The supposedly secret trick does not build your credit scores, despite what you may have heard. But there are some concrete steps you can take.

Many or all of the products on this page are from partners who compensate us when you click to or take an action on their website, but this does not influence our evaluations or ratings. Our opinions are our own.

Sometimes a grain of truth about a financial topic can morph into something that’s just plain misleading. One example is the 15/3 credit card payment trick — or hack — that you might have seen touted on the internet and social media as a secret tactic for improving bad or mediocre credit.

The 15/3 hack claims you can help your credit score dramatically by making half your credit card payment 15 days before your account statement due date and the other half-payment three days before. Problem is, it doesnt work.

“Every few years some nonsense like this gains some momentum, but theres no truth to it,” John Ulzheimer, an Atlanta-based credit expert, said in an email. Ulzheimer has worked for FICO and the credit bureau Equifax.

The number of payments you make in a credit card billing cycle — a month — does not help your number of on-time payments, a factor in widely used credit-scoring models. You’ll get credit for just one on-time payment during that month. And there’s nothing magical about 15 days and three days before your due date. In fact, it’s too late by then. At 15 days before your due date, your statement is already closed and your credit card company has likely already reported your information to the credit bureaus.

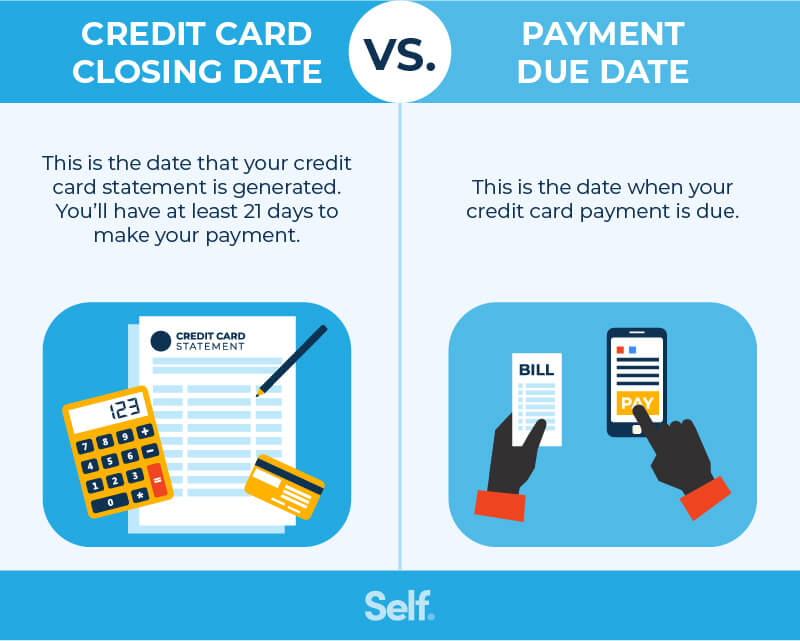

(To be fair, some also claim the rule is 15 days and three days before your statement closing date. Targeting the statement closing date at least makes a little sense, as we’ll see later — but the 15 and 3 are still irrelevant.)

What is true about credit card payments and what can help? Making multiple payments in a month could help your credit scores temporarily by making it look like you’re using less credit, but not in the way the 15/3 hack describes.

The U.S. credit-scoring system is objectively confusing, so it’s no wonder some people are misguided in promoting the 15/3 myth. But here’s what’s wrong with the 15/3 credit card hack and what really helps your credit scores.

While we’re myth-busting, let’s address one of the biggest falsehoods in credit cards: Credit scores are helped by carrying a monthly balance and paying interest. This is false. Period. Paying interest is not a factor in credit scoring. The best advice is always the same, and thats to pay your balance in full every month if you can.

The Truth About the 15/3 Credit Card Payment Method That’s Taking Social Media By Storm

Have you seen those viral TikTok videos claiming you can boost your credit score by 100 points in just a few months? The so-called 15/3 credit card hack has been spreading like wildfire across FinTok (that’s financial TikTok for us oldies) and other social media platforms. But before you jump on this bandwagon, let’s dig into what this payment method really is and whether it actually works.

I’ve been managing my credit cards for over a decade now, and I’m always skeptical about “secret hacks” that promise dramatic results. So I did some deep research to find out if this one holds water.

What Exactly Is the 15/3 Credit Card Payment Method?

The 15/3 credit card payment method suggests making two payments per month instead of one:

- Pay half of your credit card statement balance 15 days before the due date

- Pay the remaining half 3 days before the due date

For example, if your credit card bill is $2,000 and it’s due on the 25th of the month, you’d pay $1,000 on the 10th and another $1,000 on the 22nd.

Some versions of this trick swap the due date for the statement closing date (which typically comes about three weeks before your payment due date).

The promoters of this method claim it can

- Increase the number of on-time payments reported to credit bureaus

- Lower your credit utilization ratio

- Boost your credit score dramatically (some claim by up to 100 points!)

But is there any truth to these claims? Well, yes and no.

Why the 15/3 Credit Card Hack Doesn’t Work as Advertised

Let’s get real here – this hack doesn’t work the way many social media influencers claim it does. Here’s why:

1. You Don’t Get Extra “On-Time Payment” Credits

Credit card companies typically report to the credit bureaus just once a month – not multiple times. Making two payments instead of one doesn’t double your “on-time payment” history. Your account status for the month is reported as either current (paid on time) or delinquent. The number of payments you make doesn’t matter.

As John Ulzheimer a credit expert who has worked for FICO and Equifax stated “Every few years some nonsense like this gains some momentum, but there’s no truth to it.”

2. The Timing Is Off

Credit card issuers generally report your account status and balance to credit bureaus around your statement closing date – not your payment due date. By the time you’re 15 days before your due date, your statement has already closed, and your account info has likely already been reported!

3. The Numbers 15 and 3 Are Arbitrary

There’s nothing magical about making payments exactly 15 and 3 days before the due date. These specific numbers don’t have any special significance to credit scoring models.

The Grain of Truth: Credit Utilization Does Matter

So why did this myth catch on? Because there is a kernel of truth in it related to credit utilization.

Your credit utilization ratio – how much credit you’re using compared to your total available credit – accounts for about 30% of your FICO credit score. Lower utilization (ideally below 30%, and even better below 10%) can indeed help your credit score.

The part that’s correct is that making a payment before your statement closing date (not due date) can lower your reported balance, which might decrease your utilization rate and potentially boost your score temporarily.

But this isn’t a secret hack – it’s just standard credit advice that’s been misinterpreted and embellished.

Pros and Cons of Making Multiple Credit Card Payments

Even though the 15/3 method isn’t the miracle credit booster it’s claimed to be, there are some benefits to making multiple payments throughout the month:

Pros:

- Better Budget Management: Breaking up payments can make budgeting easier, especially if you’re paid biweekly

- Lower Interest Accrual: If you carry a balance, making earlier payments can reduce how much interest accrues

- Helps Avoid Missing Payments: More frequent attention to your credit card might help you avoid accidentally missing a due date

- Can Help With Cash Flow: Splitting payments might better align with when you receive income

Cons:

- Won’t Magically Improve Payment History: Multiple payments don’t count extra toward your payment history

- May Not Lower Utilization: Unless timed correctly with your statement closing date

- Adds Complexity: Having to remember multiple payment dates can be a hassle

- False Expectations: Following this “hack” expecting dramatic results will lead to disappointment

What Really Helps Your Credit Score

If you’re serious about improving your credit score, focus on these proven strategies instead:

-

Pay your bills on time, every time: Payment history is the single biggest factor in your credit score, accounting for 35% of your FICO score.

-

Keep utilization low: Try to use less than 30% of your available credit. If possible, make payments before your statement closing date to reduce reported balances.

-

Don’t apply for too much new credit at once: Each application can cause a small, temporary dip in your score.

-

Maintain a good mix of credit types: Having both revolving accounts (like credit cards) and installment loans (like auto loans) can help your score.

-

Build a long credit history: Keep old accounts open, even if you don’t use them much.

-

Consider adding alternative data: Services like Experian Boost allow you to add utility, phone, and streaming service payments to your credit report.

Better Alternatives to the 15/3 Credit Card Hack

Instead of focusing on the 15/3 method, try these more effective strategies:

Set Up Autopay

Configure automatic payments for at least the minimum payment to avoid late payments. You can always make additional manual payments if you want to pay more.

Pay Down Balances Before Statement Closing Date

If you’re trying to reduce utilization, make payments before your statement closes rather than before the due date. This is when your balance is typically reported to the credit bureaus.

Make Weekly Payments

If you want to make multiple payments, consider aligning them with your paychecks or setting up a weekly payment schedule. This can help keep your balances lower throughout the month.

Monitor Your Credit

Use free services to track your credit score and report. Many credit card issuers now offer free FICO score monitoring.

My Experience with Multiple Credit Card Payments

I’ve personally experimented with different payment schedules over the years. While making multiple payments didn’t magically boost my credit score, I did find that paying more frequently helped me stay more aware of my spending and kept my utilization naturally lower.

What worked best for me was setting up automatic payments for the minimum due (as insurance against forgetting) and then manually paying larger amounts throughout the month as my budget allowed. This approach gave me flexibility while ensuring I never missed a payment.

The Bottom Line: Is the 15/3 Method Worth Trying?

While the 15/3 credit card payment method isn’t harmful, it’s not the credit score miracle that some claim. If splitting your payment into two installments helps you budget better, go for it! Just don’t expect dramatic changes to your credit score solely from this technique.

Remember that your credit score is built on consistent, responsible behavior over time – not on quick hacks or tricks. Focus on paying on time, keeping your balances low relative to your credit limits, and maintaining a healthy mix of accounts.

As credit expert Ulzheimer put it: “The truth is paying your bill before the due date will never, ever increase your scores by some drastic amount.”

FAQs About Credit Card Payments and Credit Scores

Q: Will making two payments instead of one help my credit score?

A: Not directly. Credit card companies typically only report your account status once per month, so multiple payments don’t create multiple “on-time payment” entries in your credit history.

Q: When do credit card companies report to credit bureaus?

A: Most credit card issuers report your account information to the credit bureaus around your statement closing date, not your payment due date.

Q: What’s the best time to pay my credit card bill to improve my credit score?

A: If you’re trying to lower your reported utilization, make payments before your statement closing date (not the due date). This will reduce the balance that gets reported to the credit bureaus.

Q: Does carrying a balance help build credit?

A: No! This is a common myth. You don’t need to carry a balance or pay interest to build credit. Paying your full statement balance by the due date is the best practice.

Q: How quickly can I expect to see my credit score improve?

A: Credit improvement takes time. Focus on consistent good habits rather than quick fixes. Most people see meaningful improvements over 3-6 months of positive behavior.

What credit card payment strategies have worked for you? Have you tried the 15/3 method? I’d love to hear about your experiences in the comments!

What’s the truth?

The grain of truth in the 15/3 hack is that credit utilization matters to credit scores.

Credit utilization is simply how much credit you’re using vs. how much credit you have. Scoring models award you a higher score if you have lots of available credit, but use very little of it.

Your credit score is a snapshot in time reflecting your creditworthiness. Purposefully lowering your utilization on a certain date is like applying lipstick before the photo is taken.

But your effort to pretty-up your utilization only lasts one month — until the next month when your creditors report your balances and limits again and you have a new utilization ratio. So unless you were going to apply for a loan or otherwise needed to show a handsome credit score on a specific date, your effort was wasted.

It’s like you put on a fine suit but sat home alone. Nobody saw it, or cared.

Why the 15/3 credit hack is wrong

The main problems with the 15/3 hack:

- Wrong date peg. Typically, on or near your statement closing date — not the payment due date — your credit card company reports to the credit bureau or bureaus with such information as your balance and credit limit. It does this only once a month. Your due date comes about three weeks after that. So targeting the due date makes no sense. Making a payment 15 days and three days before the credit card due date, as the 15/3 hack suggests, is too late to influence credit reporting for that billing cycle.

- Multi-payment myth. You don’t get extra credit, so to speak, for making two payments instead of one, or making a payment early. Your creditor only reports to the bureaus once a month.

- 15/3 is random. If you use the 15/3 definition pegging payments to your closing date, that can help, for reasons well discuss below. But 15 and 3 are irrelevant. You might as well make a single payment prior to the closing date. The creditor is just reporting what your balance is at the end of the billing cycle.

“Theres no relevance to when you make the payment or payments prior to the statement closing date,” Ulzheimer said. “You can make a payment every single day if you like. Fifteen and three days doesnt do anything different than paying it off one or two days before the statement closing date.”