change in the future. Always consult with a qualified financial adviser before making significant retirement decisions.

What factors affect how much you need to retire?

When considering if 1 million is enough to retire, you need to weigh up these factors:

The UK state pension can be important in supplementing your retirement savings, reducing the amount you need to withdraw from your £1 million pot.

As of 2025/26, the Trust Funds: The Real Deal on Pros and Cons of Setting One Up